Strategi Trading Adaptif Turtle Breakout dan Pullback

Ringkasan

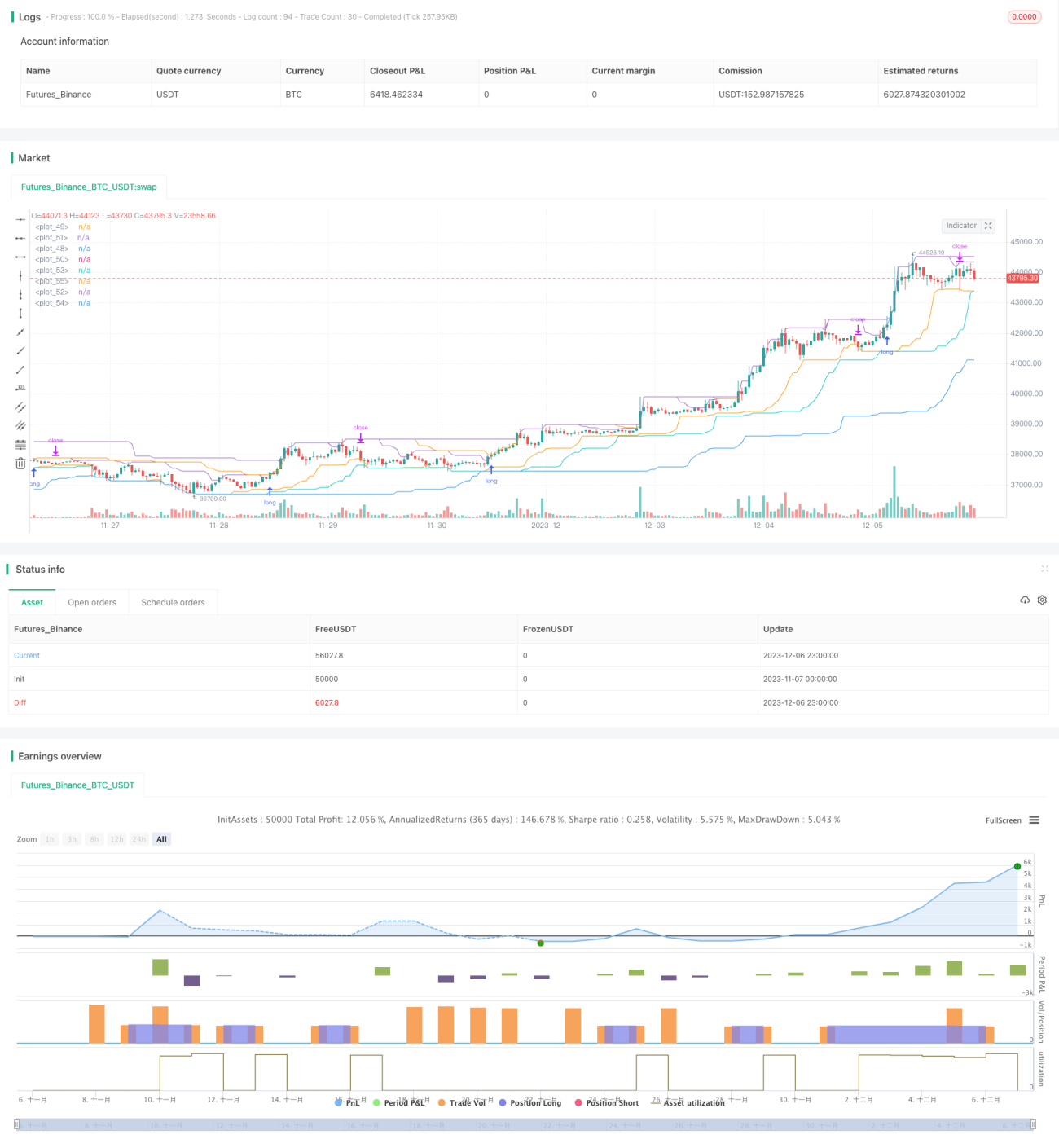

Strategi ini terutama didasarkan pada prinsip breakout tren, dikombinasikan dengan metode breakout saluran, menggunakan dual-track breakout garis cepat dan garis lambat untuk menentukan arah tren. Strategi ini memiliki perlindungan ganda berupa entry breakout dan exit pullback, sehingga dapat secara efektif menangani perubahan pasar yang tiba-tiba. Keunggulan terbesar dari strategi ini adalah dapat memantau drawdown akun secara real-time, dan ketika drawdown melebihi rasio tertentu, ukuran posisi akan secara otomatis dikurangi. Hal ini memungkinkan strategi untuk secara efektif mengendalikan risiko pasar dan kemampuan mitigasi risiko akun.

