Stratégie quantitative d'enroulement quotidien de la ligne de distraction

Aperçu

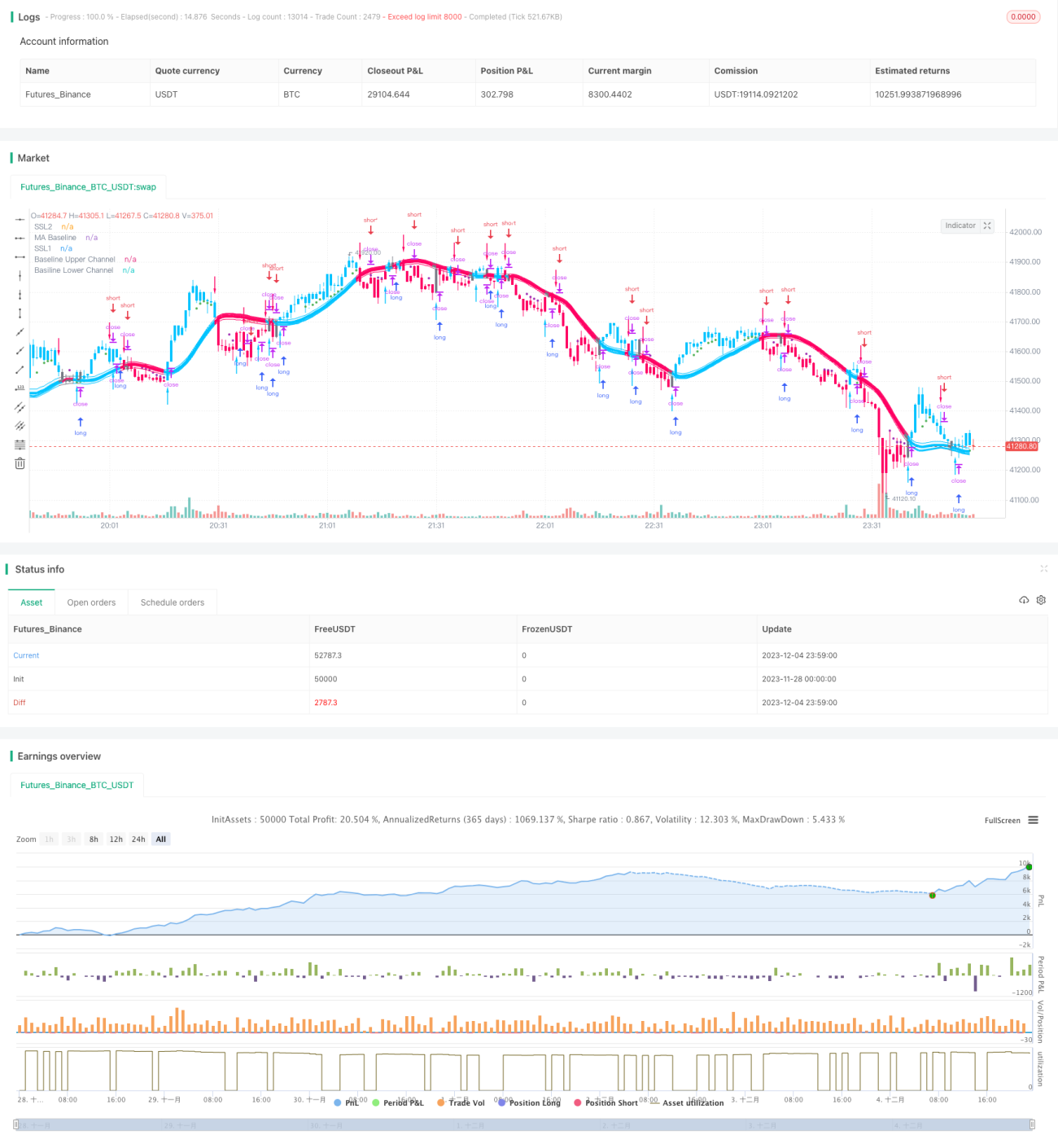

La stratégie quantitative de la ligne de distraction enveloppante quotidienne est une stratégie de trading quantitatif à court terme basée sur les moyennes mobiles et les indicateurs de prix maximum et minimum. Elle utilise les flèches EXIT de l'indicateur mixte SSL pour déterminer les points d'achat et de vente, associée à l'indicateur QQE pour filtrer, et utilise l'indicateur ATR pour calculer les niveaux de stop-loss et les positions d'ajout progressif. Cette stratégie convient aux investisseurs sensibles à la volatilité du marché et ayant un contrôle strict des risques.

