Estrategia de media móvil envolvente dinámica

Resumen

Esta estrategia implementa operaciones tanto largas como cortas basándose en medias móviles y bandas dinámicas. Sigue la ruptura del precio por encima o por debajo de las bandas para establecer posiciones, y cierra todas las posiciones cuando el precio vuelve a caer por debajo de la media base. Es adecuada para acciones y criptomonedas con tendencias claras.

Principio de la estrategia

Primero, la estrategia calcula una media base basada en el tipo y la longitud de la media móvil seleccionada por el usuario. Las medias móviles comunes incluyen SMA, EMA, etc.

A continuación, según el parámetro porcentual establecido por el usuario, se calculan las bandas superior e inferior. Por ejemplo, un 5% significa que cuando la fluctuación del precio alcanza el 105% del rango permitido (ALLOWED_BRACKET), se activa la apertura de una posición. El número de bandas es personalizable.

En cuanto a las reglas de entrada, si se rompe la banda inferior, se abre una posición larga; si se rompe la banda superior, se abre una posición corta. La regla es muy simple y clara.

Finalmente, cuando el precio vuelve a caer por debajo de la media base, se cierran todas las posiciones. Este es un punto de salida para seguir la tendencia.

Es importante destacar que la estrategia implementa la apertura de posiciones de forma escalonada. Si hay múltiples bandas, el capital se asigna proporcionalmente. Esto evita el riesgo de apostar en una sola dirección.

Análisis de ventajas

Las principales ventajas de esta estrategia son las siguientes:

-

Implementa una función de seguimiento automático de tendencias. El uso de medias móviles para determinar la dirección de la tendencia es muy común, por lo que es un método efectivo.

-

El uso de bandas filtra parte del ruido, evitando problemas de operaciones innecesarias por excesiva sensibilidad. Una configuración adecuada de los parámetros puede optimizar significativamente la rentabilidad de la estrategia.

-

La apertura escalonada de posiciones aumenta la resiliencia de la estrategia. Incluso si una ruptura en una dirección falla, las otras direcciones pueden continuar funcionando bien. Esto optimiza la relación riesgo-beneficio general.

-

Permite personalizar la media móvil y el número de bandas. Esto aumenta la flexibilidad de la estrategia, permitiendo a los usuarios ajustar los parámetros para diferentes activos.

Análisis de riesgos

Los principales riesgos de esta estrategia son:

-

El sistema de medias móviles no es sensible a señales como el cruce dorado. Si no hay una tendencia clara, la estrategia puede perder algunas oportunidades.

-

Si las bandas se configuran demasiado amplias, pueden aumentar el número de operaciones y el riesgo de deslizamiento. Si se configuran demasiado estrechas, se pueden perder movimientos grandes. Encontrar el equilibrio requiere pruebas exhaustivas.

-

En mercados laterales, la estrategia puede tener una mayor probabilidad de quedar atrapada. Por lo tanto, es mejor elegir activos con tendencias claras.

-

La apertura escalonada limita la ganancia por operación individual. Si se busca solo un riesgo unidireccional, se necesita optimización adicional.

Direcciones de optimización

Esta estrategia se puede optimizar principalmente en las siguientes direcciones:

-

Reemplazar otros indicadores para decidir la apertura y cierre de posiciones, como el indicador KDJ, o combinar múltiples indicadores para establecer filtros.

-

Agregar lógica de take profit y stop loss. Esto puede asegurar parte de las ganancias y evitar algunos riesgos de forma activa.

-

Optimizar los parámetros para encontrar la mejor combinación de media móvil y bandas. Esto requiere backtesting completo y optimización para encontrar los mejores pares de parámetros.

-

Combinar tecnologías como el aprendizaje profundo para lograr una optimización inteligente de parámetros, aprendiendo y actualizando la configuración con el tiempo.

-

Considerar las diferencias entre activos y mercados, estableciendo múltiples conjuntos de parámetros para adaptarse a diferentes entornos de negociación. Esto mejorará en gran medida la estabilidad de la estrategia.

Resumen

En general, esta estrategia de medias móviles con bandas dinámicas es muy adecuada para el trading de tendencias. Es simple, eficiente, fácil de entender y optimizar. Como estrategia básica, tiene una gran plasticidad y escalabilidad. Al fusionarse con sistemas más complejos, se pueden optimizar aún más las métricas de rentabilidad y riesgo ajustado. Por lo tanto, puede ser una base excelente para el trading cuantitativo.

