Stratégie quantitative basée sur le taux de variation du prix et les moyennes mobiles

Aperçu

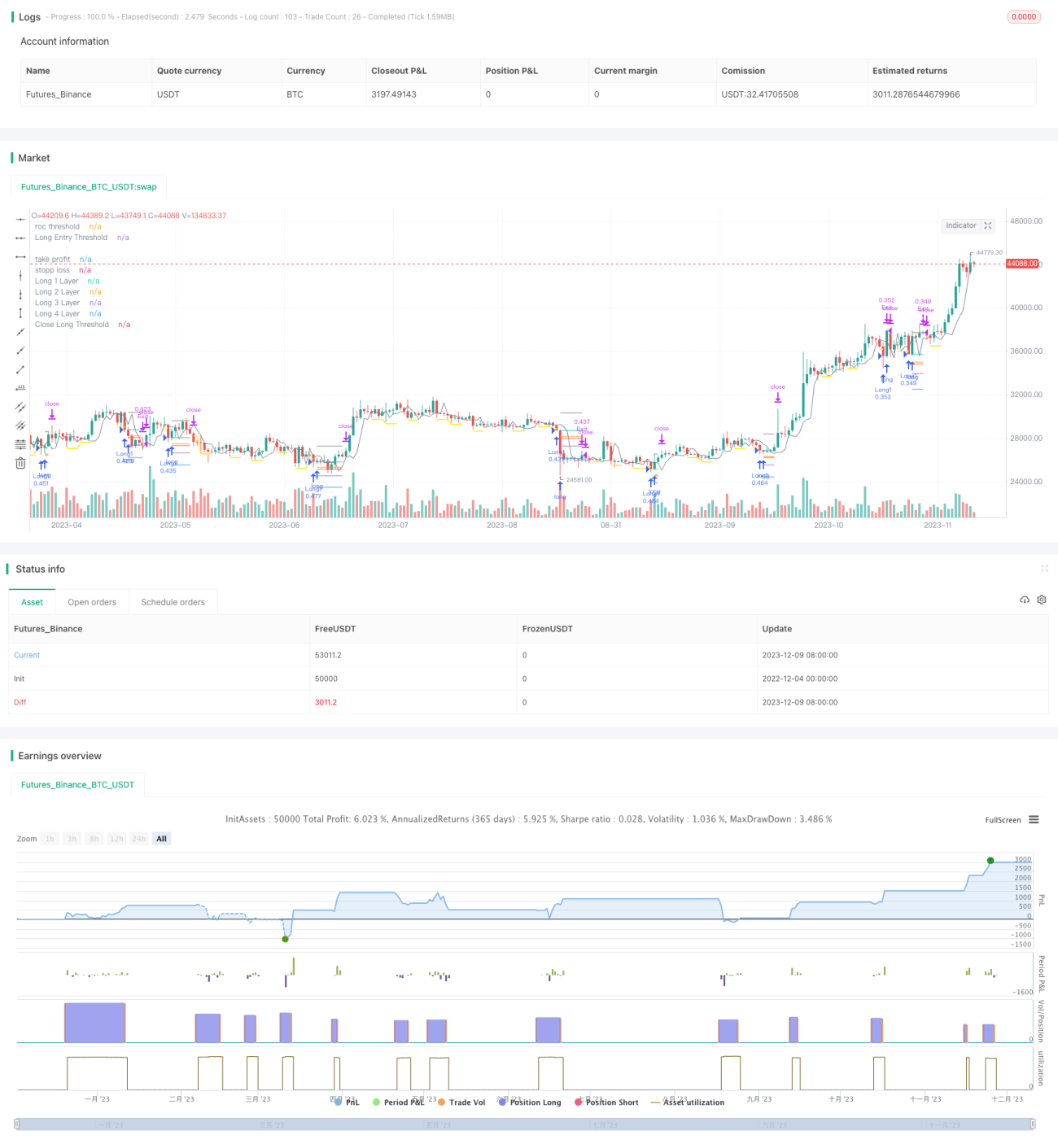

Cette stratégie combine les indicateurs techniques du taux de variation des prix et de la moyenne mobile pour réaliser un positionnement précis des points d'achat et de vente. Un seuil d'achat est établi lorsque le prix subit une baisse significative, et une position longue est ouverte lors d'une baisse supplémentaire. Un seuil de vente est établi lorsque le prix augmente, et la position est fermée lors d'une nouvelle hausse. En même temps, la stratégie utilise également une méthode d'ajout de positions, en achetant en plusieurs fois pour réduire le coût.

