हाइब्रिड ट्रेडिंग रणनीति

अवलोकन

S&P500 मिश्रित मौसमी ट्रेडिंग रणनीति एक मात्रात्मक रणनीति है जो स्टॉक ट्रेडिंग में मौसमी पैटर्न का उपयोग करती है। यह रणनीति एक उन्नत खरीद-और-होल्ड सिस्टम, तकनीकी संकेतक शर्तों और मनी फ्लो इंडिकेटर को जोड़ती है, जिससे वर्ष के बेहतर और खराब ट्रेडिंग महीनों के बीच रोटेशन संभव होता है।

रणनीति सिद्धांत

रणनीति के ट्रेडिंग सिग्नल और नियम मुख्य रूप से इस प्रकार हैं:

- प्रत्येक वर्ष अक्टूबर के पहले ट्रेडिंग दिन के उद्घाटन पर लॉन्ग एंट्री करें।

- जब VIX 60% से ऊपर हो या 15-दिवसीय ATR 90% से ऊपर हो, तो मौसमी ट्रेडिंग को स्थगित करें और बाजार की अस्थिरता शांत होने तक प्रतीक्षा करें।

- प्रत्येक वर्ष अगस्त के पहले ट्रेडिंग दिन के उद्घाटन पर पोजीशन बंद करें।

- जब VIX 120% से अधिक हो या मनी फ्लो इंडिकेटर VFI -20 से नीचे गिर जाए और 10-दिवसीय मूविंग एवरेज नीचे की ओर हो, तब भी क्लोज सिग्नल जारी होता है।

- वैकल्पिक रूप से शॉर्ट ट्रेडिंग शामिल की जा सकती है।

यह रणनीति शेयर बाजार में एक वर्ष के भीतर असमान प्रदर्शन के पैटर्न का लाभ उठाती है, ऐतिहासिक रूप से बेहतर प्रदर्शन करने वाले अक्टूबर-अप्रैल महीनों में लॉन्ग जाती है और ऐतिहासिक रूप से खराब प्रदर्शन करने वाले मई-सितंबर महीनों में लाभ बुक करती है या शॉर्ट जाती है, इस प्रकार रिवर्स ट्रेडिंग करती है। साथ ही, रणनीति में कुछ तकनीकी संकेतक शर्तें जोड़ी गई हैं, जो बाजार में बड़े उतार-चढ़ाव के दौरान ट्रेडिंग को स्थगित कर जोखिम को कम करने में मदद करती हैं।

लाभ विश्लेषण

S&P500 मिश्रित मौसमी ट्रेडिंग रणनीति के निम्नलिखित लाभ हैं:

- परिपक्व और स्थिर मौसमी पैटर्न का उपयोग। यह रणनीति इस तथ्य पर आधारित है कि S&P500 इंडेक्स में वर्ष के दौरान स्पष्ट रूप से भिन्न प्रदर्शन वाले महीने होते हैं।

- कई फ़िल्टर शर्तों का संयोजन। रणनीति में VIX, ATR, VFI जैसी कई शर्तें शामिल हैं, जो Noise को प्रभावी ढंग से फ़िल्टर कर सकती हैं और अधिक विश्वसनीय ट्रेडिंग सिग्नल उत्पन्न कर सकती हैं।

- कॉन्फ़िगर करने योग्य ट्रेडिंग नियम। रणनीति में वैकल्पिक रूप से लॉन्ग या शॉर्ट जोड़ा जा सकता है, और ट्रेडिंग महीनों को आवश्यकतानुसार समायोजित किया जा सकता है, जिससे परीक्षण और अनुकूलन आसान हो जाता है।

- अंतर्निहित जोखिम निवारण तंत्र। जैसे VIX और ATR की अस्थिरता जांच, जो बाजार में अत्यधिक उतार-चढ़ाव के प्रभाव से प्रभावी रूप से बच सकती है।

- मनी फ्लो इंडिकेटर द्वारा सहायक निर्णय। VFI बाजार सहभागियों के फंड प्रवाह को प्रतिबिंबित कर सकता है, जो रणनीति के निर्णयों के लिए अतिरिक्त आधार प्रदान करता है।

