बहु-समय-सीमा-आधारित मात्रात्मक स्विंग ट्रेडिंग रणनीति

1

Follow

1802

Followers

अवलोकन

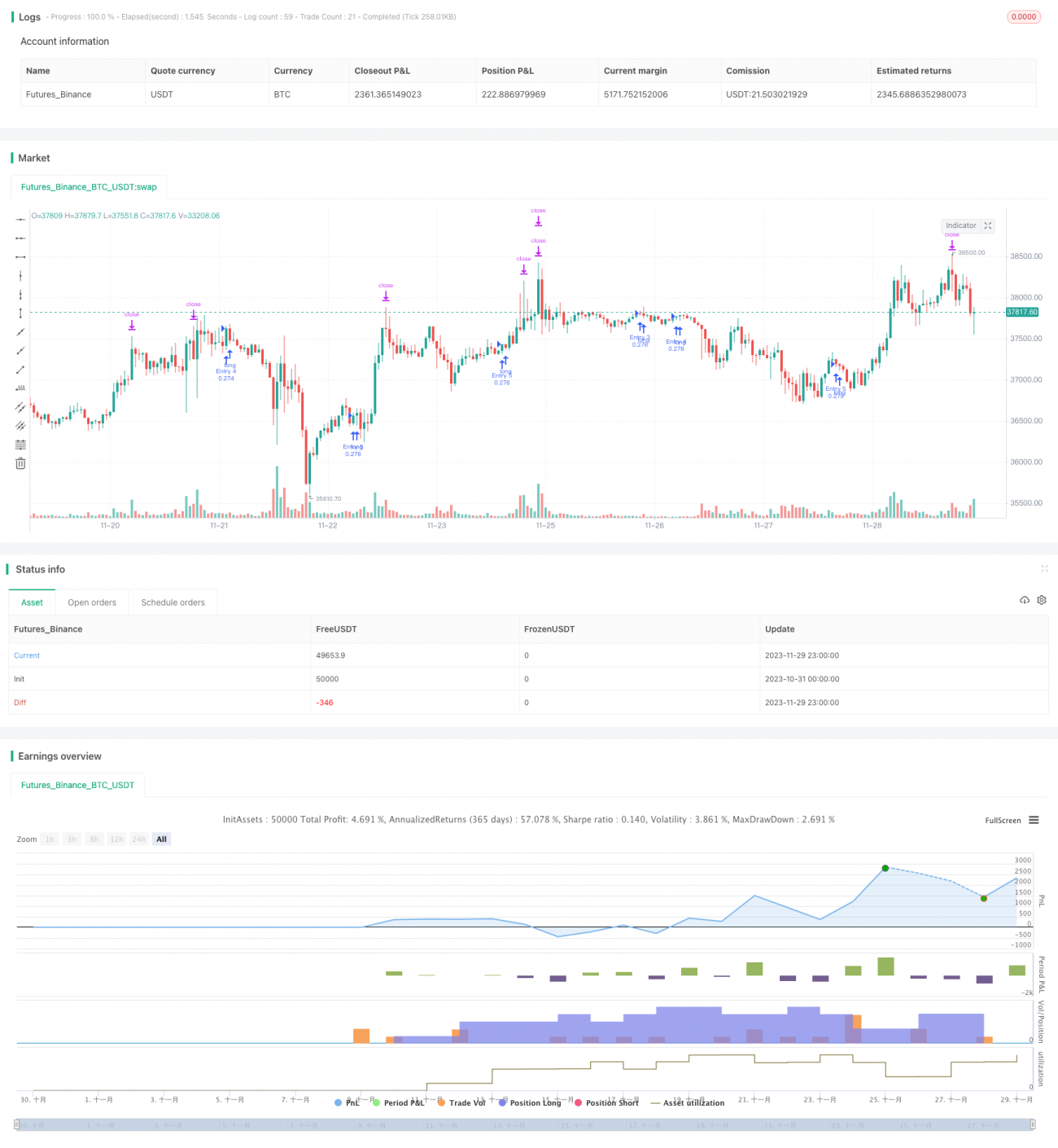

यह रणनीति विभिन्न समय-फ्रेम पर मात्रात्मक संकेतकों को संयोजित करके बिटकॉइन के मूल्य बैंड (तरंगों) की पहचान करती है, जिससे ट्रेंड-फॉलोइंग ट्रेडिंग की जा सके। रणनीति 5 मिनट के समय-फ्रेम का उपयोग करती है और लंबी अवधि के लिए बैंड रखकर लाभ कमाती है।

