Estrategia Ichimoku Cloud Nine orientada al trading

Resumen

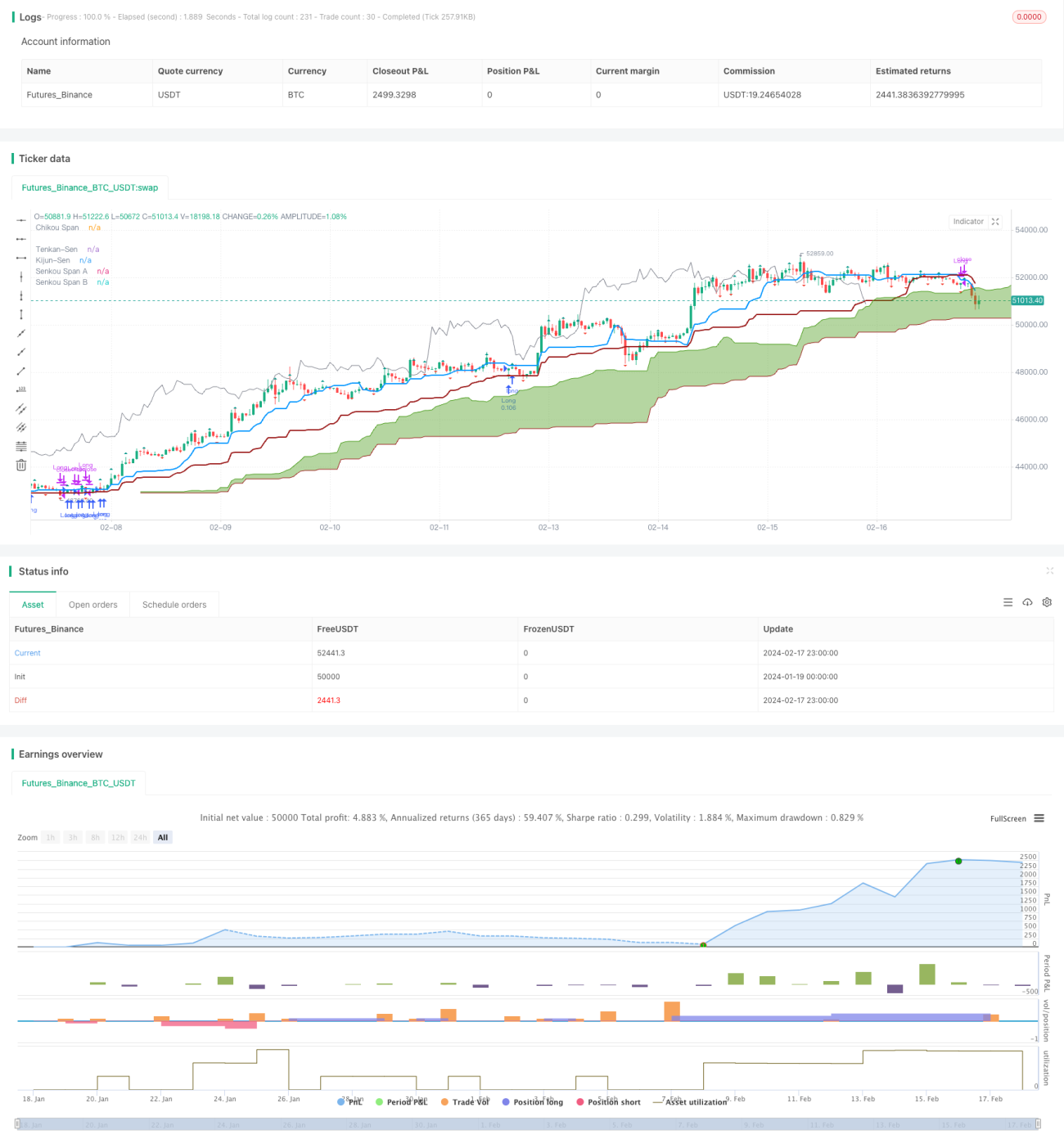

La estrategia Ichimoku Cloud Nine se basa en el indicador Ichimoku Cloud combinado con el Fractal de Williams. Esta estrategia utiliza múltiples señales de trading proporcionadas por el indicador Ichimoku Cloud para generar señales de entrada y salida. Es una estrategia orientada a la operativa real.

Principio de la estrategia

La estrategia se basa principalmente en las siguientes señales de Ichimoku para la entrada:

- Ruptura de la nube: Señal cuando el precio de cierre supera el borde superior o inferior de la nube.

- Cruce TK: Señal cuando la línea de conversión (Tenkan) cruza la línea base (Kijun).

- Giro de la nube: Señal cuando la línea Senkou Span A cruza la línea Senkou Span B.

- Cruce de borde: Señal cuando el precio pasa de un lado de la nube al otro.

Además, la estrategia cierra posiciones en las siguientes situaciones:

- Cierre cuando el precio de cierre entra en la nube.

- Cierre cuando se produce un cruce inverso TK.

- Cierre parcial cuando se rompe el Fractal de Williams.

Esta estrategia integra múltiples señales de trading de la nube Ichimoku, con el objetivo de mejorar la fiabilidad de las señales, mientras utiliza los fractales para establecer stops y controlar el riesgo.

Ventajas de la estrategia

En comparación con estrategias de una sola señal, esta estrategia aprovecha múltiples señales de la nube Ichimoku, lo que permite filtrar señales erróneas y aumentar la precisión. Además, los parámetros de la estrategia se pueden configurar de forma flexible, siendo adecuada para diferentes instrumentos y optimizaciones de parámetros.

Asimismo, la introducción de la ruptura del Fractal de Williams para establecer stops permite controlar el riesgo de manera más activa, asegurar ganancias y evitar pérdidas significativas.

Riesgos de la estrategia

La estrategia enfrenta principalmente los siguientes riesgos:

- El indicador de nube tiene rezago, no refleja cambios de precio de manera oportuna.

- Múltiples señales pueden ser demasiado conservadoras, perdiendo algunas oportunidades.

- El stop basado en fractales puede ser superado, causando pérdidas.

Para mitigar el rezago, se pueden ajustar los parámetros o desactivar algunas señales de filtro. Para el riesgo de stop por fractales, se puede ajustar el período temporal del fractal o aplicar solo un stop parcial.

Direcciones de optimización

La estrategia se puede optimizar principalmente en los siguientes aspectos:

- Ajustar los parámetros de Ichimoku para adaptarse a diferentes marcos temporales e instrumentos.

- Ajustar o desactivar algunas señales de filtro, conservando las señales principales.

- Ajustar los parámetros del fractal, utilizando fractales de mayor período temporal, o aplicando solo un stop parcial.

- Agregar otros filtros de indicadores, como indicadores de volumen.

Conclusión

La estrategia Ichimoku Cloud Nine integra múltiples señales de trading de la nube Ichimoku, aprovechando las ventajas del indicador de nube mientras mejora la precisión y la tasa de acierto de las señales. La estrategia también utiliza fractales como método de stop para controlar el riesgo. Esta estrategia puede optimizarse mediante parámetros y señales, siendo adecuada para el trading algorítmico de múltiples instrumentos.

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Cloud Nine", shorttitle="Ichimoku Cloud Nine", overlay=true, calc_on_every_tick = true, calc_on_order_fills = false, initial_capital = 5000, currency = "USD", default_qty_type = "percent_of_equity", default_qty_value = 10, pyramiding = 3, process_orders_on_close = true)

color green = #459915- 1