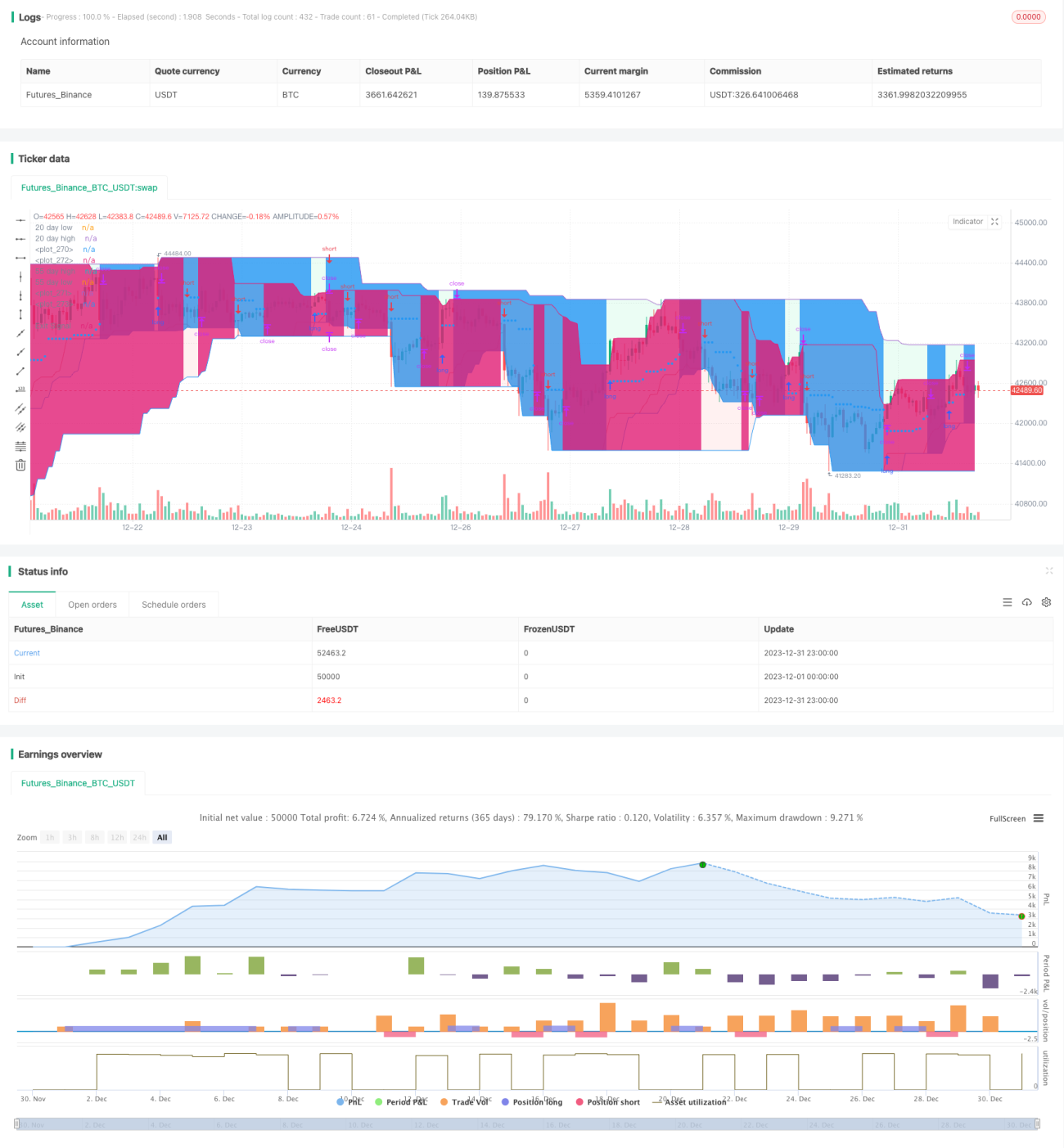

Modèle de renversement de rupture basé sur la stratégie des traders tortues

Aperçu

Cette stratégie est basée sur la célèbre « stratégie des traders de tortues », qui a été validée pendant de nombreuses années. Elle envoie des signaux d'achat et de vente, avec un maximum de 5 ordres en pyramide, ce qui signifie que la stratégie peut déclencher jusqu'à 5 ordres dans la même direction. Elle intègre une bonne gestion des risques et du capital.

Il est important de noter que cette stratégie combine deux systèmes qui fonctionnent ensemble (S1 et S2).

