Stratégie quantitative combinée de la triple moyenne mobile et du MACD

Aperçu

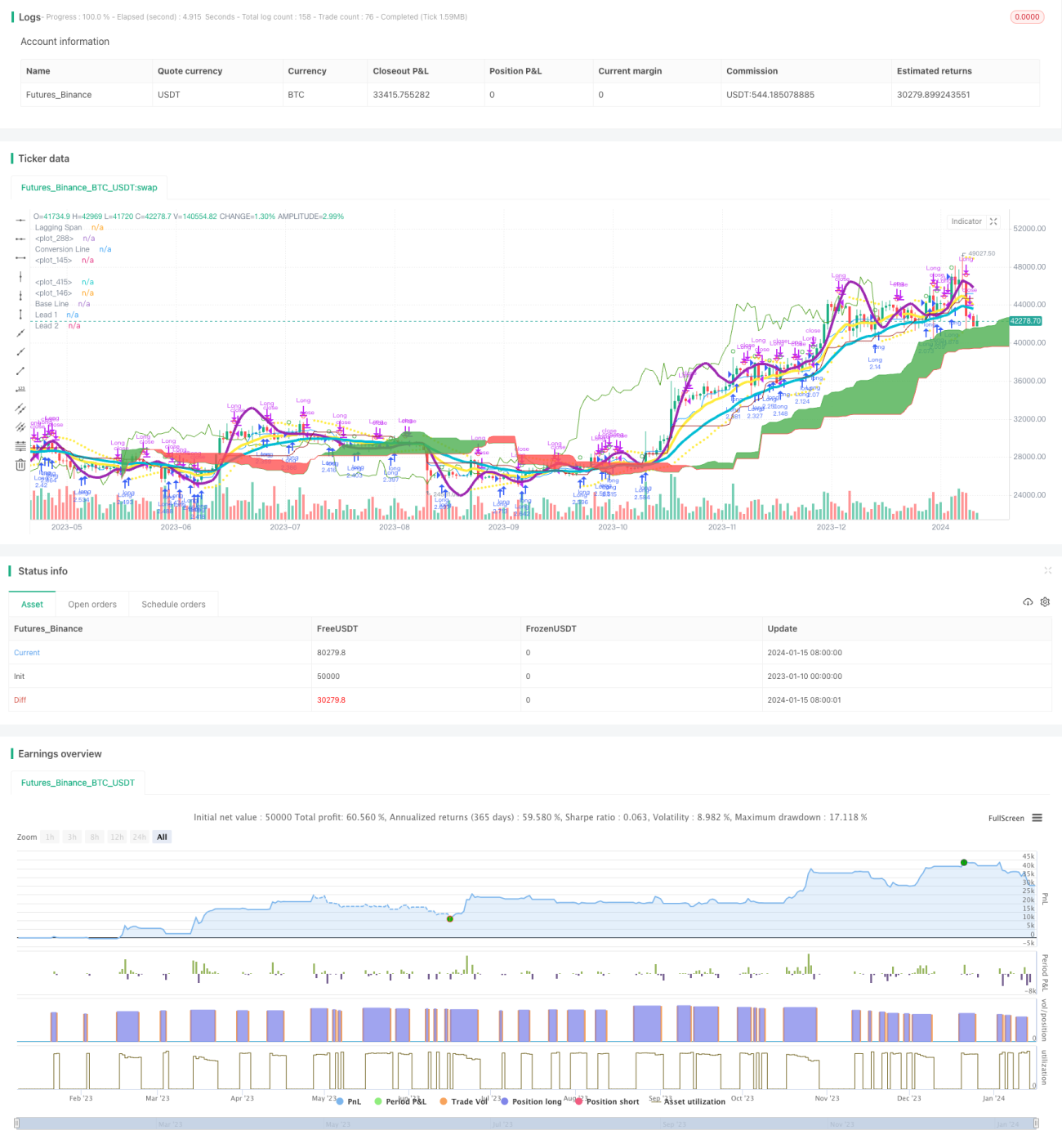

Cette stratégie développe une stratégie de trading quantitatif relativement stable et fiable en combinant l'indicateur de triple moyenne mobile et l'indicateur MACD. Elle vise à capturer les tendances futures potentielles, particulièrement adaptée aux positions à moyen et long terme.

Principe de la stratégie

Cette stratégie repose principalement sur la combinaison de la triple moyenne mobile exponentielle et de l'indicateur MACD.

Tout d'abord, la stratégie utilise des moyennes mobiles exponentielles de longueurs 3, 7 et 2. Ces trois moyennes mobiles construisent un système de moyennes mobiles allant du rapide au lent, utilisé pour déterminer la direction future de la tendance. Lorsque la moyenne mobile court terme croise au-dessus de la moyenne mobile plus long terme, il s'agit d'un signal d'achat ; lorsqu'elle croise en dessous, il s'agit d'un signal de vente.

Ensuite, la stratégie utilise également l'indicateur MACD avec des paramètres 3 et 7. Le signal d'achat est lorsque la ligne principale du MACD croise au-dessus de la ligne de signal, et le signal de vente lorsqu'elle croise en dessous.

En combinant ces deux indicateurs, on peut éviter les multiples erreurs de signaux d'un seul indicateur, améliorant ainsi la stabilité de la stratégie.

Avantages de la stratégie

- Utilisation d'un filtre double indicateur pour améliorer la qualité des signaux

- Paramètres optimisés après de multiples tests, stables et fiables

- Système de triple moyenne mobile permettant de filtrer efficacement le bruit du marché et de déterminer la tendance future

- Paramètres rapides de l'indicateur MACD permettant de capturer rapidement les opportunités à court terme

Risques de la stratégie

- Risque de drawdown et de pertes consécutives

- En l'absence de tendance claire sur le marché, la stratégie génère davantage de transactions erronées

- L'indicateur MACD peut produire des signaux erronés, nécessitant une utilisation combinée avec les moyennes mobiles

Solutions :

- Adopter une stratégie de stop loss appropriée pour limiter le drawdown maximum

- Réduire la fréquence des transactions lorsque l'état du marché est clairement sans tendance

- Optimiser les paramètres du MACD et les combiner avec d'autres indicateurs

Directions d'optimisation de la stratégie

- Tester et optimiser les paramètres des moyennes mobiles et du MACD pour trouver la meilleure combinaison

- Ajouter des indicateurs auxiliaires tels que KDJ, VRSI pour éviter les signaux erronés

- Intégrer un modèle d'apprentissage automatique pour évaluer l'état du marché et effectuer des ajustements dynamiques

- Combiner avec une stratégie de stop loss pour définir le point de stop loss optimal

Conclusion

Cette stratégie parvient à capturer les tendances de manière stable grâce à la combinaison des moyennes mobiles et du MACD. Son avantage réside dans l'utilisation combinée des indicateurs, réduisant efficacement les signaux erronés et obtenant ainsi de meilleurs résultats. Prochainement, des améliorations telles que l'optimisation des paramètres, l'introduction de stop loss et les ajustements dynamiques permettront d'affiner cette stratégie pour en faire un outil efficace dans la recherche d'opportunités à moyen et long terme.

/*backtest

start: 2023-01-10 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Matt's MACD Algo v1", shorttitle="Matt's MACD Algo v1", overlay=true, pyramiding = 0, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=7000, calc_on_order_fills = true, commission_type=strategy.commission.percent, commission_value=0, currency = currency.USD)

//study("MFI Fresh", shorttitle="MFI Fresh", overlay=true)

- 1