Stratégie de la moyenne mobile à enveloppe dynamique

Aperçu

Cette stratégie repose sur une moyenne mobile et une enveloppe dynamique pour exécuter des transactions longues et courtes. Elle suit les cassures des bornes haute et basse de l'enveloppe pour ouvrir des positions et les ferme lorsque le prix repasse en dessous de la moyenne de référence. Elle convient aux actions et aux cryptomonnaies présentant des tendances marquées.

Principe de la stratégie

Tout d'abord, la stratégie calcule une moyenne de référence en fonction du type et de la longueur de moyenne mobile choisis par l'utilisateur. Les moyennes courantes incluent la SMA, l'EMA, etc.

Ensuite, en fonction du paramètre de pourcentage défini par l'utilisateur, l'enveloppe supérieure et inférieure sont calculées. Par exemple, 5 % signifie qu'une transaction est déclenchée lorsque le prix dépasse 105 % de la bande autorisée. Le nombre d'enveloppes peut être personnalisé.

Règles d'entrée : si le prix casse l'enveloppe inférieure, on prend une position longue ; s'il casse l'enveloppe supérieure, on prend une position courte. La règle est très simple et claire.

Enfin, lorsque le prix repasse en dessous de la moyenne de référence, toutes les positions sont fermées. C'est un point de sortie lié au suivi de tendance.

Il est à noter que cette stratégie met en œuvre un fractionnement des positions. S'il y a plusieurs enveloppes, le capital est alloué proportionnellement. Cela évite le risque d'un pari unilatéral.

Analyse des avantages

La stratégie présente les principaux avantages suivants :

-

Elle assure un suivi automatique de la tendance. L'utilisation d'une moyenne mobile pour déterminer la direction de la tendance est très courante, ce qui en fait une méthode éprouvée.

-

L'enveloppe permet de filtrer une partie du bruit, évitant ainsi des transactions excessives dues à une trop grande sensibilité. Un paramétrage approprié peut considérablement optimiser la rentabilité de la stratégie.

-

Le fractionnement des positions renforce la résilience de la stratégie. Même si une cassure unilatérale échoue, d'autres directions peuvent continuer à bien fonctionner. Cela optimise le rapport risque/rendement global.

-

La possibilité de personnaliser le type de moyenne et le nombre d'enveloppes accroît la flexibilité de la stratégie, permettant aux utilisateurs d'optimiser les paramètres pour différents instruments.

Analyse des risques

Les principaux risques de la stratégie sont les suivants :

-

Le système de moyennes mobiles est peu sensible aux signaux de croisement doré (golden cross). En l'absence de tendance claire, la stratégie peut manquer certaines opportunités.

-

Un réglage trop large des enveloppes peut augmenter le nombre de transactions et le risque de glissement. À l'inverse, des enveloppes trop serrées peuvent faire passer à côté de mouvements importants. Trouver le bon équilibre nécessite des tests approfondis.

-

Dans un marché en range (oscillations), la stratégie risque de se retrouver souvent en position perdante. Il est donc préférable de la réserver aux instruments présentant des tendances marquées.

-

Le fractionnement des positions limite le gain par trade. Pour rechercher un risque unilatéral, des optimisations supplémentaires sont nécessaires.

Pistes d'optimisation

La stratégie peut être améliorée dans les directions suivantes :

-

Remplacer les indicateurs de déclenchement pour l'ouverture et la fermeture de positions (par exemple, l'indicateur KDJ) ou combiner plusieurs indicateurs comme filtres.

-

Ajouter des logiques de take profit et stop loss pour verrouiller une partie des bénéfices et gérer activement les risques.

-

Optimiser les paramètres afin de trouver la meilleure combinaison de moyenne mobile et d'enveloppe. Cela nécessite des backtests approfondis pour identifier la paire de paramètres optimale.

-

Intégrer des techniques comme le deep learning pour une optimisation intelligente des paramètres, en apprenant et en mettant à jour les réglages au fil du temps.

-

Tenir compte des différences entre instruments et marchés en définissant plusieurs jeux de paramètres adaptés à différents environnements de trading. Cela renforcera considérablement la stabilité de la stratégie.

Résumé

Dans l'ensemble, cette stratégie de moyenne mobile avec enveloppe dynamique est très adaptée au trading de tendance. Elle est simple, efficace, facile à comprendre et à optimiser. En tant que stratégie de base, elle offre une grande plasticité et extensibilité. En la fusionnant avec des systèmes plus complexes, on peut encore améliorer le rendement global et les indicateurs de risque ajusté. Elle constitue donc un excellent socle pour le trading quantitatif.