Principe de la stratégie

La taille des positions est très importante pour les traders de tortues afin de gérer correctement le risque. Cette stratégie de dimensionnement des positions s'adapte à la volatilité du marché et au compte (gains et pertes). Elle est basée sur l'ATR (Average True Range), également appelé « N ». Sa longueur par défaut est de 20.

Le nombre d'unités à acheter est :

unit = (percentage_to_risk/100)*account/atr*syminfo.pointvalue

Selon votre tolérance au risque, vous pouvez augmenter le pourcentage du compte, mais par défaut les traders de tortues utilisent 1 %. Si vous traitez des contrats, l'unité doit être arrondie à l'entier inférieur par défaut.

Une règle supplémentaire est ajoutée pour réduire le risque lorsque la valeur du compte devient inférieure au capital initial : dans ce cas, dans la formule de l'unité, il faut remplacer par :

account := (strategy.equity-strategy.openprofit)*(strategy.equity-strategy.openprofit)/strategy.initial_capital

Deux systèmes travaillent ensemble :

Un breakout (dépassement) est un nouveau plus haut ou un nouveau plus bas. S'il s'agit d'un nouveau plus haut, on ouvre une position longue ; inversement, s'il s'agit d'un nouveau plus bas, on entre en position courte.

Nous ajoutons une règle supplémentaire :

Cette règle supplémentaire permet au trader de participer à la tendance principale si le signal du système 1 a été sauté. Si le signal du système 1 est sauté et que la bougie suivante est également un nouveau breakout sur 20 jours, alors S1 n'émettra pas de signal. Il faut attendre un signal S2 ou une bougie qui ne produit pas de nouveau breakout pour réactiver S1.

Analyse des avantages

La stratégie des tortues permet d'ajouter des unités supplémentaires à une position lorsque le prix évolue en notre faveur. J'ai configuré la stratégie pour permettre jusqu'à 5 ordres dans la même direction. Ainsi, si le prix s'écarte de notre point d'entrée, nous ajoutons des unités.

Nous définissons le premier ordre (long ou court) comme l'ordre maximal. Les ordres pyramidaux suivants comporteront moins d'unités que le premier ordre.

Nous avons fixé un stop-loss maximum de 10 % pour le premier ordre, ce qui signifie que vous ne pouvez pas perdre plus de 10 % de la valeur du premier ordre. Cependant, comme le stop-loss augmente/diminue de 0,5 * ATR(20), vos ordres pyramidaux peuvent perdre davantage, et dans ce cas la perte ne sera pas garantie en dessous de 10 %. Le risque reste bien géré car ces ordres ont une valeur inférieure à celle du premier ordre.

Analyse des risques

Le plus grand risque de cette stratégie est une position trop importante. Étant donné que les ordres sont passés au marché, si plusieurs ordres de grande taille sont passés simultanément, cela peut avoir un impact important sur le cours et provoquer des glissements de prix importants, entraînant des pertes financières majeures.

Un autre risque est une mauvaise configuration de la gestion du capital. Par exemple, un stop-loss mal configuré ou un pourcentage trop élevé peut entraîner des pertes massives. Il est nécessaire de configurer soigneusement en fonction de sa propre tolérance au risque.

Axes d'optimisation

La stratégie peut être optimisée sur les aspects suivants :

-

Tester l'impact de différents paramètres sur le rendement et le ratio de Sharpe, comme la période de l'ATR, le multiple de l'ATR pour le stop-loss, etc. Trouver la combinaison de paramètres optimale.

-

Tester différentes règles d'entrée et de sortie. Par exemple, utiliser des figures de chandeliers comme filtre supplémentaire.

-

Essayer d'autres types de stop-loss, comme le trailing stop ou le stop dynamique. Cela pourrait réduire la probabilité que le stop soit déclenché.

-

Tester différents nombres d'ordres pyramidaux. Plus il y a d'ordres, plus l'effet de levier et le risque sont élevés. Trouver le point d'équilibre optimal.

-

Essayer d'arrêter le trading pendant certaines périodes (par exemple, avant la publication des chiffres de l'emploi non agricole américain) pour éviter l'impact d'événements majeurs.

Résumé

Dans l'ensemble, cette stratégie offre un bon équilibre risque-rendement et convient au trading de tendance à moyen et long terme. Elle présente des avantages tels qu'un système de trading automatisé et un risque contrôlable. Grâce à l'optimisation, la stabilité et le rendement de la stratégie peuvent être encore améliorés.

- 1