Stratégie de retournement du point le plus bas

1

Follow

1802

Followers

Aperçu

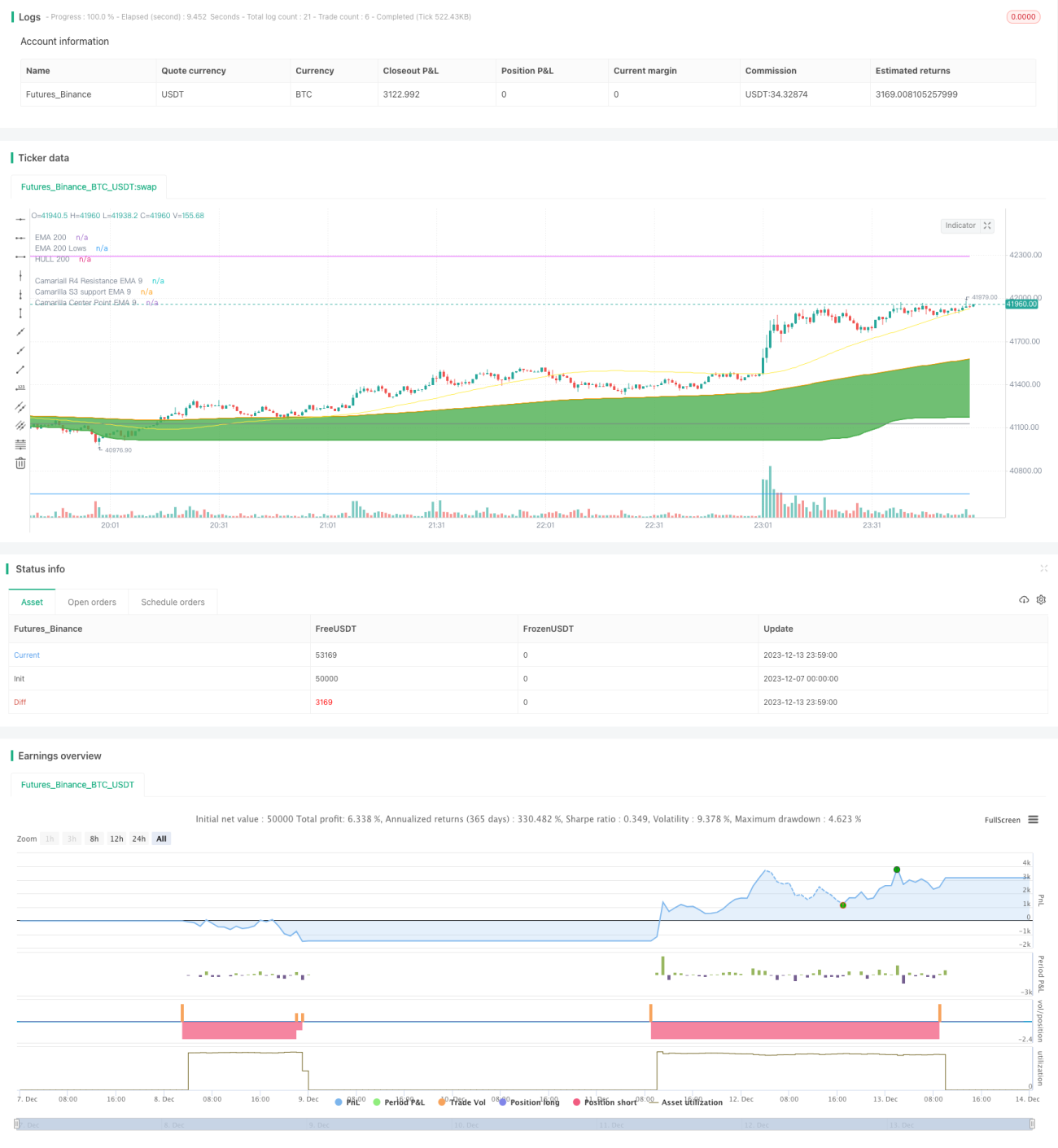

Cette stratégie est une stratégie de retournement basée sur le point le plus bas du marché. Elle utilise le plus bas de l'EMA sur 200 jours, combiné aux niveaux de support et résistance de Camarilla pour identifier le point le plus bas du marché, et passe en position longue lors du rebond des prix.

Principe de la stratégie

- Calcule le plus bas de l'EMA sur 200 jours (EMA200Lows). Lorsque le prix de clôture est inférieur à cette EMA, il est considéré comme proche du point le plus bas du marché.

- Calcule l'EMA sur 9 jours du support Camarilla 3 (S3), notée ema_s3_9, comme niveau de support important.

- Calcule également l'EMA sur 9 jours du pivot central Camarilla, notée ema_center_9, comme signal de retournement.

- Lorsque ema_center_9 croise au-dessus d'EMA200Lows, et que les 3 bougies précédentes sont toutes en dessous d'EMA200Lows, une position longue est ouverte.

- Le stop-loss utilise un stop-loss basé sur l'ATR, en suivant le plus bas mobile.

- Les objectifs de profit sont ema_h4_9 (résistance Camarilla 4) et ema_s3_9 (support Camarilla 3).

Analyse des avantages

- L'utilisation du plus bas de l'EMA sur 200 jours pour identifier la zone la plus basse du marché évite l'apparition de points plus bas en cours de route.

- La combinaison des supports Camarilla avec le pivot central permet une identification plus précise des points de retournement.

- Le stop-loss basé sur l'ATR rend le stop plus raisonnable, et le suivi du plus bas permet de verrouiller des profits plus importants.

Analyse des risques

- Le risque de détention à long terme est élevé. Cette stratégie est mieux adaptée au trading à court terme.

- En cas de forte tendance, le stop-loss peut être large. Il peut être ajusté via les paramètres de l'ATR.

- Le signal de retournement de Camarilla n'est pas fiable à 100 %, et des erreurs de jugement peuvent se produire.

Axes d'optimisation

- On peut envisager de combiner avec d'autres indicateurs, comme le RSI, pour confirmer les signaux de retournement.

- On peut étudier des ajustements de paramètres sur différents actifs pour trouver des paramètres optimaux.

- On peut tenter des méthodes d'apprentissage automatique pour ajuster dynamiquement le stop-loss ATR.

Conclusion

Cette stratégie utilise le plus bas de l'EMA et les indicateurs Camarilla pour identifier la zone la plus basse du marché et les points de retournement. Elle génère des profits via un stop-loss ATR. Dans l'ensemble, la stratégie est relativement complète et présente une certaine valeur pratique. Une optimisation ultérieure peut renforcer sa stabilité et sa fiabilité.

Source

Pine

/*backtest

start: 2023-12-07 00:00:00

end: 2023-12-14 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mohanee

//Using the lowest of low of ema200, you can find the bottomStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1