Strategi Backtesting Volatilitas Statistik Berdasarkan Metode Nilai Ekstrem

Ikhtisar

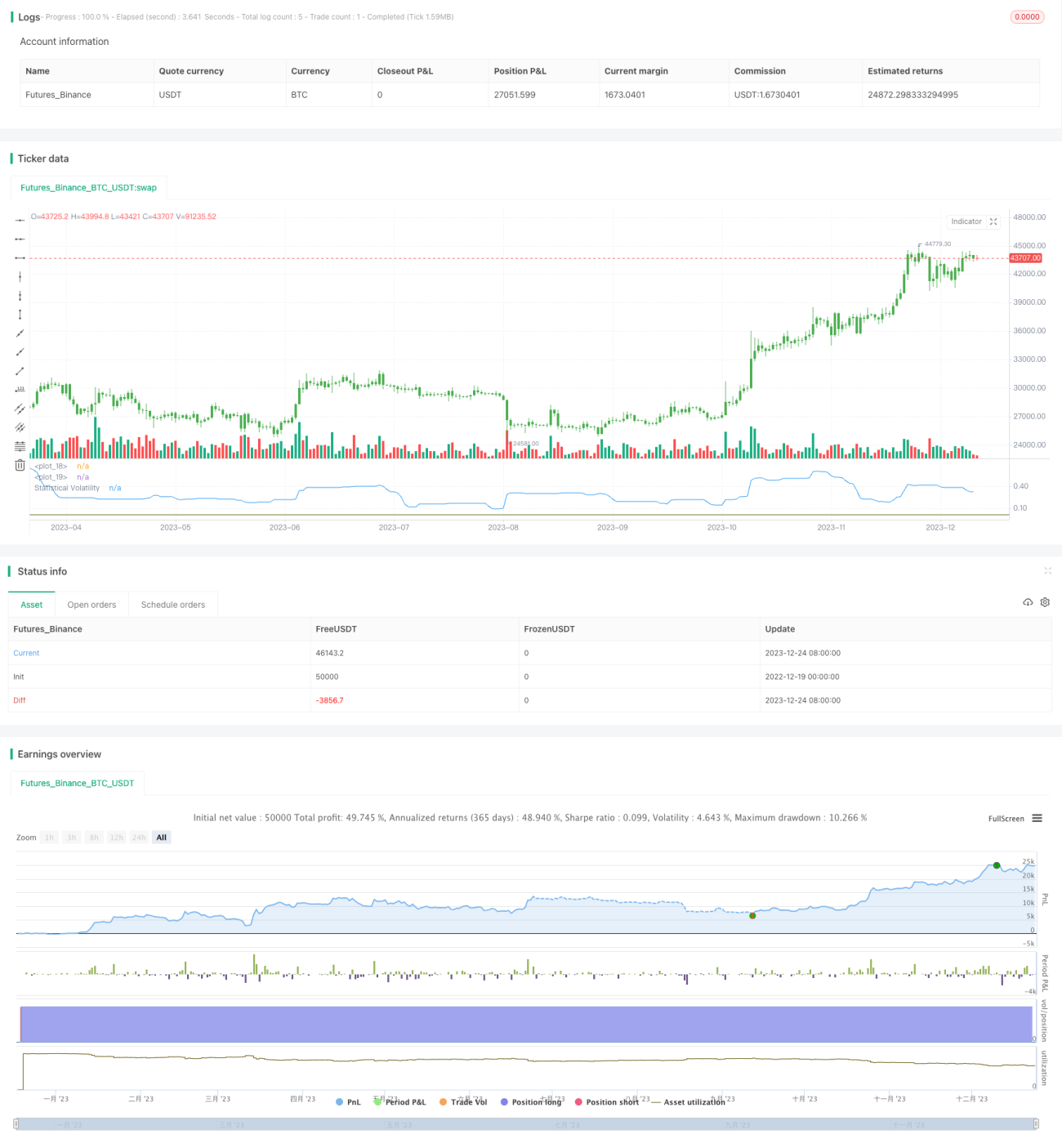

Strategi ini menggunakan metode ekstrim untuk menghitung volatilitas statistik, yang juga dikenal sebagai volatilitas historis. Volatilitas ini dihitung berdasarkan nilai ekstrim dari harga tertinggi, harga terendah, dan harga penutupan, dengan mempertimbangkan faktor waktu. Volatilitas ini mencerminkan fluktuasi harga aset. Strategi akan melakukan posisi beli atau jual ketika volatilitas berada di atas atau di bawah ambang batas yang ditetapkan.

Prinsip Strategi

- Hitung nilai ekstrim dari harga tertinggi, harga terendah, dan harga penutupan dalam periode waktu tertentu.

- Terapkan rumus metode ekstrim untuk menghitung volatilitas statistik:SqrTime = sqrt(253 / Length) Vol = ((0.6 * log(xMaxC / xMinC) * SqrTime) + (0.6 * log(xMaxH / xMinL) * SqrTime)) * 0.5

- Bandingkan volatilitas dengan ambang batas atas dan bawah yang ditetapkan untuk menghasilkan sinyal trading:pos = iff(nRes > TopBand, 1, iff(nRes < LowBand, -1, nz(pos[1], 0)))

- Lakukan posisi beli atau jual berdasarkan sinyal trading.

Analisis Kelebihan

Kelebihan utama strategi ini antara lain:

- Menggunakan indikator volatilitas statistik dapat secara efektif menangkap peluang pergerakan panas dan pembalikan pasar.

- Metode ekstrim dalam menghitung volatilitas tidak sensitif terhadap harga ekstrem, sehingga hasilnya lebih stabil dan andal.

- Parameter dapat disesuaikan untuk beradaptasi dengan lingkungan volatilitas yang berbeda.

Analisis Risiko

Risiko utama strategi ini meliputi:

- Volatilitas statistik sendiri memiliki keterlambatan tertentu, sehingga tidak dapat secara tepat menangkap titik balik pasar.

