TFO और ATR पर आधारित ट्रेंड फॉलोइंग स्टॉप-लॉस रणनीति

अवलोकन

यह रणनीति डॉ. जॉन एहलर्स के ट्रेंड फ्लेक्स ऑसिलेटर (TFO) और एवरेज ट्रू रेंज (ATR) इंडिकेटर पर आधारित एक ट्रेंड फॉलोइंग स्टॉप-लॉस रणनीति है। यह केवल लॉन्ग पोजीशन के लिए उपयुक्त है और जब ओवरसोल्ड के बाद कीमत में उलटफेर होता है तो लॉन्ग पोजीशन खोलता है। आमतौर पर यह कुछ ही दिनों में पोजीशन बंद कर देता है, जब तक कि बाजार में भालू (बियरिश) का दबदबा न हो, ऐसी स्थिति में यह पोजीशन को बनाए रखता है। यह रणनीति सरल बैकटेस्टिंग के माध्यम से कॉन्फ़िगर करने योग्य पैरामीटर्स को समायोजित करती है, लेकिन बैकटेस्ट परिणामों पर पूरी तरह भरोसा नहीं किया जाना चाहिए।

रणनीति का सिद्धांत

यह रणनीति TFO और ATR दोनों इंडिकेटरों को जोड़ती है, और खरीद की शर्त पूरी होने पर लॉन्ग पोजीशन खोलती है तथा बिक्री की शर्त पूरी होने पर पोजीशन बंद करती है।

खरीद की शर्त: जब TFO एक निश्चित सीमा से नीचे हो (अत्यधिक ओवरसोल्ड दर्शाता है) और पिछली कैंडल का TFO मान वर्तमान कैंडल से कम हो (TFO में उलटफेर और ऊपर की ओर बढ़ने का संकेत), साथ ही ATR एक निर्धारित अस्थिरता सीमा से ऊपर हो (बाजार में अस्थिरता बढ़ने का संकेत), तो तीनों शर्तें पूरी होने पर लॉन्ग पोजीशन खोली जाती है।

बिक्री की शर्त: जब TFO एक निश्चित सीमा से ऊपर हो (अत्यधिक ओवरबॉट दर्शाता है) और ATR निर्धारित सीमा से ऊपर हो, तो शर्त पूरी होने पर सभी लॉन्ग पोजीशन बंद कर दी जाती हैं। इसके अतिरिक्त, रणनीति एक ट्रेलिंग स्टॉप-लॉस भी सेट करती है; यदि कीमत निर्धारित ट्रेलिंग स्टॉप-लॉस स्तर से नीचे गिरती है, तो सभी लॉन्ग पोजीशन बंद कर दी जाती हैं। उपयोगकर्ता यह चुन सकता है कि रणनीति इंडिकेटर सिग्नल के अनुसार पोजीशन बंद करे या केवल स्टॉप-लॉस स्तर के अनुसार।

यह रणनीति अधिकतम 15 लॉन्ग पोजीशन एक साथ खोल सकती है। इसके पैरामीटर्स को समायोजित किया जा सकता है, जो विभिन्न समय-सीमाओं के लिए उपयुक्त है।

रणनीति के लाभ

-

यह ट्रेंड और अस्थिरता दोनों को जोड़कर बाजार की दिशा का आकलन करती है, जो अधिक स्थिर है। TFO ट्रेंड ब्रेकआउट के शुरुआती संकेतों को पकड़ सकता है, और ATR बाजार में अस्थिरता बढ़ने के समय को पकड़ सकता है।

-

इसमें समायोज्य खरीद/बिक्री पैरामीटर और स्टॉप-लॉस पैरामीटर हैं, जो लचीला संचालन प्रदान करते हैं। उपयोगकर्ता बाजार के अनुसार पैरामीटर्स को अनुकूलित कर सकता है।

