Strategi trailing stop loss pembalikan tren

Ringkasan

Strategi ini didasarkan pada indikator pembalikan tren, dikombinasikan dengan mekanisme stop-loss penjejakan tren, yang memungkinkan untuk mengikuti tren di pasar yang sedang tren dan mengurangi kerugian di pasar yang bergerak sideways.

Prinsip Strategi

Strategi ini menggunakan Hull Moving Average sebagai indikator utama penentuan tren. Ketika harga menembus ke atas Hull MA, posisi long dibuka; ketika harga menembus ke bawah Hull MA, posisi short dibuka. Pada saat yang sama, McGinley Moving Average digunakan untuk mengonfirmasi tren.

Setelah posisi dibuka, jika terjadi pembalikan harga, yaitu ketika Hull MA mengalami persilangan (crossover), logika perubahan tren akan dijalankan dan posisi saat ini ditutup.

Strategi ini juga menerapkan mekanisme stop-loss penjejakan tren. Setelah posisi dibuka, level stop-loss dinamis dihitung berdasarkan ATR. Seiring pergerakan harga, garis stop-loss juga akan menyesuaikan secara dinamis, memungkinkan trailing stop untuk mengunci keuntungan.

Keunggulan Strategi

- Menggunakan Hull MA untuk menentukan titik pembalikan tren; Hull MA sangat sensitif terhadap sinyal breakout.

- Dikombinasikan dengan McGinley MA untuk konfirmasi tren, dapat menyaring sebagian sinyal breakout palsu.

- Menerapkan mekanisme trailing stop dinamis yang dapat menyesuaikan lebar stop-loss berdasarkan volatilitas pasar, secara efektif mengendalikan kerugian.

- Saat verifikasi Hull MA, strategi merespons pembalikan tren dengan cepat untuk mencegah kerugian semakin membesar.

- Mudah beralih ke berbagai kombinasi parameter untuk pengujian guna menemukan parameter optimal.

Risiko dan Solusi

- Dalam kondisi pasar yang bergerak sideways (oscillating), stop-loss mungkin tersentuh.

- Solusi: Perlebar lebar stop-loss yang sesuai, tambahkan buffer stop-loss.

- Dalam kondisi pasar yang sangat fluktuatif, trailing stop mungkin tidak dapat mengikuti pergerakan harga.

- Solusi: Persingkat periode smoothing agar stop-loss lebih cepat mengikuti harga.

- Breakout palsu dapat menyebabkan kerugian yang tidak perlu.

- Solusi: Tambahkan indikator lain untuk konfirmasi guna menghindari breakout palsu.

- Parameter yang tidak tepat dapat menyebabkan kinerja strategi buruk.

- Solusi: Lakukan backtest pada siklus pasar yang berbeda untuk menemukan parameter optimal.

Ide Optimasi

- Tambahkan indikator lain untuk konfirmasi, seperti pola candlestick, Bollinger Bands, RSI, dll., untuk meningkatkan kualitas sinyal.

- Optimalkan parameter berdasarkan instrumen dan periode waktu yang berbeda untuk menemukan kombinasi parameter terbaik.

- Coba gunakan metode pembelajaran mesin untuk optimasi parameter adaptif.

- Optimalkan algoritma stop-loss untuk meminimalkan stop-loss yang tidak perlu sambil tetap melindungi posisi.

- Gabungkan manajemen modal untuk mengoptimalkan strategi ukuran posisi.

- Pertimbangkan untuk menambahkan mekanisme take-profit otomatis.