जोखिम विश्लेषण

S&P500 मिश्रित मौसमी ट्रेडिंग रणनीति में कुछ संभावित जोखिम भी हैं:

- ऐतिहासिक पैटर्न के विफल होने का जोखिम। शेयर बाजार काफी अनिश्चितता के साथ चलता है, और ऐतिहासिक पैटर्न हमेशा प्रभावी नहीं रह सकते।

- तकनीकी संकेतकों द्वारा गलत सिग्नल देने का जोखिम। VIX, ATR और VFI जैसे संकेतक भी गलत संकेत दे सकते हैं।

- अपूर्ण पैरामीटर ऑप्टिमाइज़ेशन का जोखिम। रणनीति मापदंडों का और परीक्षण और अनुकूलन किया जा सकता है, मौजूदा पैरामीटर सर्वोत्तम नहीं हो सकते।

- शॉर्ट ट्रेडिंग से अतिरिक्त जोखिम। वैकल्पिक शॉर्ट ट्रेडिंग असीमित हानि का जोखिम लाती है।

जोखिम प्रबंधन, संकेतक संयोजन, पैरामीटर समायोजन, मशीन लर्निंग के उपयोग आदि के माध्यम से रणनीति को और मजबूत किया जा सकता है और उपरोक्त जोखिमों का समाधान किया जा सकता है।

अनुकूलन दिशाएँ

S&P500 मिश्रित मौसमी ट्रेडिंग रणनीति को निम्नलिखित पहलुओं से और बेहतर बनाया जा सकता है:

- लंबे ऐतिहासिक डेटा प्रशिक्षण का परीक्षण। रणनीति मापदंडों का पुनः परीक्षण और अनुकूलन करने के लिए अधिक ऐतिहासिक डेटा का उपयोग किया जा सकता है।

- स्टॉप-लॉस तंत्र जोड़ना। फ्लोटिंग स्टॉप-लॉस या टाइम स्टॉप-लॉस सेट किया जा सकता है, जिससे प्रति ट्रेड हानि को प्रभावी ढंग से नियंत्रित किया जा सके।

- तकनीकी संकेतक मापदंडों का अनुकूलन। VIX, ATR और VFI के मापदंडों को समायोजित कर इष्टतम पैरामीटर संयोजन खोजा जा सकता है।

- मशीन लर्निंग मॉडल शामिल करना। पैरामीटर स्व-अनुकूलन के लिए न्यूरल नेटवर्क या डिसीज़न ट्री का उपयोग किया जा सकता है।

- रणनीतियों का संयोजन। अन्य रणनीतियों के साथ संयोजन का परीक्षण किया जा सकता है, जिससे गैर-सहसंबंध का उपयोग करके बाजार के व्यवस्थित जोखिम को कम किया जा सके।

सारांश

S&P500 मिश्रित मौसमी ट्रेडिंग रणनीति परिपक्व मौसमी पैटर्न, तकनीकी संकेतक शर्तों और मनी फ्लो इंडिकेटर का व्यापक उपयोग करती है। यह रणनीति शेयर बाजार के सबसे खराब प्रदर्शन वाले महीनों से बचती है, वर्ष के बेहतर ट्रेडिंग महीनों में आवंटन करती है, और इसमें प्रभावी बाजार अस्थिरता फ़िल्टरिंग तंत्र शामिल है, जो स्थिर अतिरिक्त रिटर्न उत्पन्न कर सकता है। साथ ही, रणनीति का परीक्षण, अनुकूलन और समायोजन आसान है, और यह मात्रात्मक ट्रेडर्स के लिए एक संदर्भित और पुनर्विकास योग्य ढांचा प्रदान करती है। अधिक डेटा, स्टॉप-लॉस उपायों, पैरामीटर समायोजन और संयोजन जैसे तरीकों को शामिल करके, रणनीति के प्रभाव को और बढ़ाने की संभावना है।