-

इसमें अंतर्निहित स्टॉप-लॉस सुविधा है, जो चरम बाजार स्थितियों में नुकसान को कम कर सकती है। स्टॉप-लॉस रणनीति मात्रात्मक ट्रेडिंग में एक बहुत महत्वपूर्ण तत्व है।

-

यह अतिरिक्त पोजीशन जोड़ने और आंशिक रूप से पोजीशन बंद करने का समर्थन करता है, जो पोजीशन बढ़ाकर लाभ को बढ़ा सकता है। यह तेजी वाले बाजार के लिए उपयुक्त है।

रणनीति के जोखिम

-

यह रणनीति केवल लॉन्ग पोजीशन लेती है, शॉर्ट नहीं, इसलिए यह गिरते बाजार में लाभ नहीं कमा सकती। यदि भयंकर मंदी का बाजार होता है, तो भारी नुकसान हो सकता है।

-

गलत पैरामीटर सेटिंग के कारण अत्यधिक ट्रेडिंग या खरीद-बिक्री छूट सकती है। सर्वोत्तम पैरामीटर संयोजन खोजने के लिए बार-बार परीक्षण की आवश्यकता होती है।

-

चरम बाजार स्थितियों में, स्टॉप-लॉस काम नहीं कर सकता और भारी नुकसान को रोकने में विफल हो सकता है। यह सभी स्टॉप-लॉस रणनीतियों का सामान्य जोखिम है।

-

बैकटेस्ट वास्तविक ट्रेडिंग को पूरी तरह से प्रतिबिंबित नहीं करता; वास्तविक परिणामों में कुछ अंतर हो सकता है।

रणनीति का अनुकूलन

-

बिक्री की शर्त में ट्रेलिंग स्टॉप-लॉस लाइन जोड़ने पर विचार किया जा सकता है, ताकि रणनीति समय पर स्टॉप-लॉस लगा सके और डाउनसाइड जोखिम को प्रभावी ढंग से नियंत्रित कर सके।

-

शॉर्टिंग तंत्र को शामिल किया जा सकता है: जब TFO उलटकर गिरता है और ATR पर्याप्त बड़ा होता है, तो शॉर्ट पोजीशन खोली जा सकती है, जिससे रणनीति मंदी के बाजार में भी काम कर सके।

-

अधिक फिल्टर शर्तें जोड़ी जा सकती हैं, जैसे वॉल्यूम में बदलाव, ताकि असामान्य बाजार स्थितियों के प्रभाव को कम किया जा सके।

-

विभिन्न समय-सीमाओं के लिए पैरामीटर सेटिंग और बैकटेस्ट परिणामों का परीक्षण किया जा सकता है, ताकि सर्वोत्तम समय-सीमा और पैरामीटर संयोजन खोजा जा सके।

निष्कर्ष

यह रणनीति ट्रेंड विश्लेषण और अस्थिरता निगरानी के लाभों को एकीकृत करती है, TFO और ATR इंडिकेटरों के संयोजन के माध्यम से बाजार की दिशा का निर्धारण करती है; इसमें अतिरिक्त पोजीशन जोड़ने, आंशिक रूप से पोजीशन बंद करने और ट्रेलिंग स्टॉप-लॉस जैसे तंत्र शामिल हैं, जो लाभ बढ़ा सकते हैं और जोखिम को नियंत्रित कर सकते हैं। यह तेजी वाले बाजार के लिए उपयुक्त है और इसमें विस्तार योग्य अनुकूलन की गुंजाइश है, जैसे अधिक इंडिकेटर फिल्टर और पैरामीटर ट्यूनिंग के माध्यम से प्रदर्शन में सुधार किया जा सकता है। यह मूल रूप से एक मात्रात्मक रणनीति की बुनियादी कार्यात्मक आवश्यकताओं को पूरा करती है और गहन अध्ययन एवं अनुप्रयोग के योग्य है।

