प्रवृत्ति उत्क्रमण अनुगामी स्टॉप लॉस रणनीति

अवलोकन

यह रणनीति प्रवृत्ति उलटने वाले संकेतक पर आधारित है, और प्रवृत्ति अनुवर्ती स्टॉप-लॉस तंत्र के साथ मिलकर, प्रवृत्ति बाजार में प्रवृत्ति का अनुसरण करने और संकुचित बाजार में नुकसान को कम करने का प्रभाव प्राप्त करती है।

रणनीति सिद्धांत

यह रणनीति हल मूविंग एवरेज (Hull Moving Average) को मुख्य प्रवृत्ति निर्धारण संकेतक के रूप में उपयोग करती है। जब कीमत हल एवरेज को ऊपर से पार करती है, तो लॉन्ग (खरीद) पोजीशन ली जाती है; जब कीमत हल एवरेज को नीचे से पार करती है, तो शॉर्ट (बेच) पोजीशन ली जाती है। साथ ही, मैकगिन्ली एवरेज (McGinley Average) का उपयोग प्रवृत्ति की पुष्टि के लिए किया जाता है।

पोजीशन खोलने के बाद, यदि कीमत उलट जाती है, अर्थात जब हल एवरेज पर क्रॉसओवर होता है, तो प्रवृत्ति परिवर्तन तर्क लागू होता है और वर्तमान पोजीशन बंद कर दी जाती है।

यह रणनीति प्रवृत्ति अनुवर्ती स्टॉप-लॉस तंत्र भी शामिल करती है। पोजीशन खोलने के बाद, ATR के आधार पर गतिशील स्टॉप-लॉस स्तर की गणना की जाती है। कीमत की चाल के साथ, स्टॉप-लॉस रेखा भी गतिशील रूप से समायोजित होती है, जिससे लाभ का अनुवर्ती स्टॉप-लॉस प्राप्त होता है।

रणनीति के लाभ

- हल एवरेज का उपयोग प्रवृत्ति उलट बिंदुओं को निर्धारित करने के लिए किया जाता है, हल एवरेज ब्रेकआउट संकेतों के प्रति उच्च संवेदनशीलता रखता है।

- मैकगिन्ली एवरेज के साथ प्रवृत्ति पुष्टि करने से कुछ झूठे ब्रेकआउट को फ़िल्टर किया जा सकता है।

- गतिशील अनुवर्ती स्टॉप-लॉस तंत्र का उपयोग करके बाजार की अस्थिरता के अनुसार स्टॉप-लॉस की सीमा को समायोजित किया जा सकता है, जिससे नुकसान को प्रभावी ढंग से नियंत्रित किया जा सकता है।

- हल एवरेज की पुष्टि करते समय प्रवृत्ति उलटने पर तुरंत प्रतिक्रिया देने से नुकसान को और बढ़ने से रोका जा सकता है।

- विभिन्न पैरामीटर संयोजनों को आसानी से बदलकर परीक्षण किया जा सकता है और इष्टतम पैरामीटर खोजे जा सकते हैं।

जोखिम और समाधान

- साइडवेज़ बाजार में स्टॉप-लॉस ट्रिगर होने की संभावना हो सकती है।

- उपयुक्त रूप से स्टॉप-लॉस की सीमा बढ़ाकर और स्टॉप-लॉस बफर जोड़कर इसे कम किया जा सकता है।

- तीव्र बाजार में, अनुवर्ती स्टॉप-लॉस कीमत में बदलाव का पीछा नहीं कर पा सकता है।

- स्मूथिंग अवधि को छोटा करके स्टॉप-लॉस को कीमत का तेजी से अनुसरण करने में मदद मिल सकती है।

- झूठे ब्रेकआउट अनावश्यक नुकसान का कारण बन सकते हैं।

- झूठे ब्रेकआउट से बचने के लिए अन्य संकेतक जोड़कर पुष्टि करें।

- अनुचित पैरामीटर रणनीति के खराब प्रदर्शन का कारण बन सकते हैं।

- विभिन्न बाजार चक्रों पर बैकटेस्ट करके इष्टतम पैरामीटर खोजे जा सकते हैं।

अनुकूलन विचार

- अन्य संकेतक जैसे कैंडलस्टिक पैटर्न, बोलिंगर बैंड, RSI आदि को शामिल करके पुष्टि करें और सिग्नल की गुणवत्ता में सुधार करें।

- विभिन्न उपकरणों और समय-सीमा मापदंडों के अनुसार अनुकूलन करें और सर्वोत्तम पैरामीटर संयोजन खोजें।

- मशीन लर्निंग जैसी विधियों का उपयोग करके पैरामीटर स्व-अनुकूलन अनुकूलन का प्रयास किया जा सकता है।

- स्टॉप-लॉस एल्गोरिदम को अनुकूलित करें ताकि स्टॉप-लॉस सुनिश्चित करते हुए अनावश्यक स्टॉप-लॉस को कम किया जा सके।

