Stratégie de trailing stop basée sur TFO et ATR

Aperçu

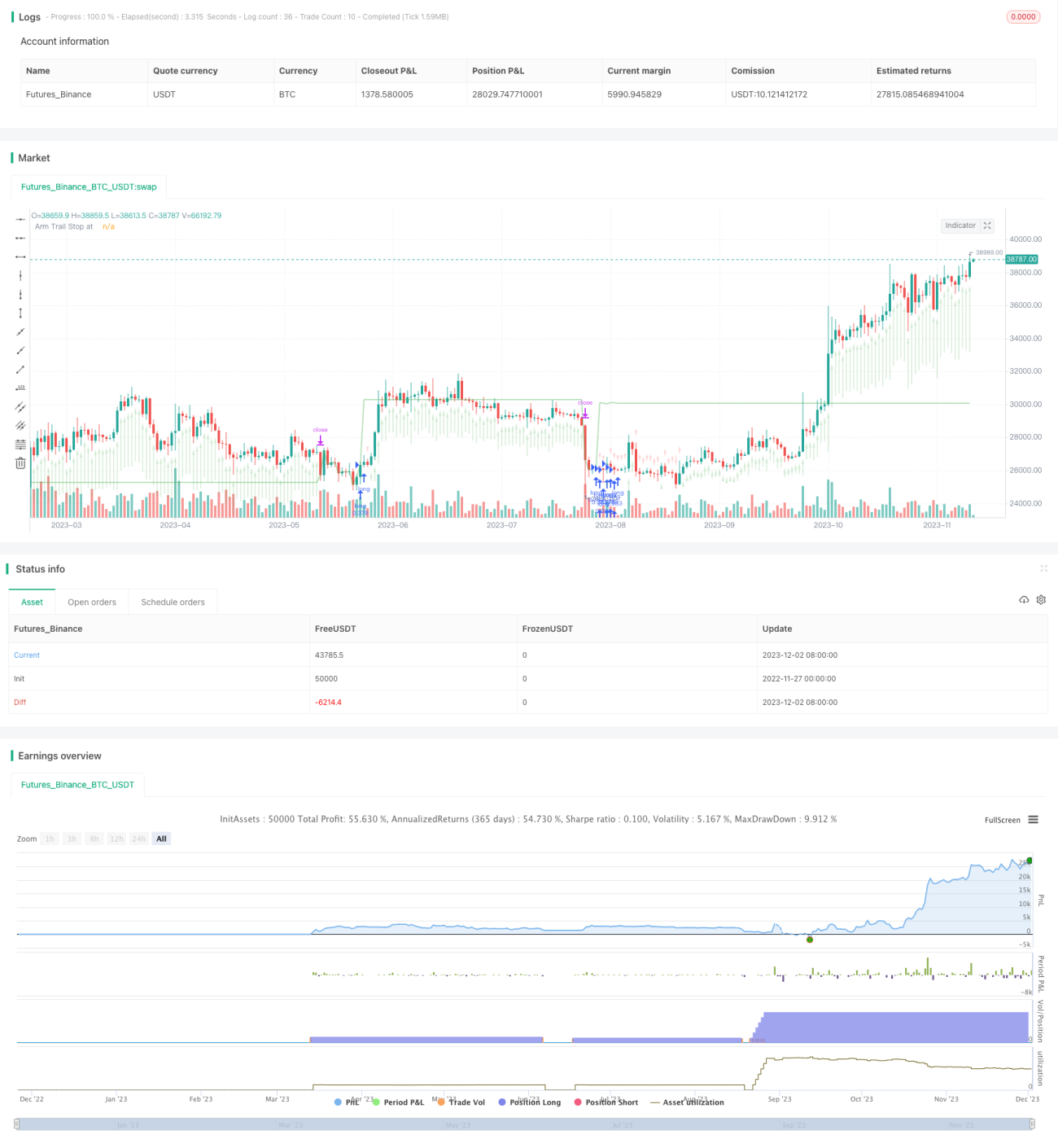

Cette stratégie est une stratégie de suivi de tendance avec stop loss basée sur l'oscillateur de flexibilité de tendance (Trend Flex Oscillator, TFO) du Dr John Ehlers et l'indicateur de la plage de variation moyenne réelle (Average True Range, ATR). Elle est conçue pour les marchés haussiers et ouvre une position longue lorsque le prix rebondit après une condition de survente (Oversold). Elle se clôture généralement en quelques jours, sauf en cas de marché baissier, où elle conserve la position. La stratégie ajuste les paramètres configurables via un backtest simple, mais les résultats de backtest ne doivent pas être considérés comme totalement fiables.

