Strategi Filter Breakout Tren dengan Dua Moving Average

Ikhtisar

Ini adalah strategi yang menggunakan moving average dan Bollinger Bands untuk menentukan tren, serta menggabungkan prinsip filter breakout dan stop loss. Strategi ini dapat menangkap sinyal tepat waktu saat tren berubah, mengurangi sinyal palsu melalui double moving average filter, dan menetapkan stop loss untuk mengelola risiko.

Prinsip Strategi

Strategi ini terutama terdiri dari beberapa bagian berikut:

-

Penentuan Tren: Menggunakan MACD untuk menentukan tren harga, membedakan tren bullish dan bearish.

-

Filter Rentang: Menggunakan Bollinger Bands untuk menentukan kisaran fluktuasi harga, menyaring sinyal yang tidak menembus rentang.

-

Konfirmasi Double Moving Average: EMA cepat dan EMA lambat membentuk double moving average, digunakan untuk mengonfirmasi sinyal tren. Sinyal beli hanya muncul ketika EMA cepat > EMA lambat.

-

Mekanisme Stop Loss: Menetapkan titik stop loss, menutup posisi ketika harga menembus titik stop loss ke arah yang tidak menguntungkan.

Logika penentuan sinyal masuk adalah:

- MACD mengindikasikan tren naik

- Harga menembus pita atas Bollinger Bands

- EMA cepat lebih tinggi dari EMA lambat

Ketika ketiga kondisi di atas terpenuhi secara bersamaan, sinyal beli dihasilkan.

Logika penutupan posisi dibagi menjadi dua jenis, yaitu take profit dan stop loss. Titik take profit adalah harga masuk dikalikan dengan persentase tertentu, dan titik stop loss adalah harga masuk dikalikan dengan persentase tertentu. Posisi ditutup ketika harga menembus salah satu titik tersebut.

Analisis Keunggulan

Strategi ini memiliki keunggulan sebagai berikut:

- Mampu menangkap perubahan tren dengan cepat, sedikit lag.

- Menyaring sinyal palsu melalui double moving average, meningkatkan kualitas sinyal.

- Mekanisme stop loss secara efektif mengendalikan kerugian per transaksi.

- Ruang optimasi parameter yang luas, dapat disesuaikan ke kondisi terbaik.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko:

- Sinyal palsu yang dihasilkan di pasar sideways dapat menyebabkan kerugian.

- Pengaturan titik stop loss yang tidak tepat dapat menyebabkan kerugian yang tidak perlu.

- Parameter yang tidak sesuai dapat menyebabkan kinerja strategi yang buruk.

Untuk mengatasi risiko ini, dapat dilakukan optimalisasi dan perbaikan melalui penyesuaian parameter, penyesuaian posisi stop loss, dan sebagainya.

Arah Optimasi

Strategi ini dapat dioptimalkan dari beberapa arah berikut:

- Menyesuaikan panjang double moving average untuk menemukan kombinasi parameter terbaik.

- Menguji berbagai metode stop loss, seperti trailing stop loss, volatilitas stop loss, dll.

- Menguji parameter MACD untuk menemukan parameter optimal.

- Menggunakan machine learning untuk optimasi parameter secara otomatis.

- Menambahkan kondisi tambahan untuk menyaring sinyal.

Dengan menguji berbagai pengaturan parameter dan mengevaluasi tingkat pengembalian serta Sharpe ratio, dapat ditemukan kondisi terbaik dari strategi ini.