Principe de la stratégie

Cette stratégie utilise les flèches EXIT de l'indicateur mixte SSL pour déterminer les points d'entrée en achat ou vente. Au-dessus de la flèche EXIT se trouve le point haut EXIT, en dessous le point bas EXIT. Lorsque le prix de clôture traverse le point haut EXIT vers le bas, un signal de vente est généré. Lorsque le prix de clôture traverse le point bas EXIT vers le haut, un signal d'achat est généré.

Pour améliorer la fiabilité des signaux, la stratégie introduit l'indicateur QQE comme condition de filtrage auxiliaire. Les signaux générés par la flèche EXIT ne sont exécutés que si l'indicateur QQE est dans la même direction.

Pour contrôler le risque, la stratégie utilise des multiples de l'indicateur ATR pour calculer les niveaux de stop-loss et les positions d'ajout progressif. Le stop-loss pour les positions courtes est prix de clôture + ATR × 1,8, pour les positions longues prix de clôture - ATR × 1,8. L'ajout se fait en trois lots, chaque lot représentant 10% du montant initial, les niveaux d'ajout sont respectivement prix de clôture - ATR × 0,1, prix de clôture - ATR × 0,3 et prix de clôture - ATR × 0,7. Chaque lot d'ajout a son propre stop-loss ; pour le premier lot, 20% du montant de la position est stoppé lorsque le seuil de stop est atteint, tandis que le reste de la position est conservé.

Avantages de la stratégie

- Bénéficier des flèches EXIT, stop-loss rapide, contrôle efficace des risques.

- Filtrage par l'indicateur QQE, améliorant la précision des signaux.

- Utilisation de l'indicateur ATR pour calculer les stops et les niveaux d'ajout en fonction de la volatilité du marché, gestion des risques plus précise.

- Ajout progressif pour bien profiter des tendances et réaliser des gains.

Risques de la stratégie

- Une position bénéficiaire atteignant un stop-loss partiel peut exposer la position restante au risque de nouveaux stops. On peut envisager un take-profit global ou un take-profit basé sur les fondamentaux de l'action elle-même.

- Les flèches EXIT et l'indicateur QQE ont des sensibilités différentes à la volatilité du marché, ce qui peut générer des signaux contradictoires. Il convient d'ajuster les paramètres pour réduire les conflits de signaux.

- Un ajout trop agressif peut entraîner des achats à des niveaux élevés et des ventes à des niveaux bas. Il faut évaluer la situation et réduire le niveau d'effet de levier.

Axes d'optimisation

- Combiner les indicateurs fondamentaux de l'action pour le take-profit, par exemple en fixant des niveaux de take-profit raisonnables basés sur le ratio valeur comptable, le PER et le taux de dividende.

- Ajuster les paramètres de l'indicateur QQE pour qu'ils soient cohérents avec les signaux générés par les flèches EXIT.

- Réduire la proportion d'ajout en fonction de la ferveur du marché, diminuer les ajouts en période de range.

- Tester la meilleure combinaison de paramètres en fonction du drawdown maximum, du ratio profit/perte, etc.

Résumé

Cette stratégie utilise les flèches EXIT de l'indicateur mixte SSL comme cœur du signal, et se sert des indicateurs QQE et ATR pour le filtrage et le stop-loss. Grâce à l'ajout progressif, elle amplifie les gains. Il s'agit d'une stratégie quantitative à court terme, adaptée pour suivre les tendances à court terme du marché. Cette stratégie offre un contrôle du drawdown et des risques, mais il faut également être attentif aux risques de conflits de signaux, d'achat à des sommets et de vente à des creux. Si l'on peut combiner des méthodes de take-profit basées sur les fondamentaux des actions, et être plus prudent dans le jugement des range et l'ajustement de la proportion d'ajout, le potentiel de profit de cette stratégie sera plus grand.

- 1