Stratégie de retournement RSI multi-facteurs

Aperçu

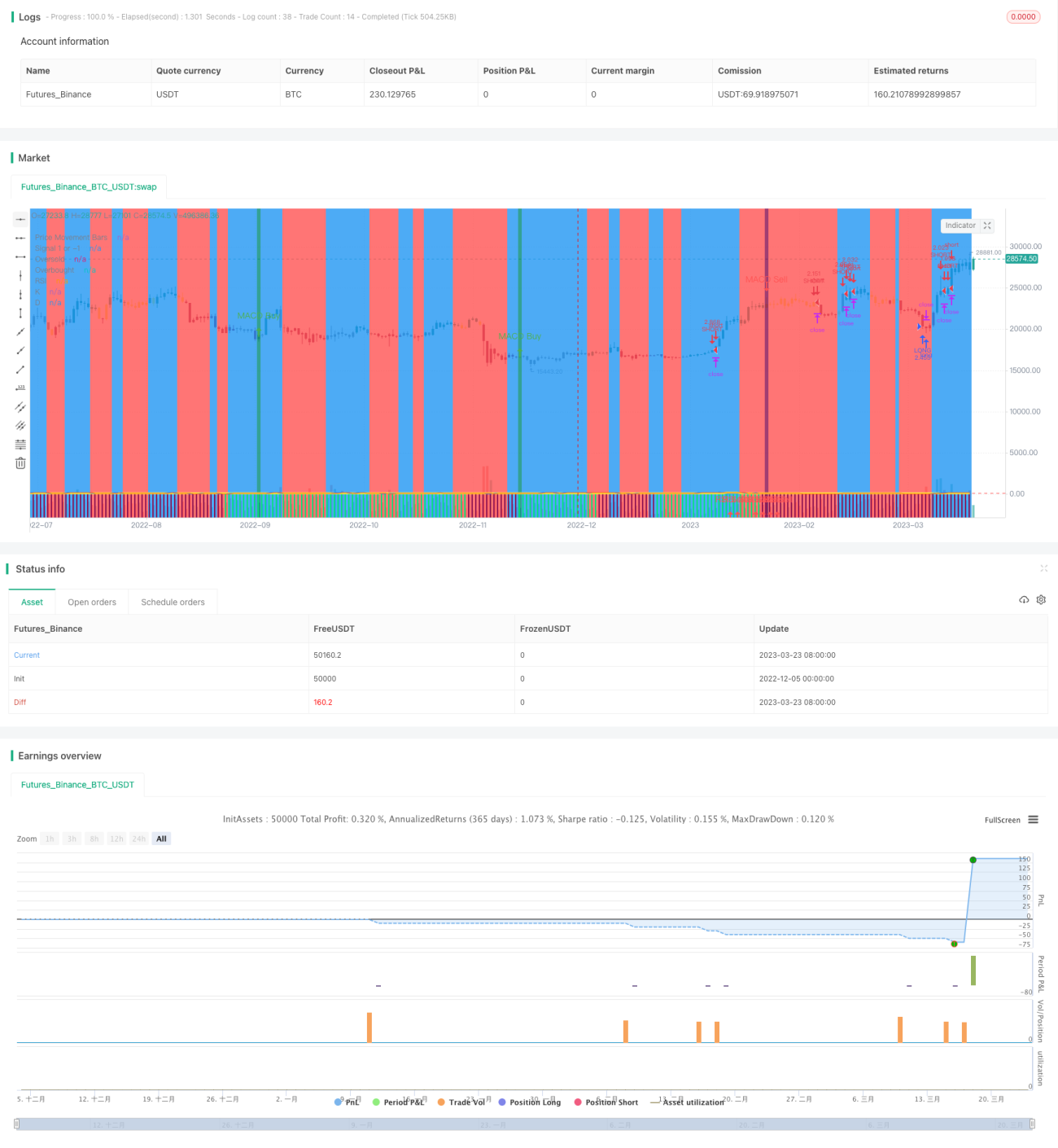

Cette stratégie utilise l'indicateur RSI pour identifier les conditions de surachat et de survente, combinée à plusieurs facteurs auxiliaires comme le MACD et l'indicateur stochastique pour les entrées en position. Il s'agit d'une stratégie de retournement visant à capturer les opportunités de retournement à court terme.