रणनीति सिद्धांत

- दैनिक समय-फ्रेम पर गणना किए गए RSI संकेतक में वॉल्यूम-भारित गणना का उपयोग करके झूठी ब्रेकआउट को फ़िल्टर किया जाता है।

- दैनिक RSI संकेतक को EMA स्मूथिंग के माध्यम से एक मात्रात्मक बैंड संकेतक में बदला जाता है।

- 5 मिनट के समय-फ्रेम में, रैखिक प्रतिगमन संकेतक और HMA संकेतक का उपयोग करके ट्रेडिंग सिग्नल बनाए जाते हैं।

- रणनीति मात्रात्मक बैंड संकेतक और ट्रेडिंग सिग्नल के संयोजन के माध्यम से विभिन्न समय-फ्रेमों को जोड़ती है, जिससे कीमतों के मध्यम से दीर्घकालिक बैंड की पहचान होती है।

लाभ विश्लेषण

- वॉल्यूम-भारित RSI संकेतक वास्तविक बैंड की प्रभावी पहचान करता है और झूठी ब्रेकआउट को फ़िल्टर करता है।

- HMA संकेतक मूल्य परिवर्तनों के प्रति अधिक संवेदनशील है और समय पर टर्निंग पॉइंट्स को पकड़ सकता है।

- कई समय-फ्रेमों का संयोजन मध्यम से दीर्घकालिक बैंड की अधिक सटीक पहचान करता है।

- 5 मिनट के समय-फ्रेम पर ट्रेडिंग से उच्च संचालन आवृत्ति मिलती है।

- बैंड-फॉलोइंग रणनीति को सटीक प्रवेश बिंदु चुनने की आवश्यकता नहीं होती है, और होल्डिंग अवधि लंबी होती है।

जोखिम विश्लेषण

- मात्रात्मक संकेतक गलत संकेत दे सकते हैं, इसलिए मौलिक विश्लेषण के साथ संयोजन की सलाह दी जाती है।

- बैंड बीच में उल्टा हो सकता है, इसलिए स्टॉप-लॉस निकास तंत्र सेट किया जाना चाहिए।

- ट्रेडिंग सिग्नल में देरी हो सकती है, जिससे सबसे अच्छा प्रवेश बिंदु छूट सकता है।

- लाभदायक बैंड के लिए लंबी होल्डिंग अवधि की आवश्यकता होती है, जिसमें कुछ पूंजी दबाव सहन करना पड़ता है।

अनुकूलन दिशाएँ

- विभिन्न मापदंडों के साथ RSI संकेतक के प्रभाव का परीक्षण करें।

- अन्य सहायक बैंड संकेतकों को शामिल करने का प्रयास करें।

- HMA संकेतक की लंबाई पैरामीटर को अनुकूलित करें।

- स्टॉप-लॉस और टेक-प्रॉफिट रणनीतियाँ जोड़ें।

- बैंड ट्रेडिंग की होल्डिंग अवधि को समायोजित करें।

निष्कर्ष

यह रणनीति मल्टी-टाइमफ्रेम कपलिंग और बैंड-फॉलोइंग दृष्टिकोण के माध्यम से बिटकॉइन के मध्यम से दीर्घकालिक प्रवृत्ति को प्रभावी ढंग से पकड़ती है। अल्पकालिक ट्रेडिंग की तुलना में, मध्यम से दीर्घकालिक बैंड ट्रेडिंग में कम ड्रॉडाउन और अधिक लाभ की गुंजाइश होती है। अगले चरण में, पैरामीटर समायोजन और जोखिम प्रबंधन रणनीतियों को जोड़कर रणनीति के रिटर्न और स्थिरता में और सुधार की उम्मीद की जा सकती है।

Source

Pine

/*backtest

start: 2023-10-31 00:00:00

end: 2023-11-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title='Pyramiding BTC 5 min', overlay=true, pyramiding=5, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=20, commission_type=strategy.commission.percent, commission_value=0.075)

//the pyramide based on this script https://www.tradingview.com/script/7NNJ0sXB-Pyramiding-Entries-On-Early-Trends-by-Coinrule/Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1