Principe de la stratégie

La stratégie combine les indicateurs TFO et ATR : elle ouvre une position longue lorsque les conditions d'achat sont remplies et la clôture lorsque les conditions de vente sont remplies.

Condition d'achat : lorsque le TFO est inférieur à un certain seuil (indiquant une condition de survente), et que la valeur du TFO de la bougie précédente est inférieure à celle de la bougie actuelle (indiquant un rebond du TFO), et que l'ATR est supérieur à un seuil de volatilité défini (indiquant une volatilité accrue du marché), les trois conditions étant remplies, une position longue est ouverte.

Condition de vente : lorsque le TFO dépasse un certain seuil (indiquant une condition de surachat) et que l'ATR dépasse le seuil défini, toutes les positions longues sont fermées. De plus, la stratégie intègre un stop loss suiveur : si le prix tombe en dessous du niveau de stop loss suiveur défini, toutes les positions longues sont également fermées. L'utilisateur peut choisir de laisser la stratégie fermer les positions en fonction des signaux des indicateurs, ou uniquement en fonction du niveau de stop loss.

La stratégie peut ouvrir jusqu'à 15 positions longues simultanément. Ses paramètres sont ajustables et peuvent être adaptés à différentes périodes.

Avantages de la stratégie

- Combine la tendance et la volatilité pour juger de la direction du marché, ce qui est relativement stable. Le TFO capte les signaux précoces de cassure de tendance, tandis que l'ATR saisit les moments de volatilité accrue.

- Dispose de paramètres d'achat/vente et de stop loss ajustables, offrant une flexibilité d'exploitation. L'utilisateur peut ajuster les paramètres en fonction du marché pour une optimisation.

- Intègre une fonction de stop loss pour réduire les pertes en cas de mouvements extrêmes. Le stop loss est un élément crucial du trading quantitatif.

- Prend en charge l'ajout de positions et la clôture partielle, permettant d'amplifier les profits en augmentant la taille des positions. Convient aux marchés haussiers.

Risques de la stratégie

- La stratégie ne fait que des positions longues, pas de ventes à découvert, et ne peut donc pas profiter des marchés baissiers. En cas de marché baissier sévère, elle peut entraîner des pertes importantes.

- Un réglage inapproprié des paramètres peut conduire à des transactions excessives ou à des occasions manquées (achats/ventes ratés). Il est nécessaire de tester plusieurs fois pour trouver la combinaison optimale de paramètres.

- En cas de conditions de marché extrêmes, le stop loss peut être inefficace et ne pas empêcher des pertes massives. C'est un problème potentiel pour toutes les stratégies avec stop loss.

- Les backtests ne reflètent pas parfaitement les conditions de trading en temps réel ; les résultats réels peuvent différer.

Optimisation de la stratégie

- On peut envisager d'ajouter une ligne de stop loss suiveur dans la condition de vente pour permettre à la stratégie de couper les pertes rapidement et de contrôler efficacement le risque de baisse.

- On peut étendre le mécanisme de vente à découvert : ouvrir une position courte lorsque le TFO s'inverse à la baisse et que l'ATR est suffisamment grand, afin que la stratégie soit adaptée aux marchés baissiers.

- On peut ajouter d'autres filtres, comme les variations de volume, pour réduire l'impact des mouvements anormaux du marché sur la stratégie.

- On peut tester les paramètres et les résultats de backtest sur différentes périodes pour trouver la meilleure combinaison de période et de paramètres.

Résumé

Cette stratégie intègre les avantages de l'analyse de tendance et de la surveillance de la volatilité, en utilisant la combinaison des indicateurs TFO et ATR pour déterminer la direction du marché. Elle intègre des mécanismes d'ajout de positions, de clôture partielle et de stop loss suiveur, permettant d'amplifier les gains et de contrôler les risques, et convient aux marchés haussiers. Elle offre également des possibilités d'optimisation extensibles, en ajoutant davantage de filtres d'indicateurs et en ajustant les paramètres pour améliorer les performances. Elle répond essentiellement aux exigences fonctionnelles de base d'une stratégie quantitative et mérite d'être étudiée et appliquée plus en profondeur.

/*backtest

start: 2022-11-27 00:00:00

end: 2023-12-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

//

// Open Source attributions:- 1