अनुकूली बुवेनके संकेतक लांग-शॉर्ट रणनीति

सारांश (अवलोकन)

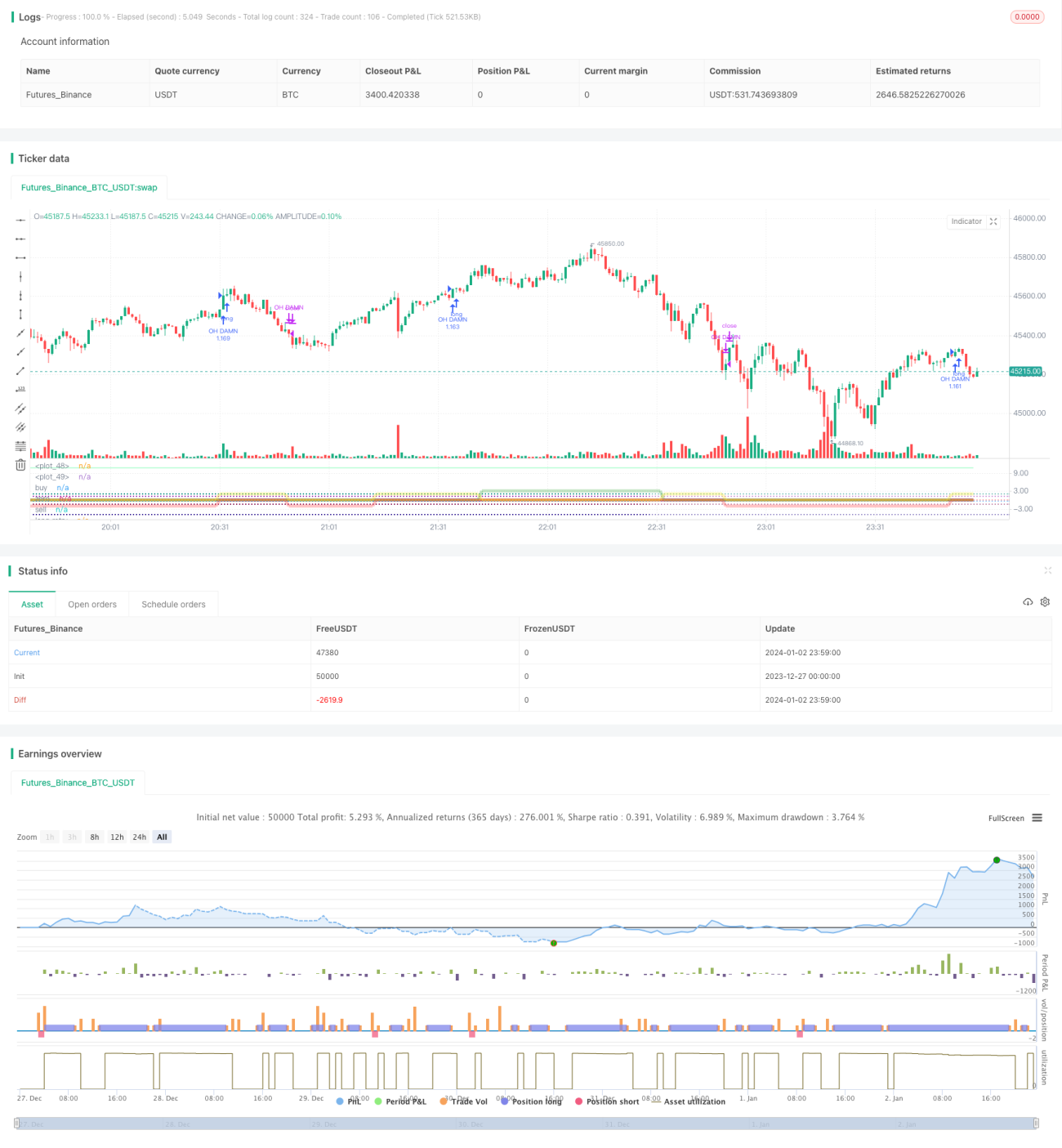

यह रणनीति बुवेन्के संकेतक के आधार पर बाजार की प्रवृत्ति की पहचान करने और लॉन्ग तथा शॉर्ट पोजीशन बनाने के लिए विकसित की गई है। इसमें बुवेन्के संकेतक, मूविंग एवरेज और क्षैतिज समर्थन रेखा जैसे तकनीकी संकेतक एकीकृत हैं, जो स्वचालित रूप से ब्रेकआउट सिग्नल की पहचान कर पोजीशन बनाते हैं।