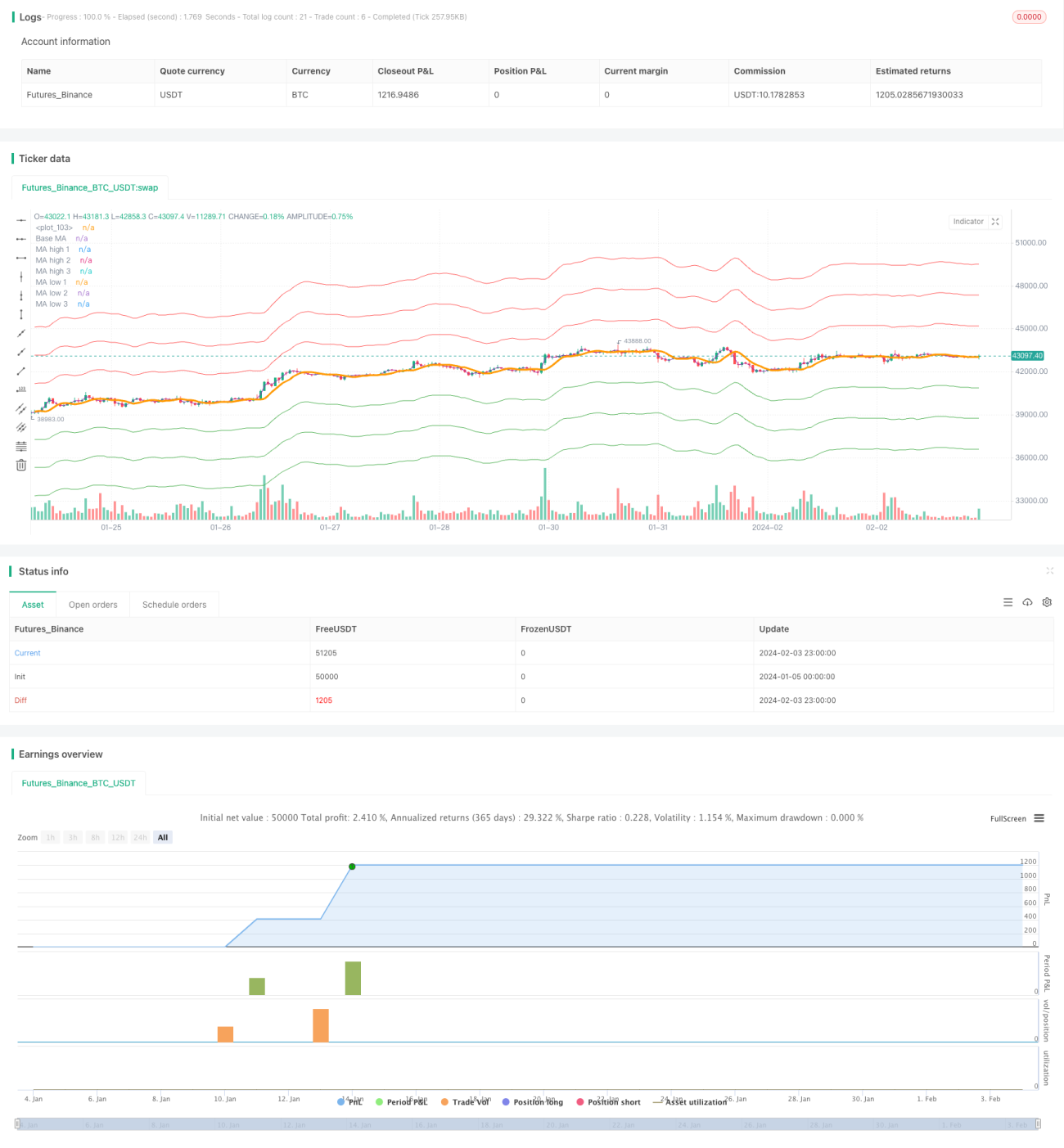

/*backtest

start: 2024-01-05 00:00:00

end: 2024-02-04 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Envelope Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100, initial_capital=1000, pyramiding = 5, commission_type=strategy.commission.percent, commission_value=0.0)

// CopyRight Crypto Robot- 1