Estrategia de seguimiento de contorno de oscilación adaptativa de múltiples marcos temporales

Resumen

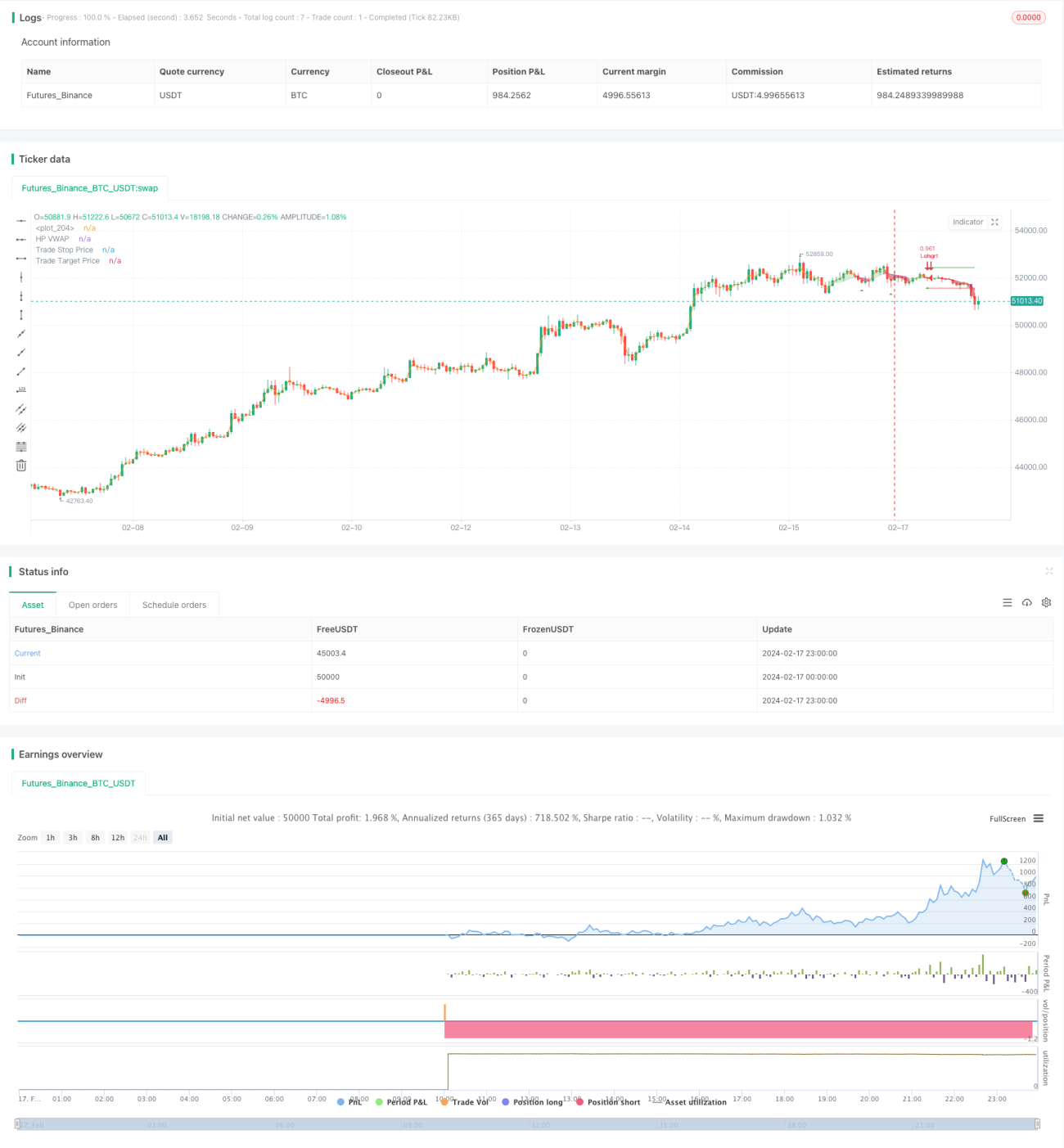

Esta estrategia utiliza el filtro Hodrick-Prescott (HP) para suavizar el precio y extraer la línea de tendencia del precio. Luego, calcula un precio promedio ponderado por volumen (VWAP) personalizado basado en un rango de tiempo definido por el usuario. Cuando el precio está por encima de la línea de tendencia, se toma una posición larga; cuando está por debajo, se toma una posición corta. Además, se combina un stop loss basado en ATR para garantizar que el riesgo de la operación sea manejable.

