Stratégie de trading bidirectionnel sur les fractures de multiples moyennes mobiles

Aperçu

Cette stratégie utilise l'indicateur Williams High/Low pour identifier les signaux de retournement haussier et baissier, combine plusieurs moyennes mobiles pour les transactions sur les écarts, et filtre les faux signaux avec le RSI, permettant ainsi un trading bidirectionnel efficace.

Principe de la stratégie

-

L'indicateur Williams High/Low utilise les prix les plus hauts et les plus bas sur une période donnée pour détecter les points de retournement et générer des signaux d'achat et de vente.

-

Les moyennes mobiles sur 20, 50 et 100 jours forment un système de multiples moyennes. Lorsque le prix franchit deux de ces moyennes, un signal de transaction est émis.

-

Le RSI identifie les zones de surachat et de survente pour filtrer les signaux incertains.

-

La stratégie détermine quelles deux moyennes sont franchies, combine les signaux de l'indicateur Williams et le filtre RSI pour produire des signaux d'achat/vente stables.

-

Entrée en position : Lorsque la moyenne courte traverse de bas en haut les moyennes longues, et que le Williams Low et le RSI bas apparaissent simultanément, on prend une position longue. Lorsque la moyenne courte traverse de haut en bas les moyennes longues, et que le Williams High et le RSI haut apparaissent simultanément, on prend une position courte.

-

Stop loss et take profit : Des niveaux fixes en pourcentage sont définis.

Avantages de la stratégie

-

L'indicateur Williams identifie précisément les supports et résistances clés, et repère les retournements.

-

Le franchissement de multiples moyennes mobiles évite les faux signaux dus aux oscillations d'une seule moyenne.

-

Le RSI aide à filtrer les faux signaux, rendant les points d'entrée plus précis et fiables.

-

Un système fixe de stop loss et take profit contrôle le risque et clarifie les gains et pertes.

-

La double confirmation des indicateurs de retournement et de tendance rend les signaux de transaction plus précis et fiables.

Risques de la stratégie

-

Un choix inapproprié d'instruments de trading peut nécessiter des ajustements de paramètres selon les actifs.

-

Une période d'analyse mal adaptée peut nécessiter des réglages selon les horizons temporels.

-

Un stop loss/take profit fixe ne s'adapte pas aux changements du marché, risquant de couper les positions trop tôt ou de ne pas capturer assez de profits.

-

Des oscillations des moyennes mobiles peuvent générer de faux signaux.

-

Lorsque les indicateurs divergent, les signaux peuvent être retardés.

Pistes d'optimisation

-

Optimiser dynamiquement les paramètres selon les instruments de trading.

-

Ajouter un système de stop loss/take profit adaptatif pour mieux équilibrer gains et pertes.

-

Introduire davantage de filtres (MACD, Stochastic, etc.) pour réduire les faux signaux.

-

Intégrer des algorithmes d'apprentissage automatique pour identifier automatiquement les meilleurs moments de trading.

-

Combiner d'autres indicateurs de tendance pour reconnaître les marchés en tendance.

Résumé

Cette stratégie combine plusieurs outils d'analyse technique (Williams, moyennes mobiles, RSI) et réduit les faux signaux par une double confirmation. Elle capture efficacement les opportunités de retournement tout en maîtrisant les risques grâce à un stop loss/take profit fixe. Globalement, c'est une stratégie de trading bidirectionnel fiable et pratique. Les prochaines étapes consisteront à renforcer ses performances via l'optimisation des paramètres, l'ajustement du stop loss/take profit et l'intégration de modèles.

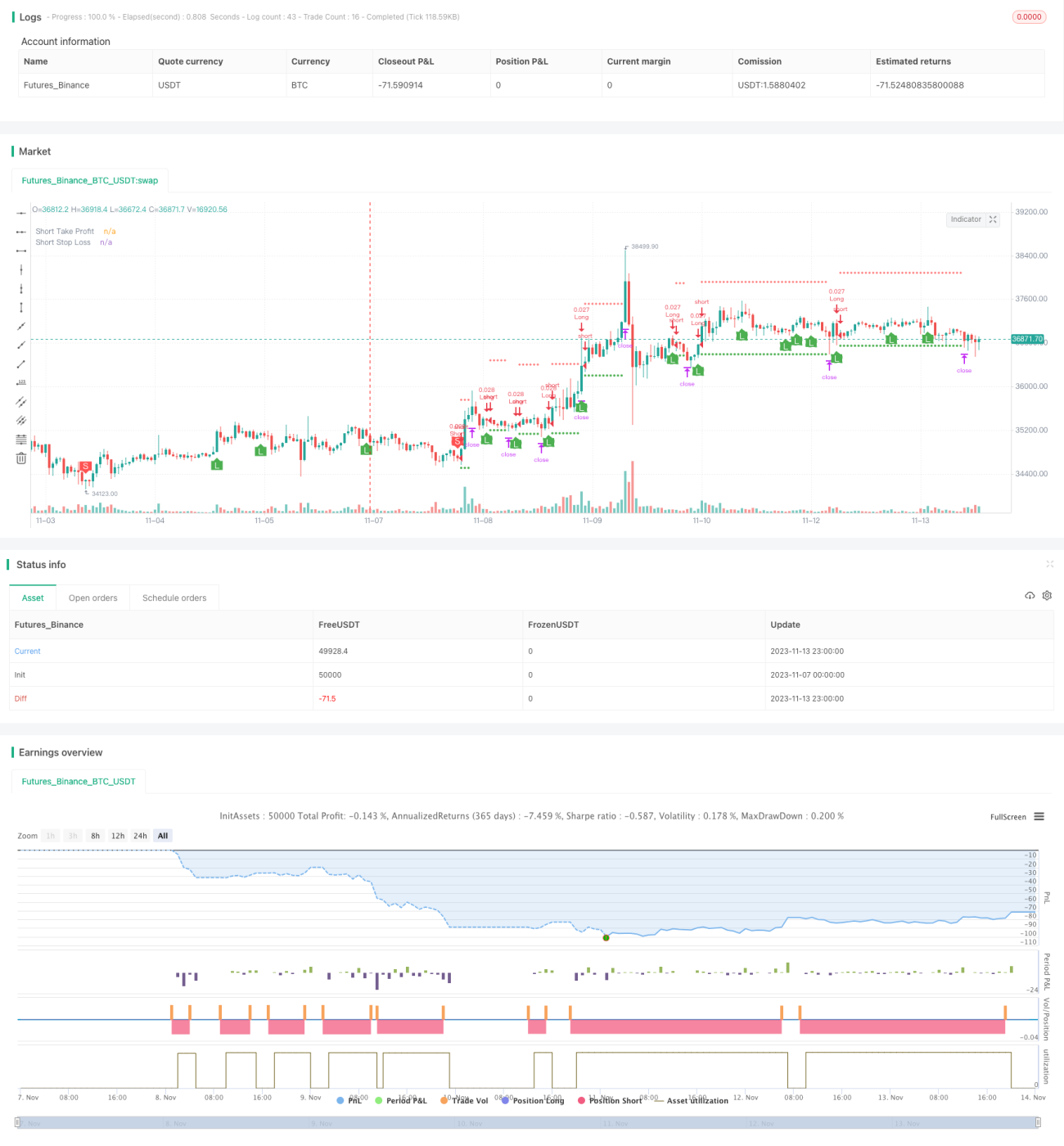

/*backtest

start: 2023-11-07 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © B_L_A_C_K_S_C_O_R_P_I_O_N

// v 1.1

- 1