- धन प्रबंधन के साथ पोजीशन प्रबंधन रणनीति को अनुकूलित करें।

- स्वचालित लाभ-लक्ष्य (टेक प्रॉफिट) तंत्र जोड़ने पर विचार करें।

निष्कर्ष

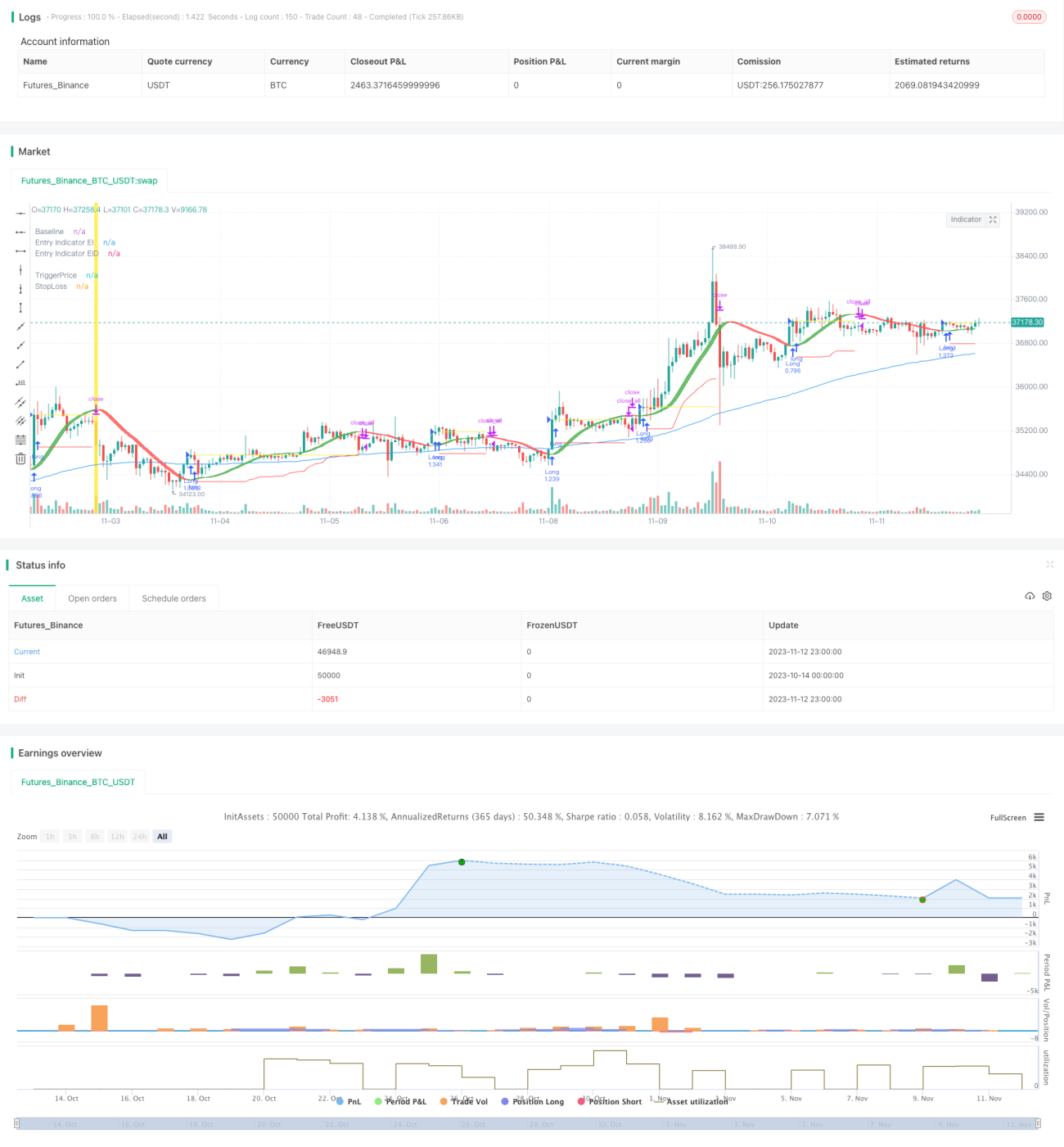

कुल मिलाकर यह रणनीति एक अपेक्षाकृत मजबूत प्रवृत्ति अनुवर्ती रणनीति है। निश्चित स्टॉप-लॉस की तुलना में, यह रणनीति गतिशील स्टॉप-लॉस तंत्र का उपयोग करती है, जो बाजार की अस्थिरता के अनुसार स्टॉप-लॉस की सीमा को समायोजित कर सकती है, जिससे स्टॉप-लॉस में फंसने की संभावना प्रभावी रूप से कम हो जाती है। साथ ही, हल एवरेज और प्रवृत्ति परिवर्तन तर्क का परिचय प्रवृत्ति उलटने पर त्वरित प्रतिक्रिया देने में सक्षम बनाता है। हालांकि, इस रणनीति में कुछ जोखिम भी हैं, जैसे साइडवेज़ बाजार में स्टॉप-लॉस जोखिम, झूठे ब्रेकआउट जोखिम आदि। संकेतक मापदंडों, स्टॉप-लॉस एल्गोरिदम, पोजीशन प्रबंधन आदि के और अनुकूलन के माध्यम से, रणनीति विभिन्न बाजारों में अधिक स्थिर प्रदर्शन प्राप्त कर सकती है।

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1