Stratégie Ichimoku Cloud Nine pour le trading

Aperçu

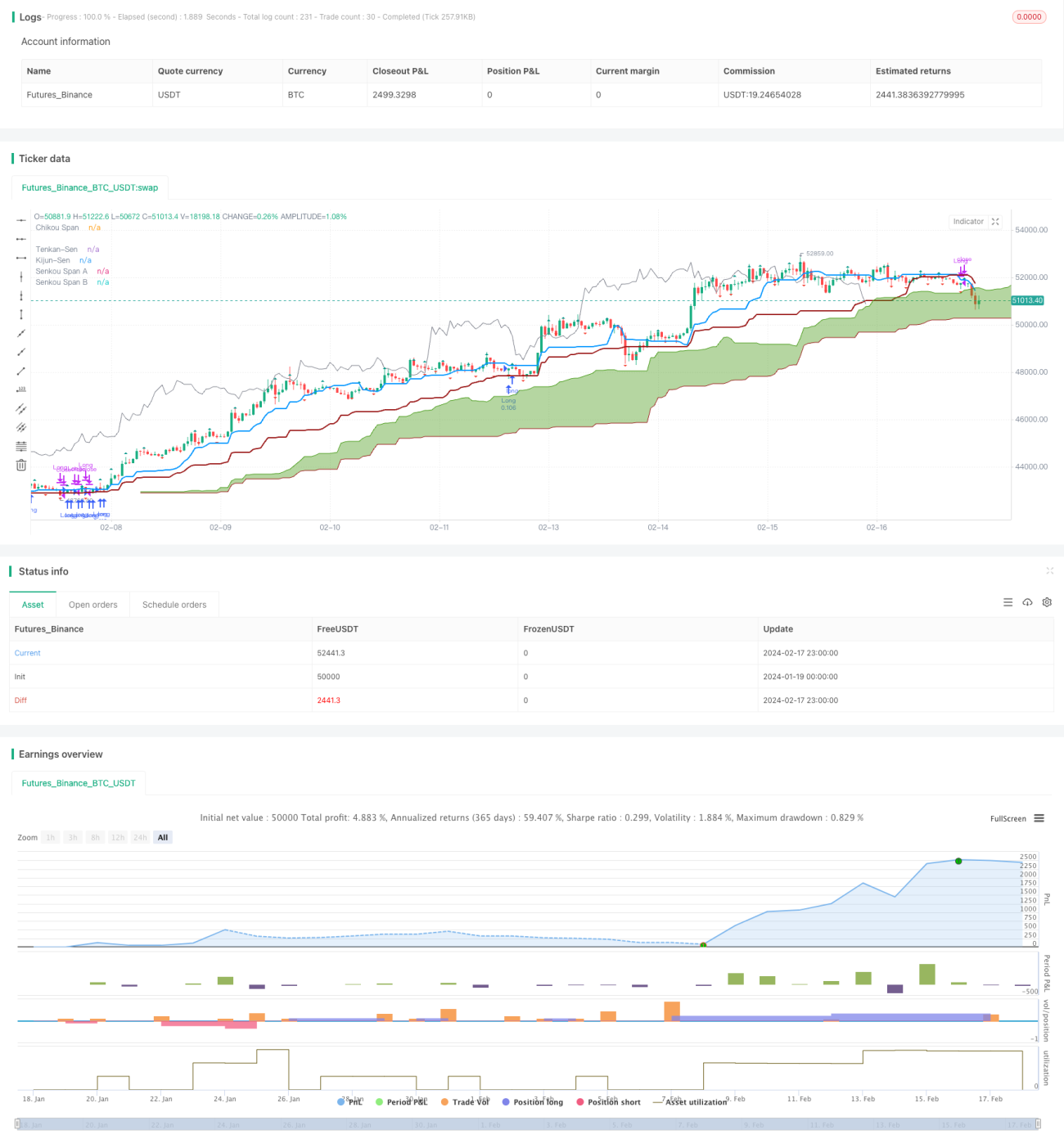

La stratégie Ichimoku Cloud Nine est une stratégie de trading basée sur l'indicateur Ichimoku Cloud combiné avec les fractales de Williams. Elle utilise les multiples signaux de trading fournis par l'indicateur Ichimoku Cloud pour générer des signaux de trading. Il s'agit d'une stratégie orientée vers le trading réel.