Principe de la stratégie

Logique d'achat

- Calculer le taux de variation des prix (ROC) et définir une ligne de seuil d'achat.

- Lorsque le prix casse en dessous de la ligne de seuil d'achat, enregistrer ce point et activer la ligne de limite d'achat.

- La ligne de limite d'achat a une durée définie par les paramètres d'entrée et se ferme après expiration.

- Lorsque le prix continue de baisser et casse en dessous de la ligne de limite d'achat, ouvrir la première position longue.

Logique de vente

- Calculer le ROC et définir une ligne de seuil de vente.

- Lorsque le prix dépasse la ligne de seuil de vente, enregistrer ce point et activer la ligne de limite de vente.

- La ligne de limite de vente a une durée définie par les paramètres et se ferme après expiration.

- Lorsque le prix continue d'augmenter et dépasse la ligne de limite de vente, fermer toutes les positions longues.

Contrôle des risques

La stratégie intègre des fonctions de stop-loss et de take-profit, avec des paramètres personnalisables, pour contrôler le risque des positions en temps réel.

Méthode d'ajout de positions

Chaque ouverture d'une position de trading définit le prix d'achat suivant selon un certain ratio basé sur les paramètres d'entrée, réalisant ainsi un effet d'achat en plusieurs fois pour ajouter des positions.

Analyse des avantages

- Utiliser l'indicateur ROC pour trouver les points d'achat et de vente ; le ROC est très sensible aux variations de prix, ce qui permet un positionnement précis.

- Utiliser la méthode de ligne de limite pour confirmer davantage le timing, évitant les fausses cassures.

- La méthode d'ajout de positions permet de suivre la valeur marchande tout en garantissant un risque contrôlable.

- Les fonctions intégrées de stop-loss et take-profit contrôlent strictement le risque de chaque position.

Risques et solutions

- En cas de forte volatilité du marché, la stratégie peut ouvrir trop de positions. La solution consiste à définir raisonnablement les paramètres d'ajout de positions et à contrôler le nombre total de positions.

- Lorsque la tendance des prix est incertaine, les niveaux de stop-loss ou take-profit peuvent être déclenchés fréquemment. On peut élargir les seuils ou désactiver cette fonction.

Suggestions d'optimisation

- Combiner avec d'autres indicateurs pour filtrer les points d'entrée. Par exemple, avec une moyenne mobile, n'accepter le ROC que lorsque le prix casse en dessous de la moyenne.

- Optimiser la logique d'ajout de positions en ne l'activant que sous certaines conditions, par exemple seulement si le prix baisse à nouveau au-delà d'un certain seuil.

- Les réglages de paramètres varient considérablement selon les instruments ; des backtests et des simulations en conditions réelles sont nécessaires pour obtenir la meilleure combinaison de paramètres.

- On peut installer un stop-loss/take-profit adaptatif, avec des niveaux variables selon la volatilité du marché.

Conclusion

Cette stratégie utilise de manière intégrée l'indicateur ROC pour un positionnement précis, la méthode des lignes de limite pour filtrer les signaux, un stop-loss/take-profit intégré pour prévenir les risques, et l'ajout de positions pour amplifier les gains. À condition que les paramètres soient bien définis, elle peut obtenir des rendements excédentaires tout en maintenant le risque dans une fourchette contrôlable. À l'avenir, on peut encore optimiser le filtrage des signaux et les mécanismes de contrôle des risques pour adapter la stratégie à davantage d'environnements de marché.

- 1