Strategi Pembalikan RSI Multi-Faktor

Ikhtisar

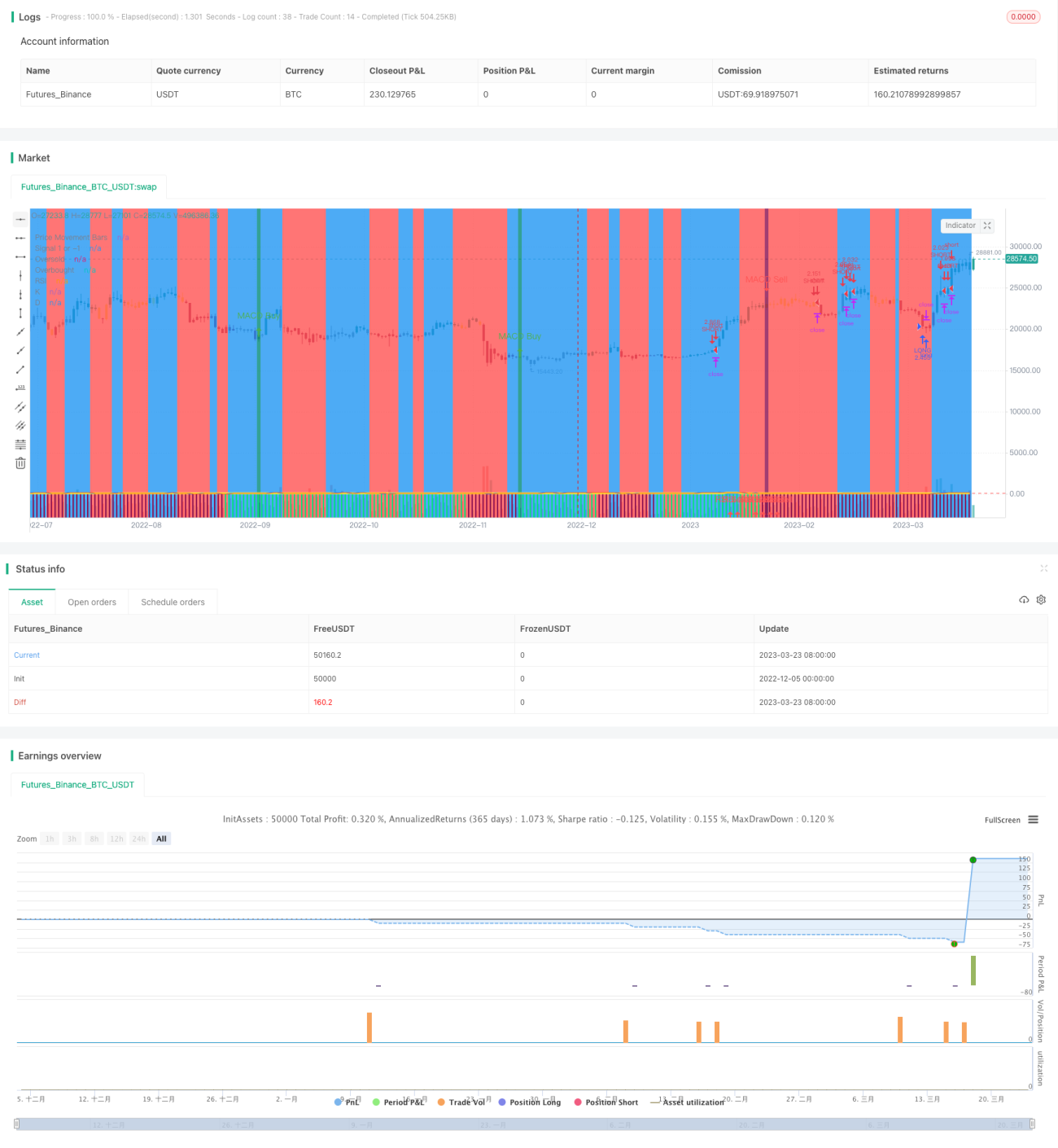

Strategi ini menggunakan indikator RSI untuk mengidentifikasi kondisi jenuh beli dan jenuh jual, dikombinasikan dengan berbagai faktor bantu seperti MACD, Stochastic, dan lain-lain untuk entry. Strategi ini bertujuan menangkap peluang pembalikan jangka pendek dan termasuk dalam strategi pembalikan (reversal strategy).

