Stratégie de trading de retournement par rupture de canal

Aperçu

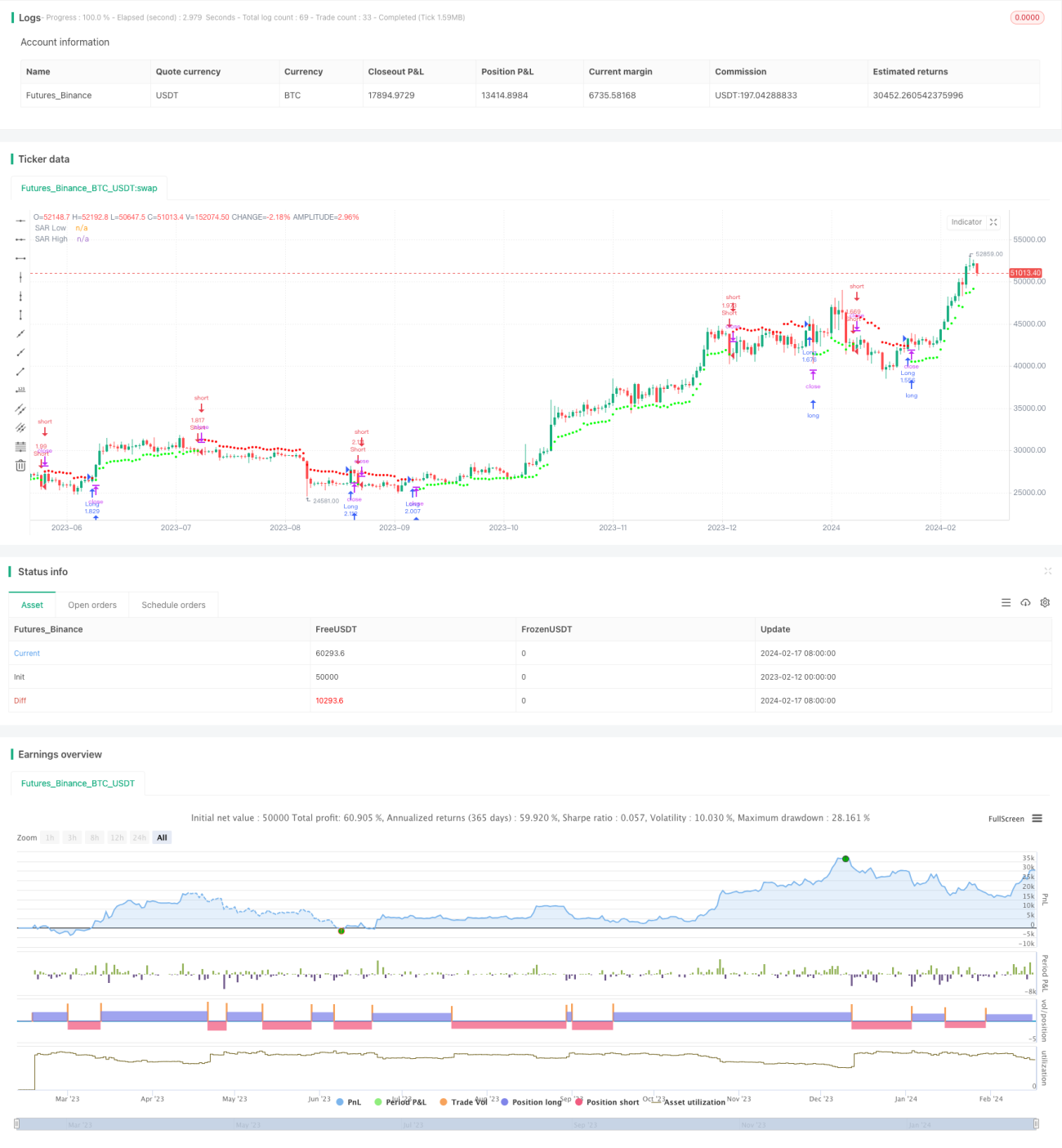

La stratégie de trading par retournement sur rupture de canal est une stratégie de trading par retournement qui suit un canal de prix pour déplacer les points de take-profit et de stop-loss. Elle utilise la méthode de la moyenne mobile pondérée pour calculer le canal de prix et ouvre des positions longues ou courtes lorsque le prix franchit le canal.

Principe de la stratégie

Cette stratégie calcule d'abord la volatilité des prix à l'aide de l'indicateur Average True Range (ATR) de Wilder. Ensuite, elle calcule la constante de range moyenne (ARC) à partir de la valeur ATR. L'ARC correspond à la moitié de la largeur du canal de prix. Ensuite, les bornes supérieure et inférieure du canal sont calculées, c'est-à-dire les points de take-profit et de stop-loss, appelés points SAR. Lorsque le prix franchit la borne supérieure, on vend à découvert ; lorsqu'il franchit la borne inférieure, on achète.

Plus précisément, on calcule d'abord l'ATR sur les N dernières bougies. Puis on multiplie l'ATR par un coefficient pour obtenir l'ARC. L'ARC multipliée par le coefficient permet de contrôler la largeur du canal. L'ARC est ajoutée au plus haut des prix de clôture des N bougies pour obtenir la borne supérieure du canal, c'est-à-dire le SAR haut. L'ARC est soustraite du plus bas des prix de clôture pour obtenir la borne inférieure du canal, c'est-à-dire le SAR bas. Si le prix de clôture franchit la borne supérieure, on vend à découvert ; s'il franchit la borne inférieure, on achète.

Avantages de la stratégie

- Utilisation de la volatilité des prix pour calculer un canal adaptatif, capable de suivre les évolutions du marché

- Trading par retournement, adapté aux marchés en retournement de tendance

- Take-profit et stop-loss mobiles, permettant de verrouiller les bénéfices et de contrôler les risques

Risques de la stratégie

- Le trading par retournement expose au risque de se faire piéger, nécessitant un réglage approprié des paramètres

- En cas de forte volatilité, les positions risquent d'être fermées prématurément

- Des paramètres inadaptés peuvent entraîner des transactions trop fréquentes

Solutions :

- Optimiser la période ATR et le coefficient ARC pour que la largeur du canal soit raisonnable

- Combiner avec des indicateurs de tendance pour filtrer les points d'entrée

- Augmenter la période ATR pour réduire la fréquence des transactions

Directions d'optimisation de la stratégie

- Optimiser la période ATR et le coefficient ARC

- Ajouter des conditions d'ouverture, par exemple en combinant avec l'indicateur MACD

- Ajouter une stratégie de stop-loss

Résumé

La stratégie de trading par retournement sur rupture de canal utilise un canal pour suivre les variations de prix, ouvre des positions en retournement lorsque la volatilité s'accentue, et met en place des take-profit et stop-loss mobiles adaptatifs. Cette stratégie convient aux marchés de range dominés par les retournements. À condition de bien identifier les points de retournement, elle peut offrir des rendements d'investissement intéressants. Cependant, il faut veiller à éviter des stop-loss trop larges et des problèmes d'optimisation des paramètres.

- 1