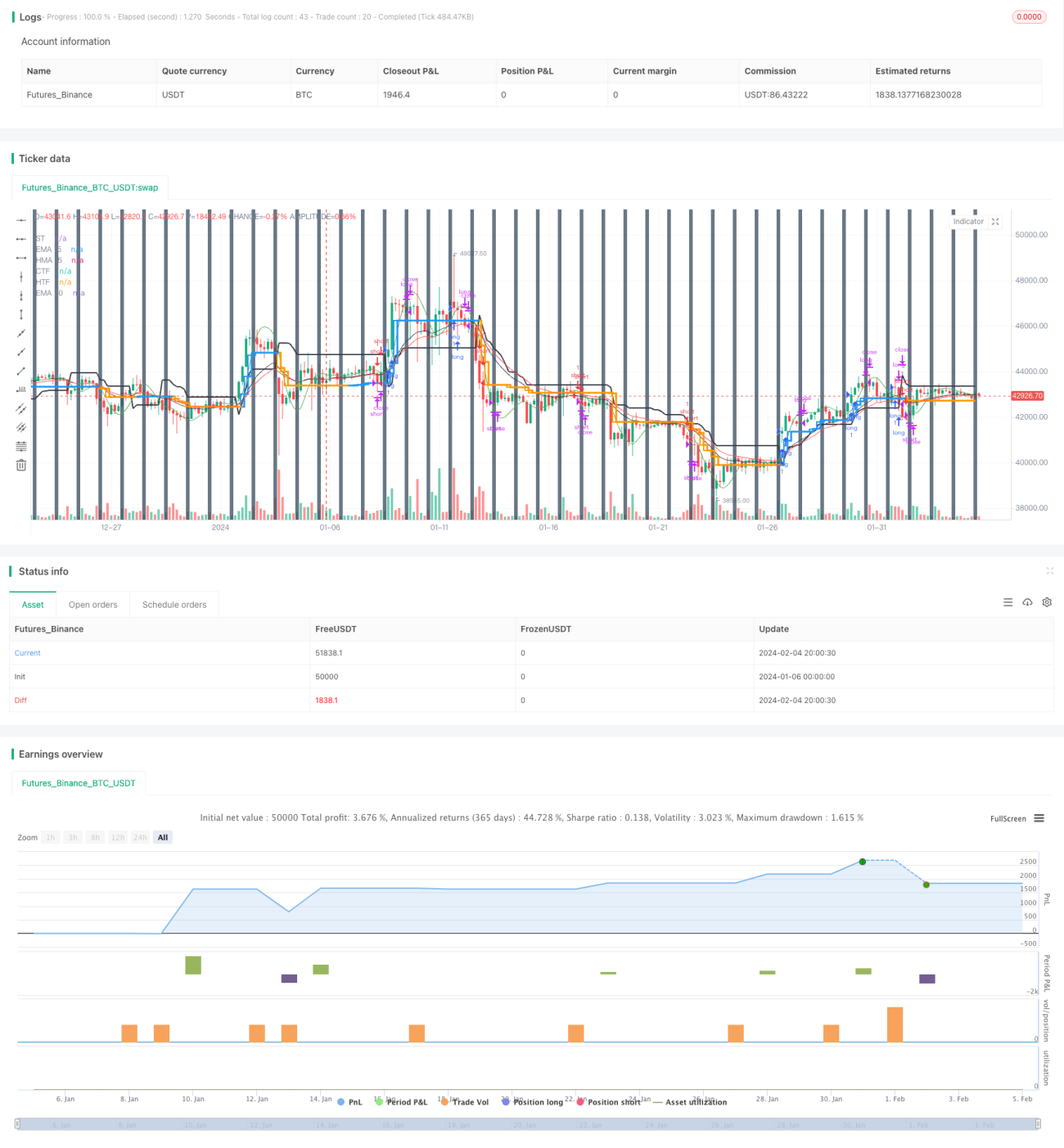

Heikin Ashi आधारित सुपर ट्रेंड ट्रेलिंग स्टॉप हानि रणनीति

रणनीति का सारांश

यह रणनीति हीकिन आशी कैंडलस्टिक्स और सुपरट्रेंड इंडिकेटर को मिलाकर एक ट्रेंड-फॉलोइंग स्टॉप-लॉस रणनीति है। यह हीकिन आशी कैंडलस्टिक्स का उपयोग बाजार के शोर को फ़िल्टर करने के लिए करती है, सुपरट्रेंड इंडिकेटर से ट्रेंड की दिशा का पता लगाती है, और सुपरट्रेंड को एक गतिशील स्टॉप-लॉस लाइन के रूप में उपयोग करके कुशल ट्रेंड ट्रैकिंग और जोखिम नियंत्रण प्राप्त करती है।