- Indikator volatilitas bereaksi lambat terhadap peristiwa tak terduga, sehingga mungkin melewatkan peluang trading jangka pendek.

- Terdapat risiko sinyal palsu dan risiko stop loss.

Langkah penanganan dan solusi:

- Persingkat periode statistik secara tepat untuk meningkatkan sensitivitas terhadap perubahan pasar.

- Gabungkan dengan indikator lain sebagai pendukung untuk meningkatkan akurasi sinyal.

- Tetapkan titik stop loss untuk mengendalikan kerugian per transaksi.

Arah Optimasi

Arah optimasi strategi ini:

- Uji parameter periode statistik yang berbeda untuk menemukan parameter optimal.

- Tambahkan modul manajemen posisi untuk menyesuaikan ukuran posisi berdasarkan volatilitas.

- Gabungkan dengan indikator seperti moving average untuk menetapkan kondisi penyaringan guna mengurangi sinyal palsu.

Kesimpulan

Strategi ini menggunakan metode ekstrim untuk menghitung volatilitas statistik dan menghasilkan sinyal trading dengan menangkap perubahan volatilitas yang tidak biasa. Dibandingkan dengan indikator seperti simple moving average, strategi ini lebih mencerminkan volatilitas pasar dan menangkap pembalikan. Selain itu, algoritma metode ekstrim membuat hasil lebih stabil dan andal. Melalui penyesuaian dan optimasi parameter, strategi ini dapat beradaptasi dengan berbagai kondisi pasar; ide trading dan indikator volatilitas statistik ini layak untuk diteliti dan diterapkan lebih lanjut.

/*backtest

start: 2022-12-19 00:00:00

end: 2023-12-25 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 22/11/2014

// This indicator used to calculate the statistical volatility, sometime - 1