रणनीति सिद्धांत

इस रणनीति का मुख्य संकेतक बुवेन्के संकेतक है, जो विभिन्न ट्रेडिंग दिनों के क्लोज़िंग प्राइस के लॉगरिदमिक अंतर की गणना करके बाजार की प्रवृत्ति और महत्वपूर्ण समर्थन/प्रतिरोध स्तरों का निर्धारण करता है। जब संकेतक किसी क्षैतिज रेखा को ऊपर से पार करता है तो लॉन्ग किया जाता है, और नीचे से पार करने पर शॉर्ट किया जाता है।

इसके अतिरिक्त, रणनीति में 21-दिन और 55-दिन जैसी कई मूविंग एवरेज से बनी "ईएमए सुरक्षा पट्टी" शामिल है। इन मूविंग एवरेज के क्रम के आधार पर यह निर्धारित किया जाता है कि बाजार वर्तमान में तेजड़िया, मंदड़िया या साइडवेज़ है, और तदनुसार शॉर्ट या लॉन्ग संचालन को प्रतिबंधित किया जाता है।

बुवेन्के संकेतक से ट्रेडिंग सिग्नल की पहचान और मूविंग एवरेज से बाजार चरण का निर्धारण – दोनों के संयोजन से अनुपयुक्त पोजीशन बनने से बचा जा सकता है।

लाभ विश्लेषण

इस रणनीति का सबसे बड़ा लाभ यह है कि यह बाजार की तेजी और मंदी की प्रवृत्ति को स्वचालित रूप से पहचान सकती है। बुवेन्के संकेतक दो समयावधियों के मूल्य अंतर के प्रति अत्यधिक संवेदनशील है, जो महत्वपूर्ण समर्थन और प्रतिरोध को तेज़ी से पहचानने में सक्षम है; साथ ही, मूविंग एवरेज का क्रम वर्तमान बाजार की स्थिति (तेजी या मंदी) का प्रभावी रूप से निर्धारण करता है।

तेज़ संकेतकों और प्रवृत्ति संकेतकों के इस संयोजन से रणनीति तेज़ी से खरीद-बिक्री के बिंदु पहचान सकती है और साथ ही अनुपयुक्त खरीद-बिक्री को रोक सकती है। यही इस रणनीति का सबसे बड़ा लाभ है।

जोखिम विश्लेषण

इस रणनीति के जोखिम मुख्यतः दो पहलुओं से आते हैं: पहला, बुवेन्के संकेतक स्वयं मूल्य परिवर्तन के प्रति अत्यधिक संवेदनशील है, जिससे कई अनावश्यक ट्रेडिंग सिग्नल उत्पन्न हो सकते हैं; दूसरा, साइडवेज़ बाजार में मूविंग एवरेज का क्रम अव्यवस्थित हो सकता है, जिससे पोजीशन निर्माण में भ्रम पैदा हो सकता है।

पहले जोखिम के लिए, बुवेन्के संकेतक के मापदंडों को उचित रूप से समायोजित किया जा सकता है, संकेतक गणना अवधि बढ़ाकर अनावश्यक ट्रेडिंग को कम किया जा सकता है; दूसरे जोखिम के लिए, अधिक मूविंग एवरेज जोड़कर प्रवृत्ति निर्धारण को अधिक सटीक बनाया जा सकता है।

अनुकूलन दिशाएँ

इस रणनीति की मुख्य अनुकूलन दिशाएँ मापदंड समायोजन और फ़िल्टर शर्तों को जोड़ना है।

बुवेन्के संकेतक के लिए, विभिन्न अवधि के मापदंडों को आज़माकर सर्वोत्तम पैरामीटर संयोजन पाया जा सकता है; मूविंग एवरेज के लिए, और अधिक एवरेज जोड़कर एक अधिक पूर्ण प्रवृत्ति निर्धारण प्रणाली बनाई जा सकती है। इसके अलावा, अस्थिरता संकेतक, वॉल्यूम संकेतक आदि फ़िल्टर शर्तें जोड़कर झूठे सिग्नल को कम किया जा सकता है।

मापदंडों और शर्तों के व्यापक समायोजन से रणनीति की स्थिरता और लाभप्रदता को और बढ़ाया जा सकता है।

सारांश

यह अनुकूली बुवेन्के लॉन्ग-शॉर्ट रणनीति तेज़ संकेतकों और प्रवृत्ति संकेतकों को सफलतापूर्वक संयोजित करती है, जो स्वचालित रूप से बाजार के प्रमुख बिंदुओं की पहचान कर सही पोजीशन बना सकती है। इसका लाभ तेज़ पहचान और अनुपयुक्त पोजीशन निर्माण को रोकने की क्षमता है। अगले चरण में मापदंडों और शर्तों के अनुकूलन के माध्यम से रणनीति की स्थिरता और लाभ स्तर को और बेहतर बनाया जा सकता है।

- 1