Principio de la estrategia

-

Utiliza el filtro HP para extraer la línea de tendencia del precio. El filtro HP extrae el componente de tendencia a largo plazo del precio mediante un método de optimización, filtrando las interferencias de las fluctuaciones a corto plazo.

-

Calcula el VWAP basado en un rango de tiempo definido por el usuario. El VWAP refleja con mayor precisión el precio promedio en diferentes períodos.

-

Cuando el precio está por encima de la línea de tendencia HP, se cumple la condición de largos; cuando está por debajo, se cumple la condición de cortos. Esto permite capturar rupturas del precio desde abajo hacia arriba o desde arriba hacia abajo.

-

El stop loss con ATR combina un riesgo razonable para evitar pérdidas excesivas.

Análisis de ventajas

-

Al utilizar el filtro HP para extraer la tendencia del precio, es más suave en comparación con indicadores como la media móvil, evitando ser engañado por fluctuaciones de precio a corto plazo.

-

El VWAP con período personalizado permite una mayor flexibilidad para adaptarse a los cambios del ciclo del mercado.

-

Operar según la dirección de la tendencia se alinea con el concepto de trading de tendencias, lo que proporciona una mayor tasa de aciertos.

-

El stop loss con ATR controla la pérdida por operación, evitando pérdidas excesivas.

-

Múltiples parámetros ajustables ofrecen un amplio margen de optimización para diferentes mercados.

Riesgos y contramedidas

-

En mercados laterales o de consolidación, el stop loss puede activarse con frecuencia. Se puede ampliar adecuadamente el rango del stop loss.

-

Al final de una tendencia, a menudo ocurren rupturas de prueba de retroceso que pueden atrapar la estrategia. Se debe combinar con otros indicadores para identificar el final de la tendencia y cerrar posiciones a tiempo.

-

Una configuración inadecuada del período VWAP puede perder oportunidades de trading más efectivas. Se debe ajustar dinámicamente el período VWAP en conjunto con indicadores de tendencia.

Direcciones de optimización

-

El parámetro λ del filtro HP ajusta la suavidad. Con valores altos de λ, la línea de tendencia es más suave, más adecuada para capturar tendencias a largo plazo; con valores bajos, responde más sensiblemente a los cambios de precio, más adecuada para oportunidades de corto y mediano plazo.

-

El múltiplo del ATR ajusta el rango del stop loss. Se puede optimizar junto con el parámetro λ: cuando λ es alto, se puede ampliar el rango del stop loss; cuando λ es bajo, se puede reducir el rango para asegurar más ganancias.

-

La relación riesgo-recompensa (R:R) afecta directamente la relación ganancia-pérdida. Se pueden probar diferentes múltiplos para evaluar el control de drawdown y la rentabilidad.

Resumen

La estrategia en su conjunto adopta un enfoque de seguimiento de tendencias. A través de diversas configuraciones de parámetros, se puede optimizar para diferentes horizontes temporales (largo, mediano y corto), con una alta tasa de aciertos y buena rentabilidad. En cuanto al control de riesgos, se ha considerado adecuadamente para garantizar que las pérdidas por operación no sean excesivas. En general, la estrategia utiliza métodos más científicos para extraer las características de la tendencia del precio, combinado con un amplio espacio de optimización de parámetros, lo que le otorga un buen potencial de aplicación.

/*backtest

start: 2024-02-17 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tathal animouse hajixde

//@version=4- 1