Principe de la stratégie

Cette stratégie repose principalement sur les signaux Ichimoku suivants pour entrer en position :

- Percée des nuages : un signal est généré lorsque le prix de clôture franchit le bord supérieur ou inférieur du nuage.

- Croisement TK : un signal est généré lorsque la ligne de conversion (Tenkan) croise la ligne de base (Kijun).

- Inversion des nuages : un signal est généré lorsque la ligne Senkou Span A croise la ligne Senkou Span B.

- Croisement de bord : un signal est généré lorsque le prix passe d'un côté du nuage à l'autre.

De plus, la stratégie ferme les positions dans les situations suivantes :

- Fermeture lorsque le prix de clôture entre dans le nuage.

- Fermeture lors d'un croisement inverse du TK.

- Fermeture partielle lorsque la fractale de Williams est cassée.

Cette stratégie fusionne plusieurs signaux de trading du graphique Ichimoku, visant à améliorer la fiabilité des signaux, tout en utilisant les fractales pour définir les stops et contrôler le risque.

Avantages de la stratégie

Par rapport aux stratégies à signal unique, cette stratégie utilise de manière combinée les multiples signaux du graphique Ichimoku, ce qui permet de filtrer certains signaux décalés et d'améliorer la précision des signaux. De plus, les paramètres de la stratégie peuvent être configurés de manière flexible, ce qui la rend adaptable à différents instruments et optimisations de paramètres.

En outre, l'introduction de la cassure des fractales de Williams pour définir les stops permet de contrôler le risque de manière plus proactive, de verrouiller les profits et d'éviter des pertes massives.

Risques de la stratégie

Cette stratégie est principalement confrontée aux risques suivants :

- L'indicateur de nuage présente un retard et ne peut pas refléter les variations de prix en temps réel.

- Les signaux multiples peuvent être trop prudents et faire manquer certaines opportunités.

- Le stop basé sur les fractales peut être cassé, entraînant des pertes.

Pour remédier au problème de retard, il est possible d'ajuster les paramètres ou de désactiver certains signaux de filtrage. Pour le risque de stop basé sur les fractales, il est possible d'ajuster la période des fractales ou de n'utiliser qu'un stop partiel.

Voies d'optimisation de la stratégie

Cette stratégie peut être principalement optimisée sous les aspects suivants :

- Ajuster les paramètres Ichimoku pour les adapter à différentes périodes et instruments.

- Ajuster ou désactiver certains signaux de filtrage, en conservant les signaux principaux.

- Ajuster les paramètres des fractales, en utilisant des fractales de périodes plus longues, ou en n'appliquant qu'un stop partiel.

- Ajouter d'autres indicateurs de filtrage, tels que des indicateurs de volume.

Résumé

La stratégie Ichimoku Cloud Nine intègre plusieurs signaux de trading du graphique Ichimoku, exploitant les avantages de l'indicateur de nuage tout en améliorant la précision et le taux de réussite des signaux. La stratégie utilise également les fractales comme méthode de stop pour contrôler le risque. Grâce à l'optimisation des paramètres et des signaux, elle peut être adaptée au trading algorithmique de plusieurs instruments.

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Cloud Nine", shorttitle="Ichimoku Cloud Nine", overlay=true, calc_on_every_tick = true, calc_on_order_fills = false, initial_capital = 5000, currency = "USD", default_qty_type = "percent_of_equity", default_qty_value = 10, pyramiding = 3, process_orders_on_close = true)

color green = #459915- 1