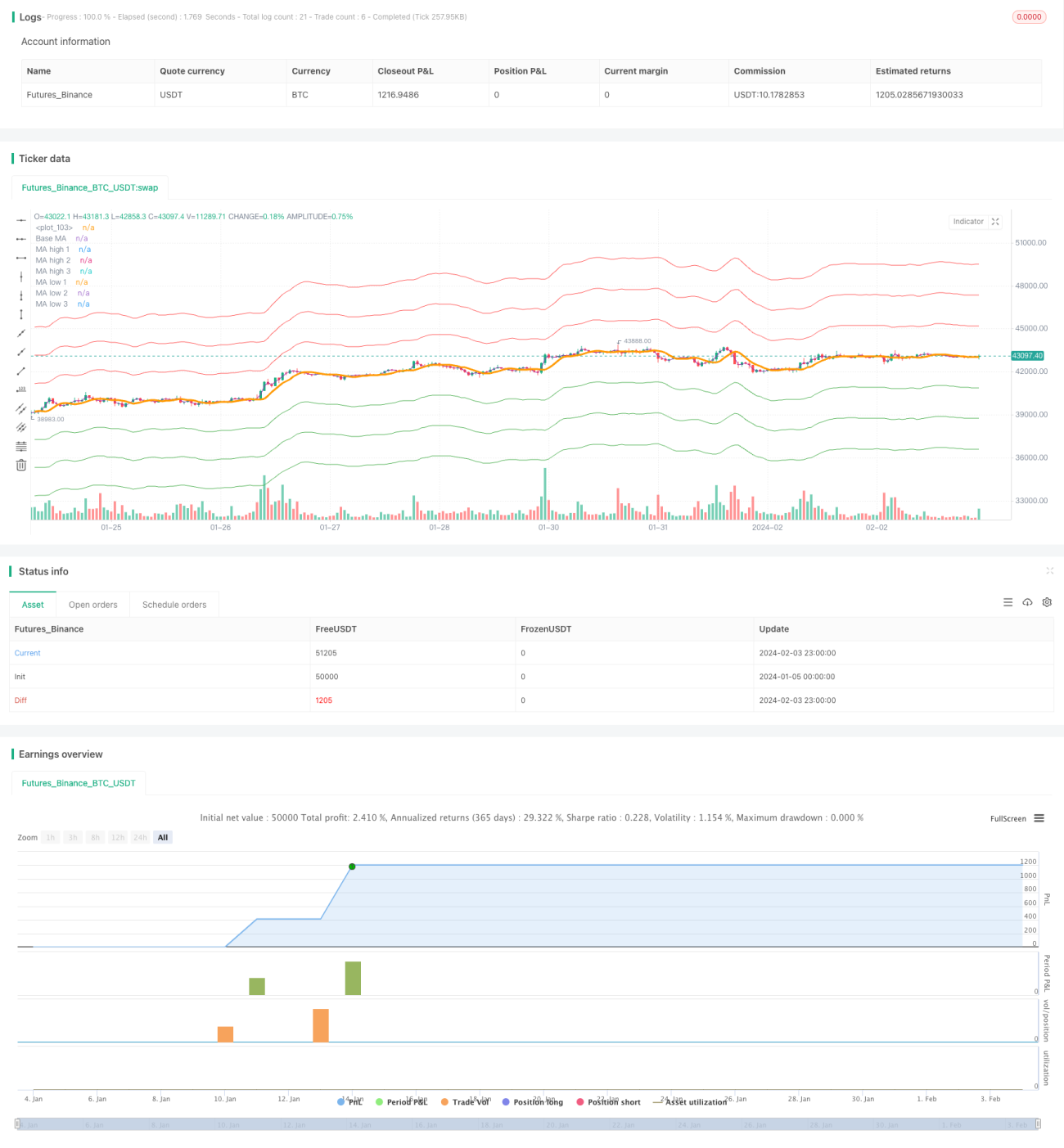

/*backtest

start: 2024-01-05 00:00:00

end: 2024-02-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Envelope Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100, initial_capital=1000, pyramiding = 5, commission_type=strategy.commission.percent, commission_value=0.0)

// CopyRight Crypto Robot- 1