Principe de la stratégie

La stratégie utilise principalement l'indicateur RSI pour déterminer si le marché est en situation de surachat ou de survente. Lorsque le RSI dépasse le seuil de surachat défini, cela indique que le marché pourrait être en surachat, et la stratégie choisit alors de vendre à découvert. Lorsque le RSI passe en dessous du seuil de survente défini, cela indique que le marché pourrait être en survente, et la stratégie choisit alors d'acheter. Ainsi, en capturant les opportunités de trading à court terme générées lors du retournement d'un état extrême à un autre, la stratégie réalise des bénéfices.

En outre, la stratégie intègre plusieurs facteurs auxiliaires tels que le MACD et le stochastique. Ces facteurs auxiliaires servent à filtrer les éventuels faux signaux de trading. Ce n'est que lorsque l'indicateur RSI émet un signal et que les facteurs auxiliaires le confirment que la stratégie prend une décision de trading réelle. Cette combinaison multi-facteurs améliore la fiabilité des signaux de la stratégie, renforçant ainsi sa stabilité.

Analyse des avantages

Le principal atout de cette stratégie réside dans son efficacité de capture et la validation multi-facteurs qui améliore la qualité des signaux. Concrètement, cela se manifeste par les aspects suivants :

- L'indicateur RSI lui-même possède une bonne capacité à identifier les régimes de marché, permettant de détecter efficacement les situations de surachat et de survente.

- L'utilisation de plusieurs outils auxiliaires pour une validation multi-facteurs améliore la qualité des signaux et filtre un grand nombre de faux positifs.

- La stratégie est peu sensible aux paramètres et facile à optimiser.

Risques et solutions

Cette stratégie comporte également certains risques, principalement dans deux domaines :

- Risque d'échec du retournement. Les signaux de retournement reposent eux-mêmes sur des opportunités d'arbitrage statistique, et il n'est pas exclu qu'un retournement particulier échoue. Ce risque peut être contrôlé en réduisant la taille de la position ou en définissant un stop-loss.

- Risque de pertes dans un marché haussier. La stratégie reste globalement orientée vers des opérations contraires, ce qui peut entraîner des pertes dans un marché haussier. Cela nécessite une bonne évaluation de la tendance générale et, si nécessaire, une intervention manuelle pour éviter les conditions de marché défavorables.

Pistes d'optimisation

Cette stratégie doit être optimisée dans les directions suivantes :

- Tester différents instruments pour trouver la meilleure combinaison de paramètres. Bien que la stratégie soit peu sensible aux paramètres, il est recommandé de rechercher les paramètres optimaux pour chaque instrument.

- Ajouter un mécanisme de sortie adaptatif. Tester l'ajout de stop-loss dynamiques, de sortie temporelle, etc., pour rendre la stratégie plus adaptable aux changements du marché.

- Introduire des algorithmes d'apprentissage automatique. Essayer de faire apprendre au modèle la probabilité de succès d'un retournement, améliorant ainsi le taux de réussite de la stratégie.

Résumé

Globalement, cette stratégie est une stratégie de retournement à court terme. Elle utilise la capacité de l'indicateur RSI à identifier les situations de surachat et de survente, tout en s'appuyant sur plusieurs outils auxiliaires pour une validation multi-facteurs, améliorant ainsi la qualité des signaux. Cette stratégie offre une efficacité de capture élevée et une bonne stabilité. Elle mérite d'être testée et optimisée davantage pour finalement atteindre la rentabilité.

/*backtest

start: 2022-12-05 00:00:00

end: 2023-03-24 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='Ain1',title='All in One Strategy', overlay=true, initial_capital = 1000, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.18, calc_on_every_tick=true)- 1