Stratégie de suivi de tendance multi-indicateurs

Aperçu

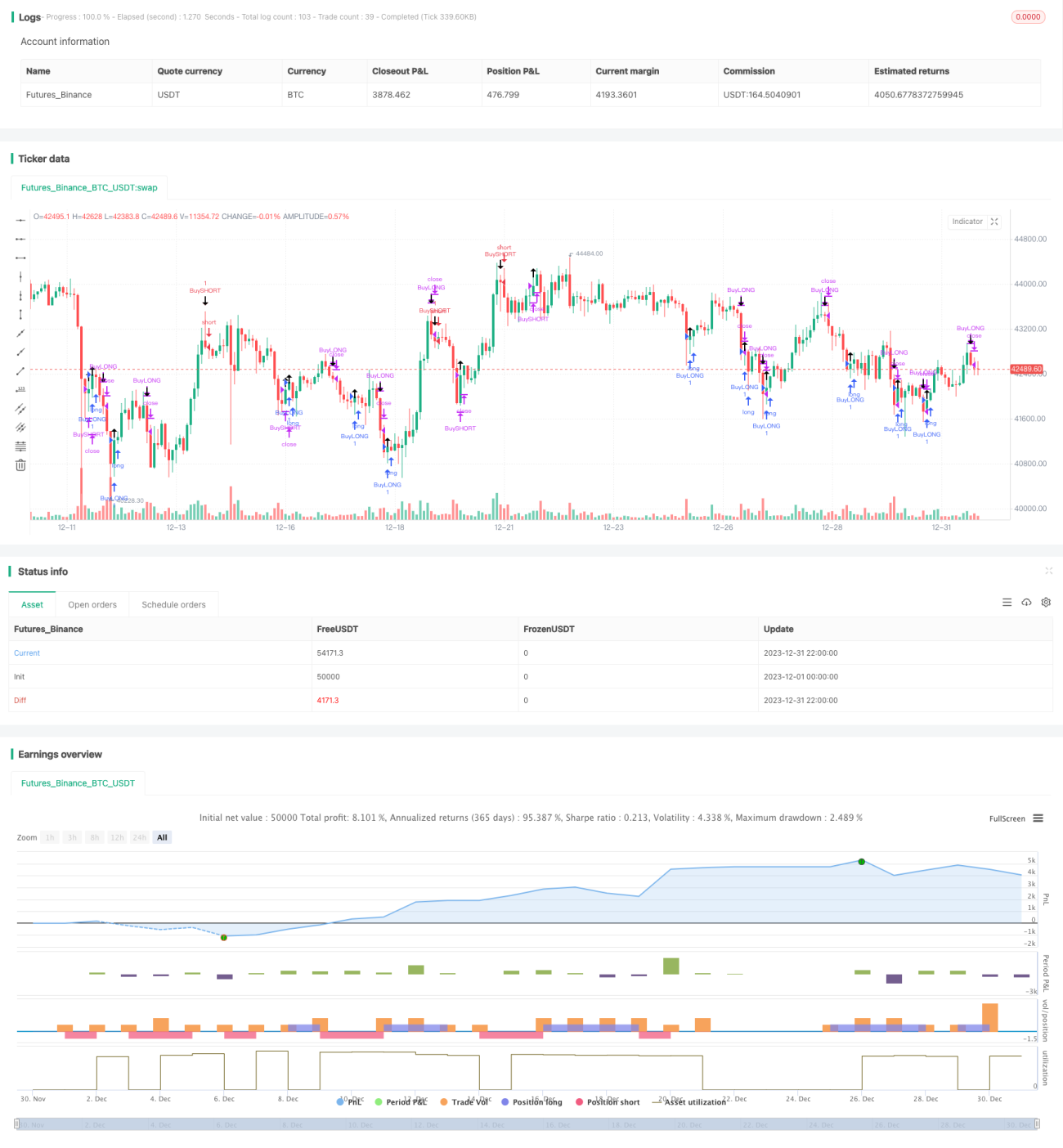

Cette stratégie combine plusieurs indicateurs pour identifier la tendance et met en place un stop suiveur de tendance afin de verrouiller les profits. Elle utilise principalement les bandes de Bollinger, le RSI et l'ADX pour déterminer les points d'entrée, ainsi que l'ATR et les bandes de Bollinger pour le stop.

Principe de la stratégie

Les principaux indicateurs de la stratégie sont les bandes de Bollinger, le RSI et l'ADX. Lorsque le prix s'approche de la bande inférieure de Bollinger et que le RSI est inférieur à 30, la situation est jugée comme survendue : on prend une position longue. Lorsque le prix s'approche de la bande supérieure de Bollinger et que le RSI est supérieur à 70, la situation est jugée comme surachetée : on prend une position courte. De plus, si l'ADX est supérieur à 25, on considère qu'une tendance est formée, ce qui renforce la validité des signaux long et short.

Après l'ouverture de la position, la stratégie utilise l'ATR et les bandes de Bollinger pour définir le stop. Concrètement, l'ATR sert à déterminer la distance maximale de stop ; lorsque le prix atteint ce niveau, le stop est déclenché. Les bandes de Bollinger (supérieure et inférieure) sont utilisées pour définir un stop suiveur, mis à jour en temps réel en fonction de l'évolution du prix.

Analyse des avantages

Cette stratégie combine plusieurs indicateurs pour identifier efficacement la tendance et utilise un mécanisme de stop pour verrouiller les profits tout en réduisant le risque de perte. Il s'agit d'une stratégie relativement robuste. Ses principaux avantages sont les suivants :

- L'utilisation des bandes de Bollinger pour détecter les situations de surachat/survente permet d'identifier les retournements potentiels.

- L'ajout du RSI améliore la précision des signaux.

- L'ADX confirme la formation d'une tendance, garantissant la direction correcte des transactions.

- Le stop suiveur basé sur l'ATR et les bandes de Bollinger permet de maximiser le verrouillage des profits.

Analyse des risques

Cette stratégie comporte également certains risques :

- L'utilisation de multiples indicateurs rend les paramètres sujets au surajustement (overfitting).

- Lorsque l'intervalle des bandes de Bollinger est large, les signaux de surachat/survente perdent en efficacité.

- Un stop suiveur mal calibré peut entraîner des pertes accrues.

Pour faire face à ces risques, nous pouvons prendre les mesures suivantes :

- Optimiser les paramètres avec plusieurs combinaisons pour éviter le surajustement.

- Ajuster les paramètres des bandes de Bollinger en fonction de la volatilité du marché.

- Tester différentes distances de stop pour s'assurer qu'elles supportent les fluctuations normales.

Pistes d'optimisation

Cette stratégie peut être améliorée dans les directions suivantes :

- Ajouter un contrôle de la taille de la position en fonction du multiplicateur de stop.

- Intégrer un module de money management pour limiter strictement la perte unitaire.

- Tester d'autres indicateurs de stop, comme le DMI, l'Envelopes, etc.

- Intégrer un modèle d'apprentissage automatique pour estimer la probabilité de tendance et améliorer l'efficacité.

Résumé

Dans l'ensemble, cette stratégie est une stratégie de suivi de tendance relativement robuste. En déterminant la direction de la tendance via de multiples indicateurs et en contrôlant le risque avec des stops, elle peut obtenir un bon rendement. Nous avons également proposé plusieurs pistes d'optimisation qui, si elles sont mises en œuvre, pourraient encore améliorer ses performances.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1