रणनीति का सिद्धांत

- हीकिन आशी कैंडलस्टिक्स की गणना करें: इसमें ओपन, क्लोज़, हाई और लो शामिल हैं।

- सुपरट्रेंड इंडिकेटर की गणना करें: ATR और कीमत के आधार पर ऊपरी और निचली बैंड की गणना करें।

- ट्रेंड की दिशा निर्धारित करने के लिए हीकिन आशी कैंडलस्टिक्स और सुपरट्रेंड को मिलाएं।

- जब हीकिन आशी का क्लोज़ पिछली कैंडल के क्लोज़ की तुलना में सुपरट्रेंड की ऊपरी बैंड के अधिक करीब होता है, तो यह तेजी का संकेत है; जब हीकिन आशी का क्लोज़ पिछली कैंडल के क्लोज़ की तुलना में सुपरट्रेंड की निचली बैंड के अधिक करीब होता है, तो यह मंदी का संकेत है।

- तेजी के ट्रेंड में, सुपरट्रेंड की ऊपरी बैंड को ट्रेलिंग स्टॉप-लॉस लाइन के रूप में उपयोग करें; मंदी के ट्रेंड में, सुपरट्रेंड की निचली बैंड को ट्रेलिंग स्टॉप-लॉस लाइन के रूप में उपयोग करें।

रणनीति के लाभ

- हीकिन आशी का उपयोग करके झूठे ब्रेकआउट को फ़िल्टर करता है, जिससे ट्रेंड सिग्नल अधिक विश्वसनीय बनते हैं।

- सुपरट्रेंड एक गतिशील स्टॉप-लॉस के रूप में कार्य करता है, जिससे ट्रेंड लाभ अधिकतम होता है और अत्यधिक ड्रॉडाउन से बचा जाता है।

- विभिन्न समय अवधियों में बुलिश और बेयरिश का निर्धारण करने से हाई और लो सिग्नल अधिक विश्वसनीय बनते हैं।

- समय पर पोज़ीशन बंद करने की सुविधा विशिष्ट समय पर होने वाली तर्कहीन मार्केट चालों के प्रभाव को कम करती है।

रणनीति के जोखिम

- ट्रेंड रिवर्सल होने पर स्टॉप-लॉस लगने की संभावना। स्टॉप-लॉस लाइन को थोड़ा ढीला करके इस जोखिम को कम किया जा सकता है।

- सुपरट्रेंड पैरामीटर के अनुचित सेटिंग से स्टॉप-लॉस बहुत चौड़ा या संकीर्ण हो सकता है। विभिन्न पैरामीटर संयोजनों का परीक्षण किया जा सकता है।

- मनी मैनेजमेंट पर विचार नहीं किया गया। पोज़ीशन नियंत्रण सेट किया जाना चाहिए।

- ट्रेडिंग लागत पर विचार नहीं किया गया। लागत के प्रभाव का आकलन किया जाना चाहिए।

रणनीति अनुकूलन दिशाएँ

- सुपरट्रेंड पैरामीटर संयोजनों का अनुकूलन करें, इष्टतम पैरामीटर खोजें।

- पोज़ीशन नियंत्रण कार्यक्षमता जोड़ें।

- लागत विचार जोड़ें, जैसे कमीशन, स्लिपेज आदि।

- ट्रेंड की ताकत के आधार पर स्टॉप-लॉस की चौड़ाई को लचीले ढंग से समायोजित करें।

- एंट्री सिग्नल को फ़िल्टर करने के लिए अन्य इंडिकेटरों को शामिल करने पर विचार करें।

निष्कर्ष

यह रणनीति हीकिन आशी और सुपरट्रेंड दोनों इंडिकेटरों के लाभों को एकीकृत करती है, जिससे ट्रेंड की दिशा को पकड़ा जा सकता है, साथ ही सुपरट्रेंड के माध्यम से स्वचालित गतिशील ट्रेलिंग स्टॉप-लॉस प्राप्त होता है, जिससे ट्रेंड मुनाफा लॉक किया जा सकता है। रणनीति के मुख्य जोखिम ट्रेंड रिवर्सल और पैरामीटर अनुकूलन से हैं, जिन्हें आगे के अनुकूलन के माध्यम से सुधारा जा सकता है। कुल मिलाकर, यह रणनीति इंडिकेटर एकीकरण के माध्यम से ट्रेडिंग सिस्टम की स्थिरता और लाभ क्षमता को बढ़ाती है।

- 1