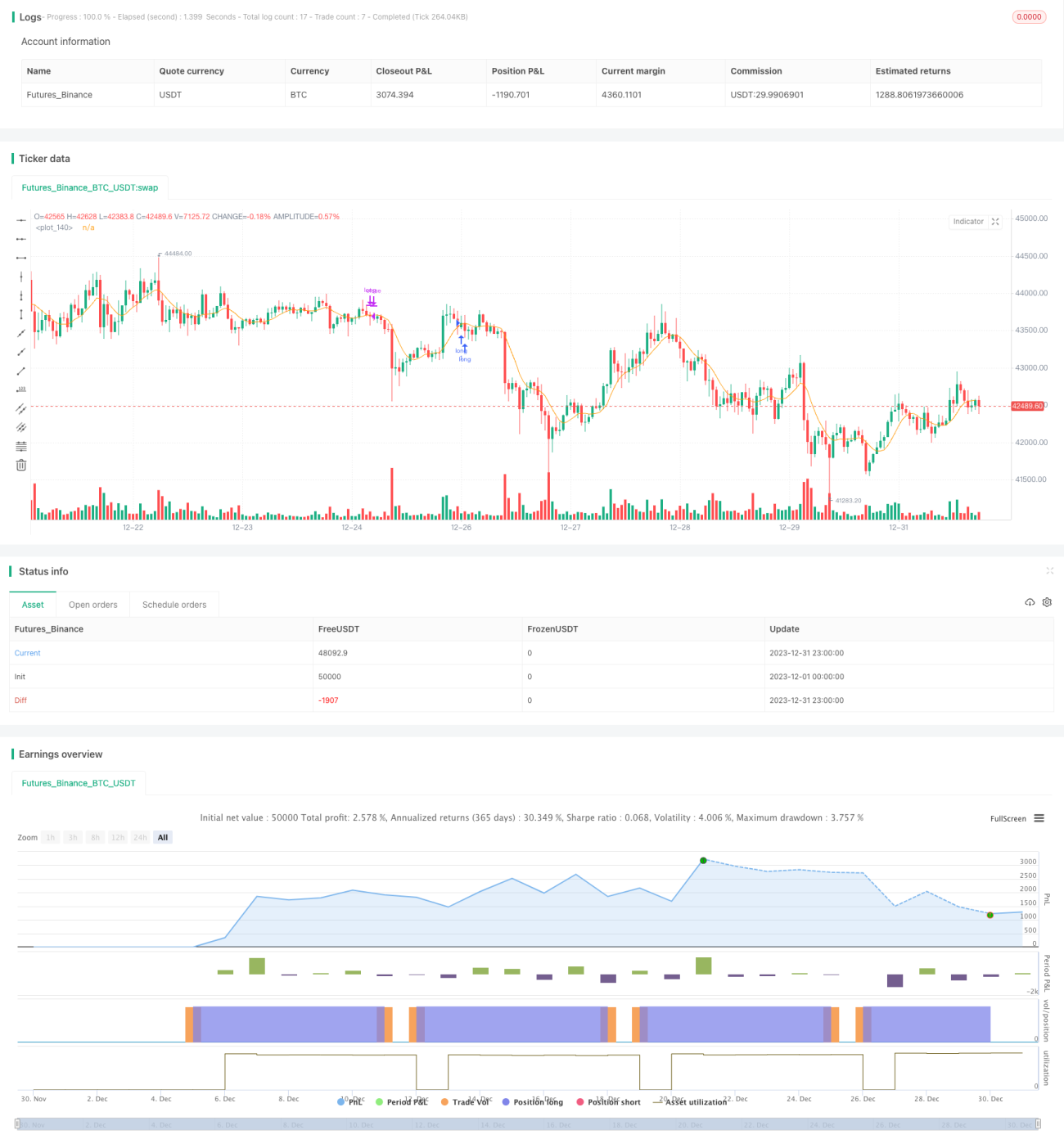

Stratégie de trading quantitatif combinant les moyennes mobiles multi-timeframe avec les horaires de trading

Aperçu

Cette stratégie utilise plusieurs indicateurs de moyennes mobiles, combinés au choix de la période de transaction pour déterminer les points d’entrée et de sortie, afin de réaliser un trading quantitatif.

Principe de la stratégie

La stratégie utilise 9 types de moyennes mobiles, dont SMA, EMA, WMA, etc. Selon le choix de l’utilisateur, pour entrer en position longue, le cours de clôture croise à la hausse la moyenne mobile sélectionnée et la bougie précédente se clôture en dessous de cette moyenne mobile ; pour entrer en position courte, le cours de clôture croise à la baisse la moyenne mobile sélectionnée et la bougie précédente se clôture au-dessus de cette moyenne mobile. Tous les ordres sont exécutés uniquement à l’ouverture du lundi. Les conditions de clôture sont un stop-profit/stop-loss fixe ou une clôture avant la fermeture du dimanche.

Analyse des avantages

Cette stratégie rassemble l’essence de plusieurs moyennes mobiles, et l’utilisateur peut choisir différents paramètres pour s’adapter à divers contextes de marché. L’entrée n’est effectuée que lorsqu’une tendance est clairement apparue, évitant ainsi les « transactions inefficaces ». De plus, la stratégie n’ouvre de positions que le lundi et les clôture (stop-profit/stop-loss ou clôture) avant le dimanche, limitant le nombre maximum d’ouvertures par semaine et contrôlant efficacement le risque de trading.

Analyse des risques

Cette stratégie repose principalement sur les indicateurs de moyennes mobiles pour juger la tendance. En cas de retournement de tendance, certaines transactions risquent d’être piégées. En outre, l’ouverture limitée au lundi uniquement empêche d’entrer sur des opportunités ultérieures survenant après le lundi, ce qui peut faire manquer une partie des profits.

Pour contrôler ces risques, il est recommandé d’utiliser des paramètres de moyennes mobiles dynamiques : lorsque le marché entre dans une phase de consolidation, réduire la période. On peut également élargir les fenêtres d’ouverture en autorisant de nouvelles positions le mercredi ou le jeudi.

Directions d’optimisation

Cette stratégie peut être optimisée selon les aspects suivants :

- Ajouter un algorithme Algerism de stop-profit/stop-loss pour ajuster dynamiquement les points de stop-profit et de stop-loss.

- Intégrer un modèle d’apprentissage automatique pour juger de la tendance annuelle et éviter d’entrer sur un marché en consolidation.

- Optimiser la logique d’ouverture et de clôture afin de permettre davantage d’opportunités d’ouverture.

Résumé

Cette stratégie intègre plusieurs indicateurs de moyennes mobiles pour déterminer la direction de la tendance. En ouvrant les positions le lundi et en les clôturant le dimanche, elle contrôle efficacement le nombre maximal de transactions par semaine. Par ailleurs, des règles strictes de stop-profit/stop-loss limitent la perte maximale par transaction. Globalement, cette stratégie est conçue de manière optimisée sous les deux dimensions du jugement de tendance et du contrôle des risques ; c’est une stratégie de trading quantitatif relativement robuste.

- 1