Strategi Kuantitatif Berdasarkan Tingkat Perubahan Harga dan Rata-rata Bergerak

Ikhtisar

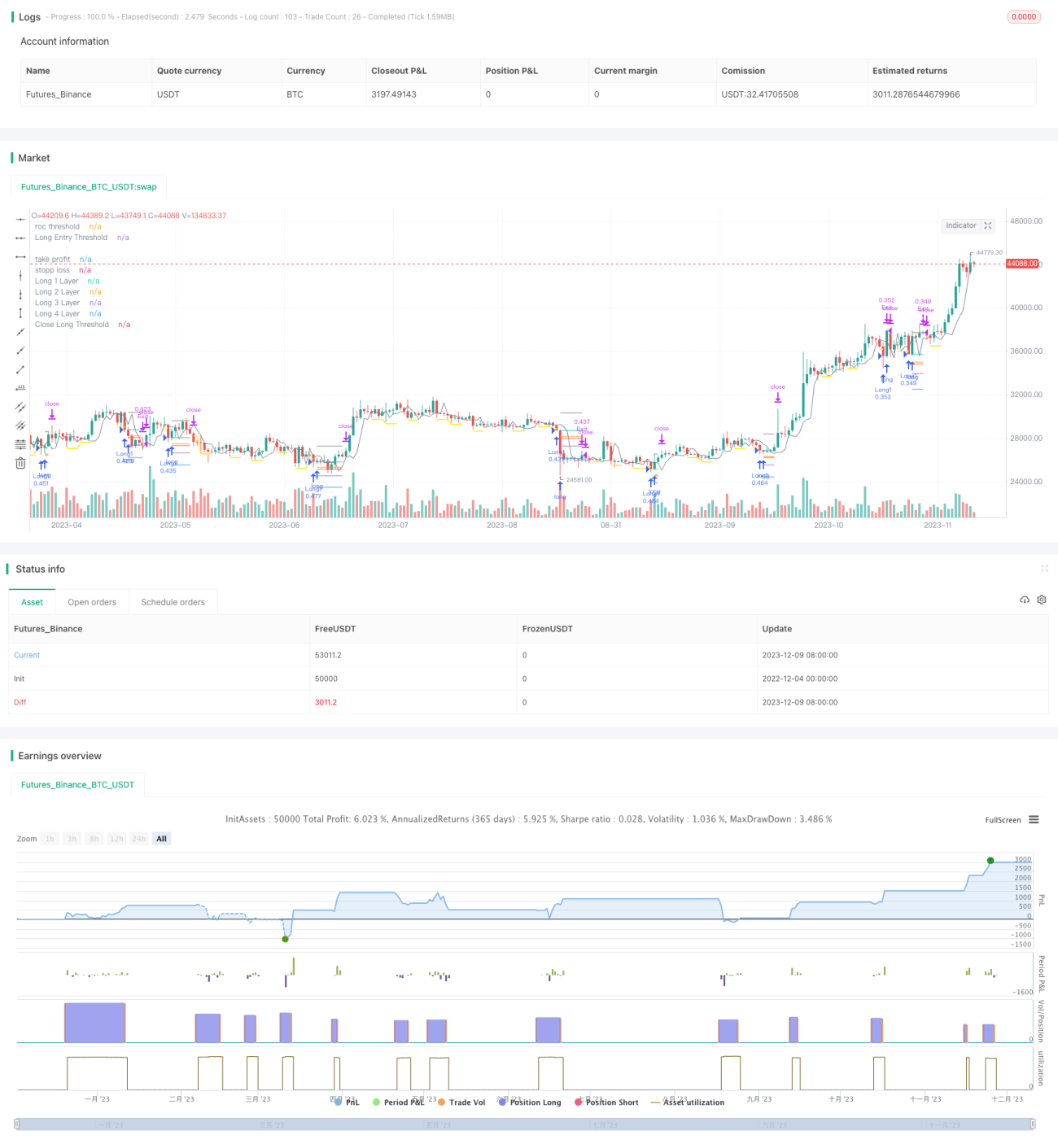

Strategi ini menggabungkan indikator teknis tingkat perubahan harga dan rata-rata bergerak untuk menempatkan titik beli dan jual secara presisi. Ketika harga mengalami penurunan signifikan, ambang beli ditetapkan, dan ketika harga turun lebih lanjut, posisi long dibuka. Ketika harga naik, ambang jual ditetapkan, dan ketika harga terus naik, posisi ditutup. Selain itu, strategi ini juga menggunakan metode penambahan posisi, membeli dalam beberapa kali untuk mengurangi biaya.