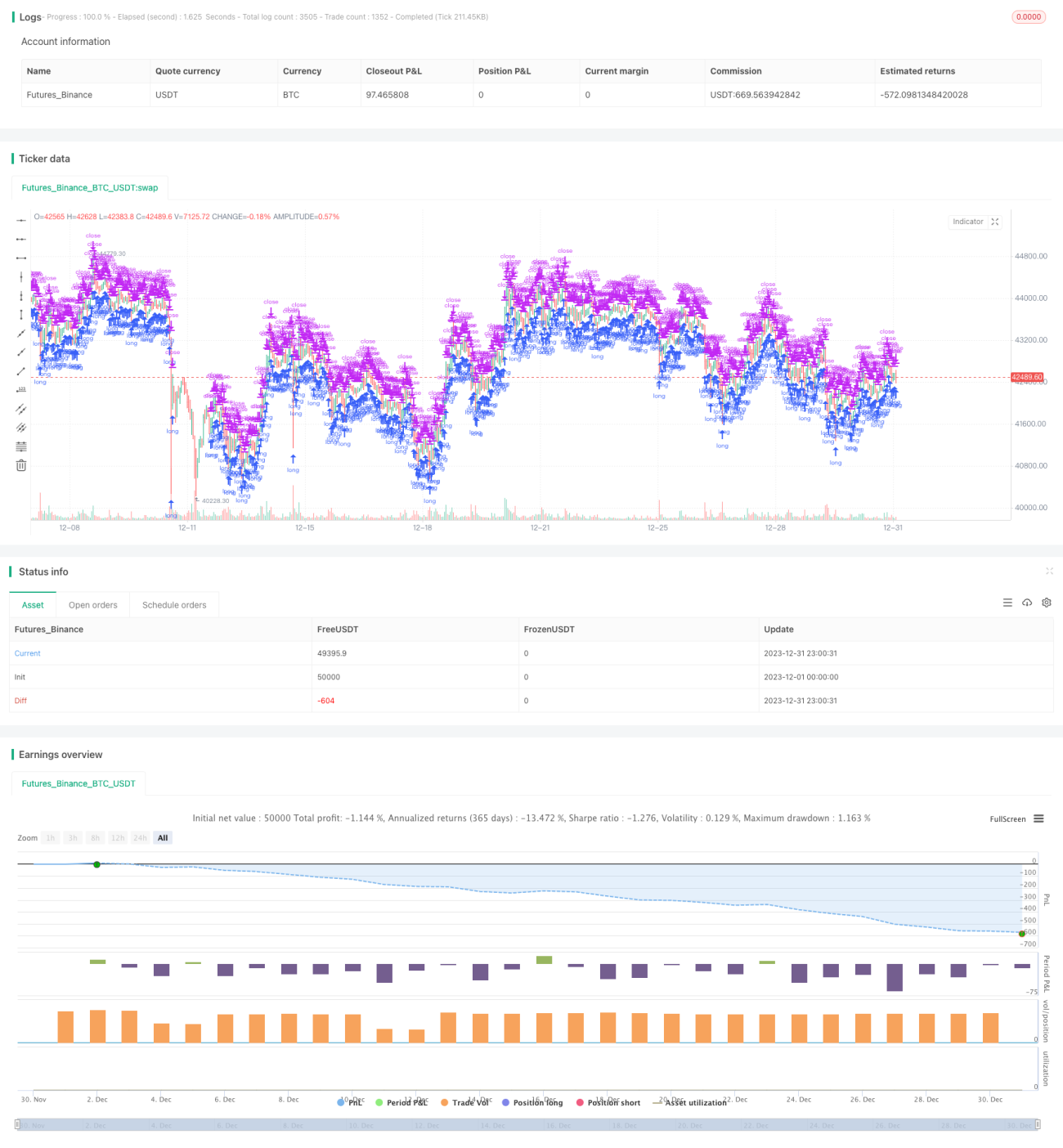

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// TASC Issue: April 2022 - Vol. 40, Issue 4

// Article: Sell In May? Stock Market Seasonality

// Article By: Markos Katsanos

// Language: TradingView's Pine Script v5- 1