Prinsip Strategi

-

Dual-track garis cepat dan lambat: Membangun saluran menggunakan garis cepat dan garis lambat. Garis cepat memiliki respons yang lebih cepat, sementara garis lambat lebih halus. Menggabungkan breakout dual-track untuk menentukan arah tren.

-

Entry breakout: Ketika harga menembus saluran ke atas, lakukan long; ketika menembus saluran ke bawah, lakukan short. Menggunakan stop loss order untuk mengurangi risiko.

-

Exit pullback: Memantau drawdown maksimum secara real-time. Setelah mencapai titik exit drawdown, secara proaktif melakukan stop loss dan menutup posisi. Titik exit drawdown dapat disesuaikan berdasarkan kondisi pasar.

-

Ukuran posisi adaptif: Jumlah posisi disesuaikan secara real-time berdasarkan ekuitas akun untuk menghindari risiko pasar. Semakin besar drawdown akun, semakin sedikit posisi yang dipegang. Kemampuan mitigasi risiko lebih kuat.

Keunggulan Strategi

-

Saluran dual-track + entry breakout, menentukan tren dengan lebih akurat.

-

Mekanisme stop loss dan take profit, secara efektif mengendalikan kerugian per transaksi.

-

Memantau drawdown akun secara real-time, secara proaktif menyesuaikan ukuran posisi, mengurangi risiko pasar.

-

Ukuran posisi terkait dengan ekuitas akun, kemampuan mitigasi risiko kuat, dapat menangani perubahan pasar yang tiba-tiba.

Risiko Strategi

-

Dalam kondisi pasar yang sangat berfluktuasi, pengendalian drawdown mungkin gagal, menyebabkan kerugian semakin besar.

-

Ketika garis cepat memasuki area netral, mungkin muncul beberapa sinyal breakout yang tidak valid.

-

Garis lambat terlalu halus, tidak dapat menangkap pembalikan tren cepat secara tepat waktu.

-

Saat menggunakan posisi long dan short secara bersamaan, ada risiko terjebak dalam posisi dua arah.

Arah Optimasi Strategi

-

Untuk kondisi pasar yang sangat berfluktuasi, dapat menetapkan toleransi drawdown yang lebih tinggi untuk menghindari stop loss yang berlebihan.

-

Menambahkan filter area netral untuk menghindari sinyal tidak valid di area netral.

-

Mengoptimalkan parameter saluran garis lambat untuk meningkatkan kecepatan respons terhadap pergerakan cepat.

-

Menambahkan aturan urutan pembukaan posisi untuk menghindari posisi dua arah yang terjebak.

Kesimpulan

Secara keseluruhan, strategi ini merupakan strategi efektif yang cocok untuk perdagangan tren jangka menengah hingga panjang. Keunggulan terbesarnya adalah pemantauan drawdown secara real-time dan penyesuaian posisi secara dinamis. Hal ini memungkinkan strategi untuk secara otomatis menyesuaikan ukuran posisi, dengan kemampuan adaptasi pasar yang kuat. Ketika terjadi perubahan pasar yang drastis atau fluktuasi harga, strategi dapat secara otomatis mengurangi ukuran posisi, secara efektif mencegah kerugian semakin besar. Ini sulit dicapai oleh banyak strategi tradisional. Secara keseluruhan, strategi ini memiliki pendekatan yang inovatif dan kepraktisan yang kuat. Layak untuk dieksplorasi dan dioptimalkan dalam penerapannya.

//Noro

//2020

//Original idea from «Way of the Turtle: The Secret Methods that Turned Ordinary People into Legendary Traders» (2007, CURTIS FAITH, ISBN: 9780071486644)

//@version=4

strategy("Noro's Turtles Strategy", shorttitle = "Turtles str", overlay = true, default_qty_type = strategy.percent_of_equity, initial_capital = 100, default_qty_value = 100, commission_value = 0.1)

//Settings

needlong = input(true, title = "Long")

needshort = input(false, title = "Short")

sizelong = input(100, defval = 100, minval = 1, maxval = 10000, title = "Lot long, %")- 1