Prinsip Strategi

Logika Pembelian

- Hitung tingkat perubahan harga (ROC) dan tetapkan garis ambang beli.

- Ketika harga menembus di bawah garis ambang beli, catat titik tersebut dan aktifkan garis batas pembelian.

- Garis batas pembelian memiliki durasi sesuai parameter yang dimasukkan, dan akan ditutup setelah kedaluwarsa.

- Ketika harga terus turun dan menembus di bawah garis batas pembelian, buka posisi long pertama.

Logika Penjualan

- Hitung tingkat perubahan harga (ROC) dan tetapkan garis ambang jual.

- Ketika harga menembus di atas garis ambang jual, catat titik tersebut dan aktifkan garis batas penjualan.

- Garis batas penjualan memiliki durasi sesuai parameter yang dimasukkan, dan akan ditutup setelah kedaluwarsa.

- Ketika harga terus naik dan menembus di atas garis batas penjualan, tutup semua posisi long.

Kontrol Risiko

Strategi ini dilengkapi dengan fungsi stop loss dan take profit yang dapat disesuaikan parameternya, untuk mengontrol risiko posisi yang ada secara real-time.

Metode Penambahan Posisi

Setiap kali posisi trading dibuka, harga pembelian berikutnya ditetapkan dengan rasio tertentu berdasarkan parameter yang dimasukkan, sehingga mencapai efek penambahan posisi secara bertahap.

Analisis Keunggulan

- Menggunakan indikator tingkat perubahan harga (ROC) untuk menemukan titik beli dan jual, ROC sangat sensitif terhadap perubahan harga, sehingga penempatan titik beli dan jual akurat.

- Menggunakan metode garis batas untuk lebih memastikan waktu masuk/keluar, menghindari breakout palsu.

- Metode penambahan posisi memungkinkan pelacakan nilai pasar dengan tetap menjaga risiko terkendali.

- Dilengkapi dengan fungsi stop loss dan take profit untuk mengontrol risiko setiap posisi secara ketat.

Risiko dan Solusi

- Ketika pasar mengalami volatilitas ekstrem, strategi dapat membuka terlalu banyak posisi. Solusinya adalah dengan mengatur parameter penambahan posisi secara wajar dan mengontrol jumlah total posisi.

- Ketika tren harga sideways tidak jelas, harga stop loss atau take profit mungkin sering terpicu. Ambang stop loss/take profit dapat diperlonggar atau fitur tersebut dimatikan.

Saran Optimasi

- Gabungkan dengan indikator lain untuk memfilter waktu masuk. Misalnya, dengan rata-rata bergerak, hanya percaya pada sinyal ROC ketika harga menembus di bawah rata-rata bergerak.

- Optimalkan logika penambahan posisi, hanya aktifkan penambahan posisi jika kondisi tertentu terpenuhi. Misalnya, hanya menambah posisi jika harga turun lagi melebihi batas tertentu.

- Parameter untuk instrumen yang berbeda akan sangat bervariasi, diperlukan backtest dan simulasi trading yang cukup untuk mendapatkan kombinasi parameter terbaik.

- Dapat mengatur stop loss dan take profit adaptif, menetapkan level stop loss yang berbeda sesuai dengan volatilitas pasar.

Kesimpulan

Strategi ini menggabungkan indikator ROC untuk menempatkan titik beli dan jual secara presisi, metode garis batas untuk memfilter sinyal, stop loss/take profit bawaan untuk mengelola risiko, dan penambahan posisi untuk memperbesar keuntungan. Dengan pengaturan parameter yang wajar, strategi ini dapat memperoleh keuntungan lebih sambil menjaga risiko dalam batas terkendali. Ke depannya, mekanisme filter sinyal dan kontrol risiko dapat dioptimalkan lebih lanjut agar strategi ini dapat beradaptasi dengan lebih banyak kondisi pasar.

- 1