Estrategia de stop-loss de seguimiento de tendencia RSI

Resumen

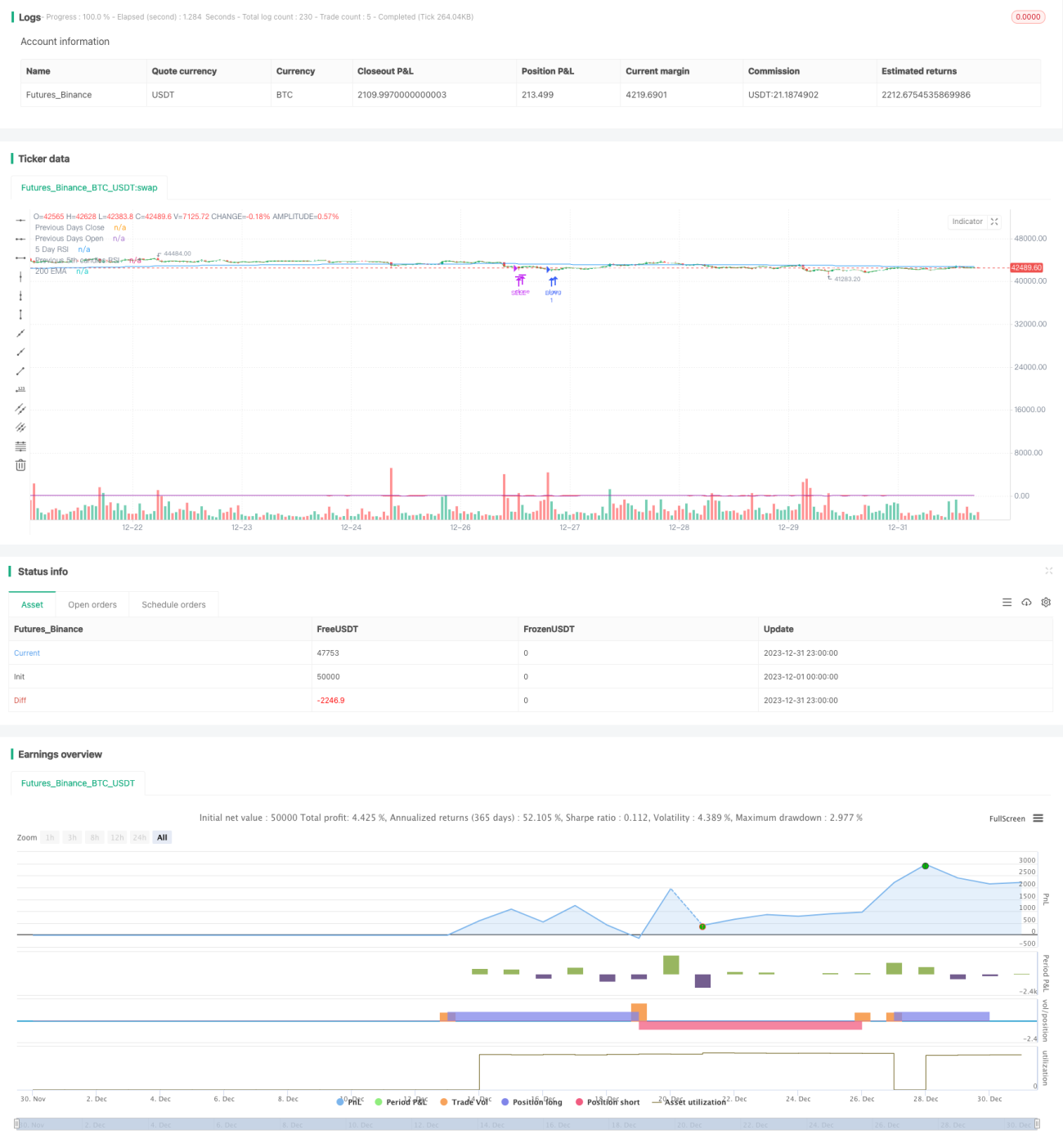

Se trata de una estrategia de trading cuantitativa que utiliza el indicador RSI para identificar tendencias y establecer stops y targets dinámicos. Esta estrategia combina el RSI para determinar la dirección del mercado y establece stops y targets dinámicos para asegurar ganancias y minimizar el riesgo.

Principio de la estrategia

La estrategia utiliza principalmente el indicador RSI para determinar la dirección del mercado y decidir si abrir posiciones largas o cortas. Cuando el RSI cruza al alza la línea de sobreventa (nivel bajo), se considera que el mercado está en una tendencia alcista y se abre una posición larga. Cuando el RSI cruza a la baja la línea de sobrecompra (nivel alto), se considera que el mercado está en una tendencia bajista y se abre una posición corta.

Al mismo tiempo, la estrategia rastrea el precio de apertura de cada orden y establece stops y targets dinámicos. Para las posiciones largas, se establece un stop loss como un porcentaje del precio de apertura; para las cortas, se establece un take profit como un porcentaje del precio de apertura. Cuando el precio alcanza el nivel de stop o target, la estrategia cierra automáticamente la posición para detener la pérdida o asegurar la ganancia.

Ventajas de la estrategia

- Utiliza el RSI para determinar la dirección de la tendencia, evitando operar en rangos laterales.

- Establece stops y targets dinámicos, lo que permite asegurar ganancias de manera flexible y controlar eficazmente el riesgo.

- Los parámetros del RSI y los porcentajes de stop/target se pueden ajustar y optimizar mediante entradas externas.

Riesgos de la estrategia

- El indicador RSI tiene cierto rezago, lo que puede hacer que se pierdan puntos de cambio de tendencia a corto plazo.

- Si las líneas de stop y target están demasiado cerca, pueden ser superadas, provocando el cierre prematuro de la posición.

Direcciones de optimización

- Se pueden probar diferentes períodos del RSI para evaluar su efectividad.

- Se pueden probar distintas combinaciones de parámetros para encontrar la mejor relación stop/target.

- Se pueden agregar indicadores adicionales para filtrar señales.

Conclusión

En general, esta estrategia es una estrategia de trading cuantitativa que utiliza el RSI para seguir la tendencia y lo complementa con stops y targets dinámicos. En comparación con estrategias basadas en un solo indicador, esta estrategia gestiona mejor el riesgo y permite asegurar ganancias de manera efectiva. Mediante la optimización de parámetros y la incorporación de indicadores auxiliares, se puede mejorar aún más su rendimiento.

- 1