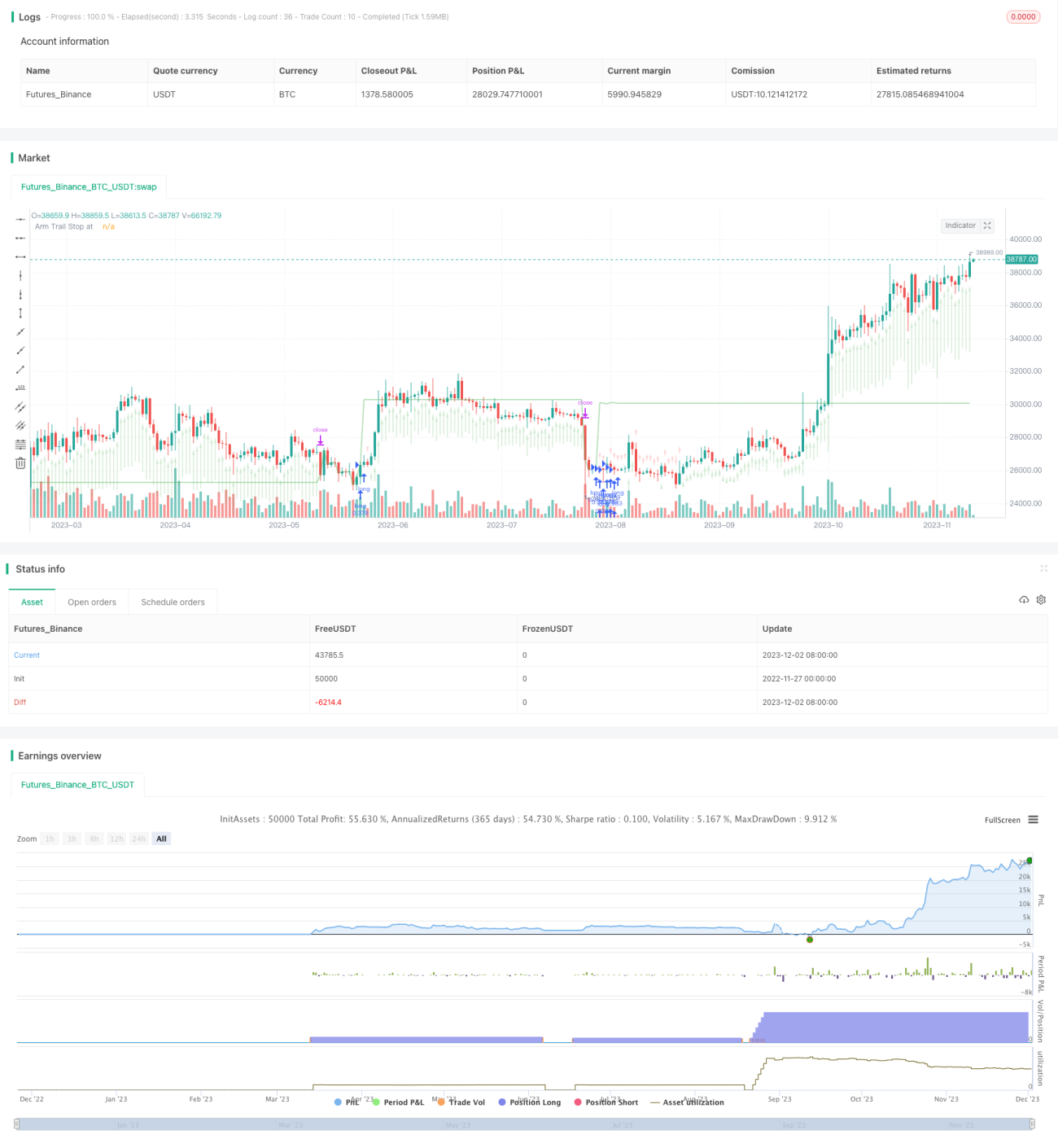

/*backtest

start: 2022-11-27 00:00:00

end: 2023-12-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

//

// Open Source attributions:- 1