Kesimpulan

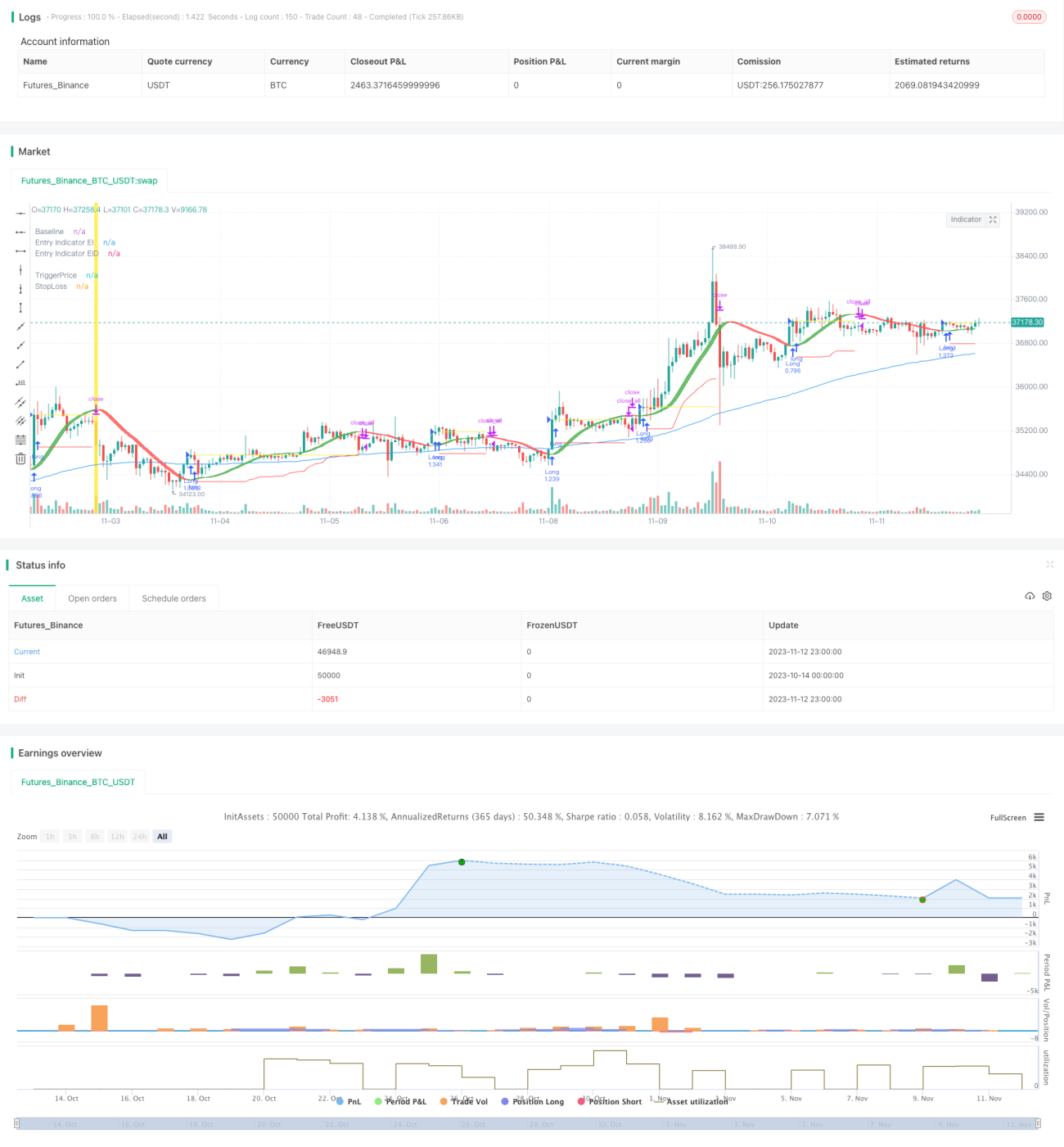

Secara keseluruhan, strategi ini merupakan strategi penjejakan tren yang cukup stabil. Dibandingkan dengan stop-loss tetap, strategi ini menggunakan mekanisme stop-loss dinamis yang dapat menyesuaikan lebar stop-loss berdasarkan volatilitas pasar, secara efektif mengurangi probabilitas stop-loss tersentuh. Pada saat yang sama, pengenalan Hull MA dan logika perubahan tren memungkinkan respons yang cepat terhadap pembalikan tren. Namun, strategi ini juga memiliki risiko tertentu, seperti risiko stop-loss di pasar sideways dan risiko breakout palsu. Dengan mengoptimalkan parameter indikator, algoritma stop-loss, manajemen posisi, dan lainnya, strategi dapat mencapai kinerja yang lebih stabil di berbagai pasar.

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1