Stratégie de suivi de profil oscillant adaptatif multi-périodes

Aperçu

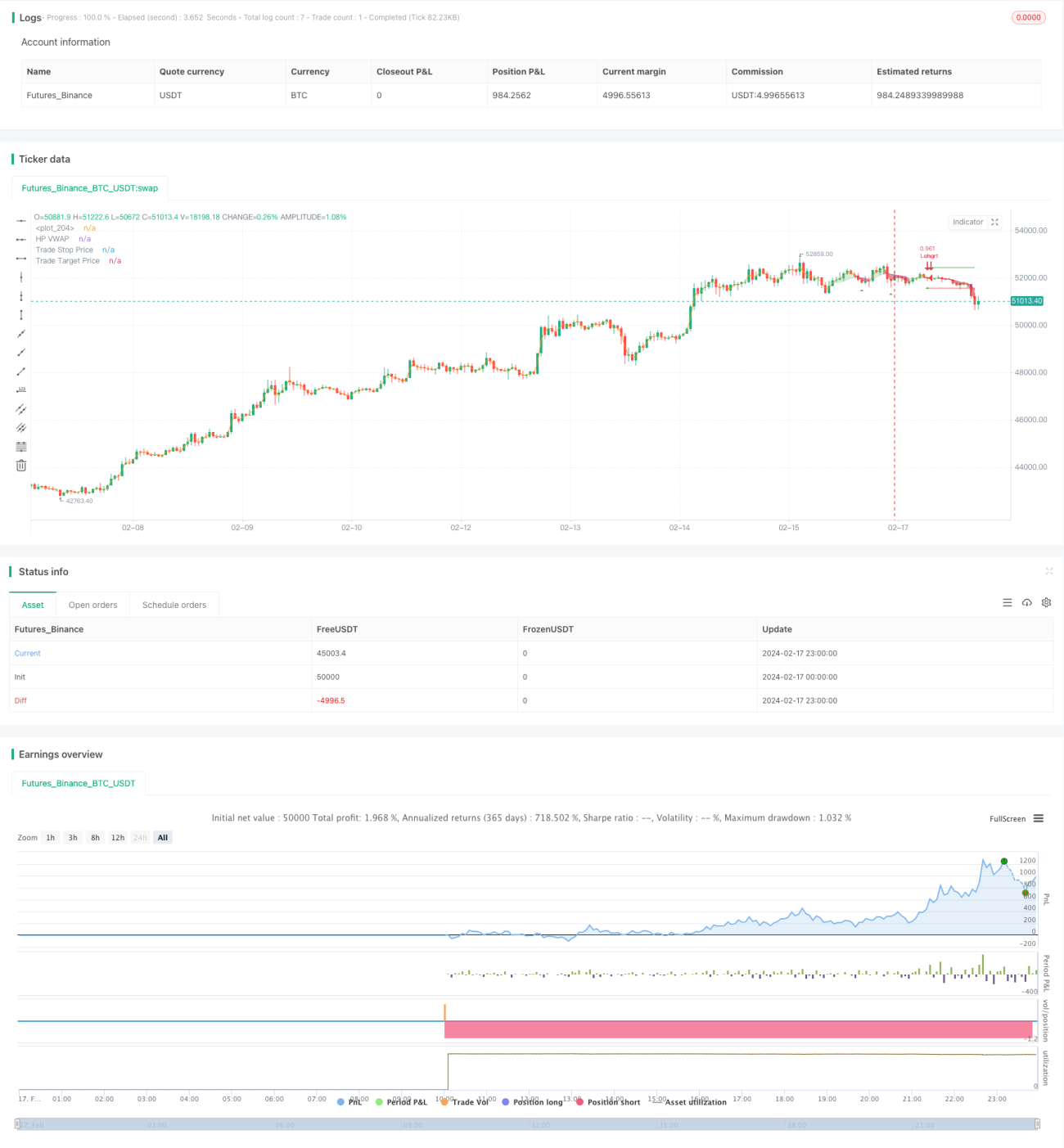

Cette stratégie utilise le filtre Hodrick-Prescott (HP) pour lisser les prix et extraire la tendance des prix. Ensuite, elle calcule un prix moyen pondéré par le volume (VWAP) personnalisé basé sur une période définie par l'utilisateur. Lorsque le prix est supérieur à la ligne de tendance, une position longue est prise ; lorsqu'il est inférieur, une position courte est prise. Un stop-loss basé sur l'ATR est également intégré pour garantir un risque contrôlé.

Principe de la stratégie

-

Utilisation du filtre HP pour extraire la ligne de tendance des prix. Le filtre HP extrait la composante de long terme des prix par une méthode d'optimisation, en filtrant les fluctuations à court terme.

-

Calcul du VWAP sur une période définie par l'utilisateur. Le VWAP reflète plus précisément le prix moyen sur différentes périodes.

-

Lorsque le prix est au-dessus de la ligne de tendance HP, la condition d'achat est remplie ; lorsqu'il est en dessous, la condition de vente est remplie. Cela permet de capter les cassures à la hausse ou à la baisse.

-

Le stop-loss ATR permet de prendre un risque raisonnable et d'éviter des pertes excessives.

Analyse des avantages

-

L'extraction de la tendance par le filtre HP est plus lisse que des indicateurs comme la MA, évitant d'être trompé par les fluctuations à court terme.

-

Personnalisation de la période VWAP, offrant une plus grande flexibilité pour s'adapter aux cycles du marché.

-

Trading dans le sens de la tendance, conforme à la philosophie du suivi de tendance, avec un taux de réussite plus élevé.

-

Le stop-loss ATR contrôle la perte par transaction, évitant des pertes trop importantes.

-

Plusieurs paramètres réglables, permettant une optimisation pour différents marchés.

Risques et contre-mesures

-

En cas de marché en range (sideways), le stop-loss peut être déclenché fréquemment. Il est possible d'élargir la plage du stop-loss.

-

En fin de tendance, des retracements ou des cassures test peuvent piéger la stratégie. Il convient d'utiliser d'autres indicateurs pour repérer la fin de tendance et de fermer les positions rapidement.

-

Un réglage inapproprié de la période VWAP peut manquer des opportunités de trading plus efficaces. Il est conseillé d'ajuster dynamiquement la période VWAP en fonction des indicateurs de tendance.

Pistes d'optimisation

-

Le paramètre λ du filtre HP ajuste la force du lissage. Une valeur λ élevée rend la ligne de tendance plus lisse, mieux adaptée aux tendances de long terme ; une valeur λ faible la rend plus réactive aux changements de prix, mieux adaptée aux opportunités à moyen/court terme.

-

Le multiple ATR ajuste la plage du stop-loss. Il peut être optimisé avec λ : avec λ élevé, élargir la plage du stop-loss ; avec λ faible, la réduire pour verrouiller plus de profits.

-

Le ratio risque/récompense (R:R) impacte directement le ratio gain/perte. Il est possible de tester différents multiples pour évaluer le contrôle du drawdown et la rentabilité.

Résumé

Cette stratégie est conçue selon une approche de suivi de tendance. Grâce à plusieurs paramètres, elle peut être optimisée pour différentes périodes (long, moyen, court terme) avec un taux de réussite et une rentabilité élevés. La gestion des risques est également prise en compte pour éviter des pertes excessives par transaction. Globalement, cette stratégie utilise une méthode scientifique pour extraire les caractéristiques de tendance des prix, et sa flexibilité paramétrique lui confère un bon potentiel d'application.

/*backtest

start: 2024-02-17 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tathal animouse hajixde

//@version=4- 1