Kesimpulan

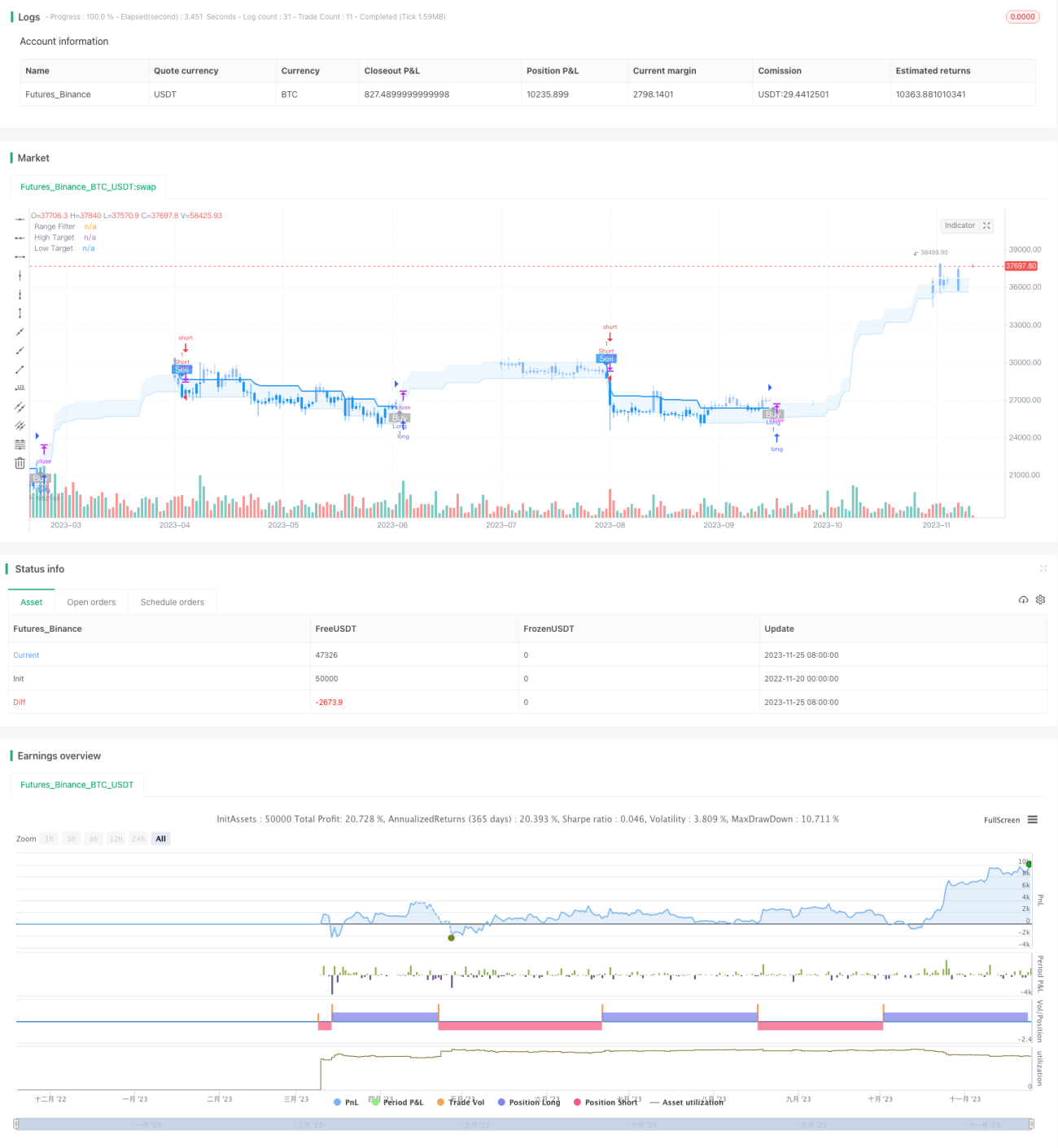

Ini adalah strategi kuantitatif yang menggunakan penentuan tren, filter rentang, konfirmasi double moving average, dan konsep stop loss. Strategi ini secara efektif dapat menentukan arah tren, menemukan keseimbangan antara maksimalisasi laba dan pengendalian risiko. Melalui optimasi parameter dan machine learning, strategi ini masih memiliki ruang perbaikan yang besar untuk mencapai hasil yang lebih baik.

/*backtest

start: 2022-11-20 00:00:00

end: 2023-11-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Range Filter Buy and Sell Strategies", shorttitle="Range Filter Strategies", overlay=true,pyramiding = 5)

// Original Script > @DonovanWall- 1