Stratégie de stop-loss de suivi de tendance RSI

Aperçu

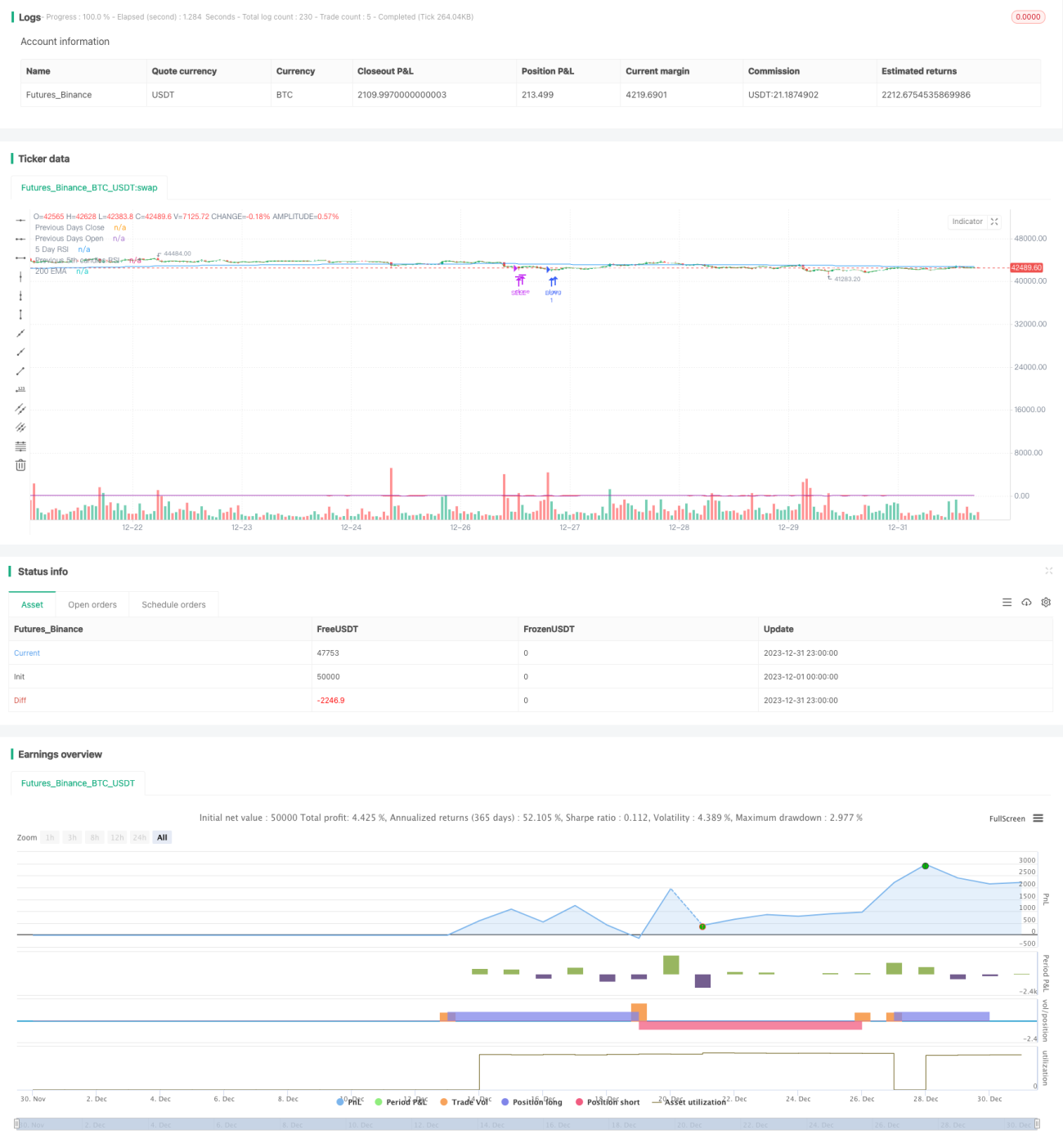

Il s'agit d'une stratégie de trading quantitatif utilisant l'indicateur RSI pour déterminer la tendance et définir des stop-loss et take-profit. Cette stratégie combine l'indicateur RSI pour évaluer la direction du marché, ainsi que des stop-loss et take-profit dynamiques afin de verrouiller les profits et de minimiser les risques.

Principe de la stratégie

La stratégie utilise principalement l'indicateur RSI pour déterminer la direction du marché et décider d'acheter ou de vendre à découvert. Lorsque le RSI franchit à la hausse le seuil bas, le marché est considéré comme étant dans une tendance haussière, et l'on achète (position longue). Lorsque le RSI franchit à la baisse le seuil haut, le marché est considéré comme étant dans une tendance baissière, et l'on vend à découvert (position courte).

Parallèlement, la stratégie suit le prix d'ouverture de chaque ordre et définit un stop-loss et un take-profit flottants. Pour les positions longues, un stop-loss est fixé à un certain pourcentage du prix d'ouverture ; pour les positions courtes, un take-profit est fixé à un certain pourcentage du prix d'ouverture. Lorsque le prix atteint ces niveaux, la stratégie ferme automatiquement la position pour limiter les pertes ou verrouiller les profits.

Avantages de la stratégie

- Utilisation de l'indicateur RSI pour déterminer la direction du marché, évitant les transactions en range.

- Définition de stop-loss et take-profit flottants, permettant de verrouiller les profits de manière flexible et de contrôler efficacement les risques.

- Les paramètres RSI et les pourcentages de stop-loss/take-profit peuvent être ajustés et optimisés via des entrées externes.

Risques de la stratégie

- L'indicateur RSI présente un certain retard et peut manquer des points de retournement de tendance à court terme.

- Si les niveaux de stop-loss/take-profit sont trop proches, ils risquent d'être déclenchés accidentellement.

Pistes d'optimisation

- Tester l'efficacité de l'indicateur RSI sur différentes périodes.

- Tester différentes combinaisons de paramètres pour trouver le ratio stop-loss/take-profit optimal.

- Ajouter des indicateurs supplémentaires pour filtrer les signaux.

Résumé

Dans l'ensemble, cette stratégie est une stratégie de trading quantitatif qui suit la tendance à l'aide du RSI et l'accompagne de stop-loss et take-profit flottants. Comparée à une stratégie basée sur un seul indicateur, elle gère mieux les risques et permet de verrouiller efficacement les profits. Ses performances peuvent être améliorées par l'optimisation des paramètres et l'ajout d'indicateurs auxiliaires.

- 1