Prinsip Strategi

Strategi ini terutama memanfaatkan indikator RSI untuk menilai apakah pasar berada dalam kondisi jenuh beli atau jenuh jual. Ketika indikator RSI melebihi garis jenuh beli yang ditetapkan, hal ini menunjukkan pasar mungkin berada dalam kondisi jenuh beli, sehingga strategi memilih untuk melakukan short. Ketika indikator RSI turun di bawah garis jenuh jual yang ditetapkan, hal ini menunjukkan pasar mungkin berada dalam kondisi jenuh jual, sehingga strategi memilih untuk melakukan long. Dengan cara ini, strategi memperoleh keuntungan dari peluang perdagangan jangka pendek yang muncul selama proses pembalikan saat pasar beralih dari satu kondisi ekstrem ke kondisi ekstrem lainnya.

Selain itu, strategi juga memperkenalkan beberapa faktor bantu seperti MACD dan Stochastic. Fungsi faktor bantu ini adalah untuk menyaring sinyal perdagangan positif palsu yang mungkin muncul. Hanya ketika indikator RSI memberikan sinyal dan faktor bantu juga mendukung sinyal tersebut, strategi akan mengambil tindakan perdagangan yang sebenarnya. Pendekatan multi-faktor ini dapat meningkatkan keandalan sinyal strategi, sehingga juga meningkatkan stabilitas strategi.

Analisis Kelebihan

Kelebihan terbesar dari strategi ini adalah efisiensi penangkapan yang tinggi, serta penerapan verifikasi multi-faktor yang meningkatkan kualitas sinyal. Secara khusus, hal ini tercermin dalam beberapa aspek berikut:

- Indikator RSI sendiri memiliki kemampuan yang kuat dalam mengidentifikasi rezim pasar, sehingga dapat secara efektif mengenali kondisi jenuh beli dan jenuh jual.

- Dengan bantuan berbagai alat bantu untuk verifikasi multi-faktor, kualitas sinyal meningkat dan sejumlah besar sinyal positif palsu tersaring.

- Strategi ini tidak sensitif terhadap parameter, sehingga mudah dioptimalkan.

Risiko dan Solusi

Strategi ini juga menghadapi risiko tertentu, terutama terfokus pada dua aspek:

- Risiko kegagalan pembalikan. Sinyal pembalikan itu sendiri bergantung pada peluang arbitrase statistik, sehingga tidak menutup kemungkinan adanya probabilitas kegagalan pembalikan. Risiko dapat dikendalikan dengan mengurangi ukuran posisi atau menetapkan stop loss.

- Risiko kerugian dalam kondisi pasar bullish. Secara keseluruhan, strategi ini masih mengandalkan operasi melawan tren, sehingga pasti akan mengalami beberapa kerugian dalam kondisi pasar bullish. Hal ini membutuhkan penilaian yang akurat terhadap tren besar, dan jika perlu, intervensi manual untuk melewati kondisi pasar yang tidak menguntungkan.

Arah Optimasi

Strategi ini perlu dioptimalkan dari beberapa aspek berikut ke depannya:

- Menguji berbagai instrumen untuk mencari kombinasi parameter terbaik. Meskipun strategi tidak sensitif terhadap parameter, tetap disarankan untuk mencari parameter optimal untuk setiap instrumen yang berbeda.

- Menambahkan mekanisme keluar adaptif. Dapat diuji dengan menambahkan stop loss dinamis, keluar berdasarkan waktu, dan lain-lain, sehingga strategi lebih mampu beradaptasi terhadap perubahan pasar.

- Memperkenalkan algoritma machine learning. Dapat dicoba untuk membuat model mempelajari probabilitas keberhasilan pembalikan, guna meningkatkan rasio kemenangan strategi.

Kesimpulan

Secara keseluruhan, strategi ini adalah strategi pembalikan jangka pendek. Dengan memanfaatkan kemampuan indikator RSI dalam mengidentifikasi kondisi jenuh beli dan jenuh jual, serta dibantu oleh berbagai alat bantu untuk verifikasi multi-faktor, kualitas sinyal meningkat. Strategi ini memiliki efisiensi penangkapan yang tinggi dan stabilitas yang cukup baik. Layak untuk diuji dan dioptimalkan lebih lanjut, pada akhirnya mencapai profitabilitas.

/*backtest

start: 2022-12-05 00:00:00

end: 2023-03-24 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='Ain1',title='All in One Strategy', overlay=true, initial_capital = 1000, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.18, calc_on_every_tick=true)- 1