Strategi Rasio Moving Average Berantai dengan Filter Tren Ganda

Ikhtisar

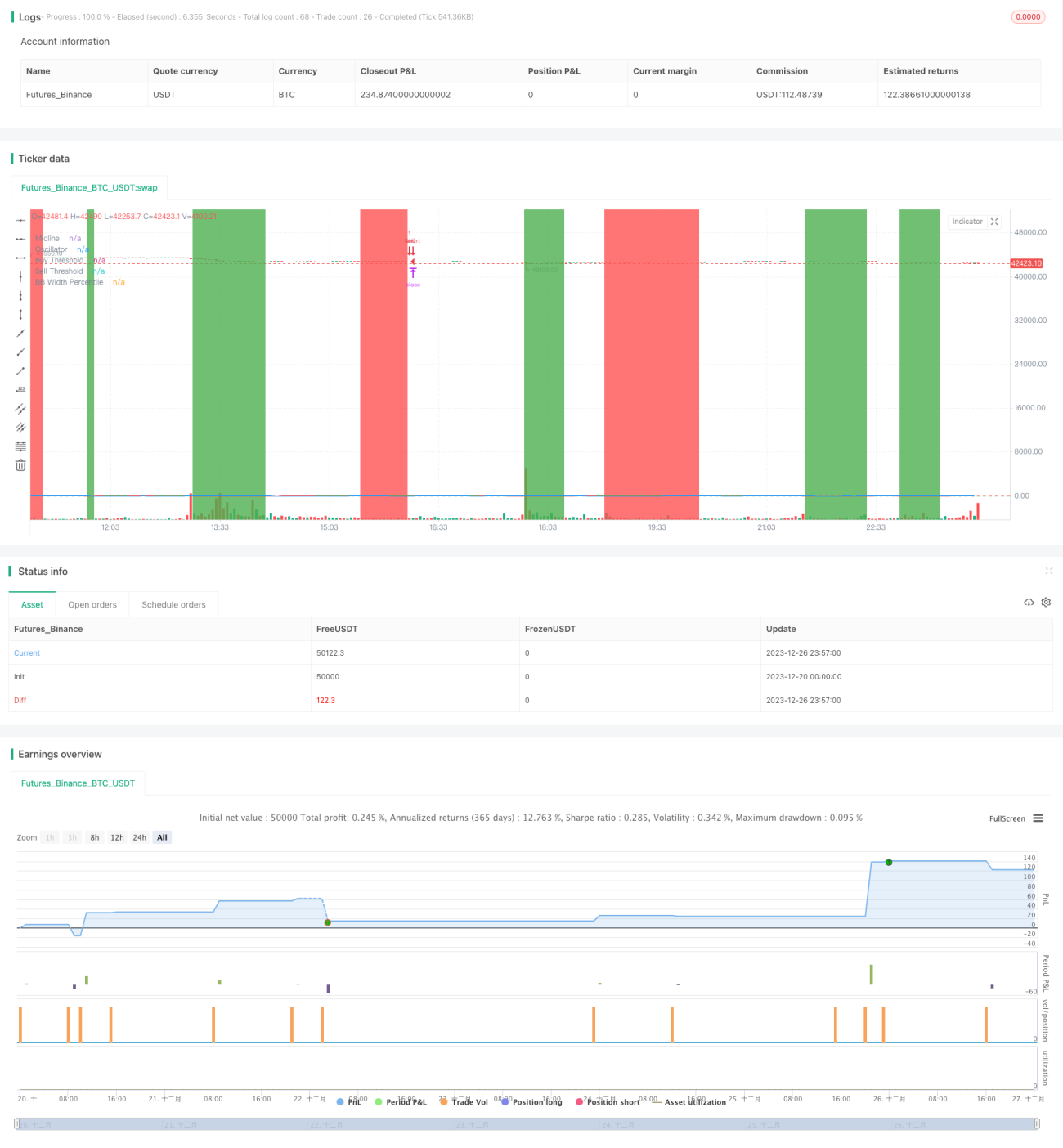

Strategi ini adalah strategi pengikut tren yang didasarkan pada indikator rasio rata-rata bergerak ganda, dikombinasikan dengan filter Bollinger Bands dan indikator filter tren ganda, serta menggunakan mekanisme keluar berantai. Strategi ini bertujuan untuk mengidentifikasi arah tren jangka menengah-panjang menggunakan indikator rasio rata-rata bergerak, memilih titik masuk yang baik ketika arah tren sudah jelas, dan menetapkan mekanisme keluar take-profit dan stop-loss untuk mengunci keuntungan serta mengurangi kerugian.

Prinsip Strategi

- Hitung rata-rata bergerak cepat (garis 10 hari) dan rata-rata bergerak lambat (garis 50 hari), lalu hitung rasionya, yang disebut rasio rata-rata bergerak harga. Rasio ini dapat secara efektif mengidentifikasi perubahan tren jangka menengah-panjang harga.

- Ubah rasio rata-rata bergerak harga menjadi persentil, yaitu kekuatan relatif rasio saat ini dalam periode waktu tertentu. Persentil ini didefinisikan sebagai osilator.

- Ketika osilator menembus ke atas ambang beli yang ditetapkan (10), sinyal beli dihasilkan; ketika menembus ke bawah ambang jual (90), sinyal jual dihasilkan, mengikuti tren.

- Filter sinyal perdagangan dengan indikator lebar Bollinger Bands; lakukan operasi saat Bollinger Bands menyempit.

- Gunakan indikator filter tren ganda; sinyal beli hanya dihasilkan ketika harga berada dalam saluran tren naik, dan sinyal jual hanya ketika harga berada dalam saluran tren turun, sehingga menghindari operasi melawan tren.

- Tetapkan mekanisme keluar berantai, termasuk take-profit, stop-loss, dan keluar kombinasi, dengan beberapa kondisi keluar yang dapat ditetapkan sebelumnya, dan prioritaskan keluar dari kondisi yang memberikan keuntungan paling besar.

Keunggulan Strategi

- Mekanisme filter tren ganda, andal dalam menentukan arah tren utama, menghindari operasi melawan tren.

- Indikator rasio rata-rata bergerak lebih efektif daripada rata-rata bergerak tunggal dalam menentukan perubahan tren.

- Indikator lebar Bollinger Bands dapat secara efektif mengidentifikasi periode volatilitas rendah pasar, di mana sinyal perdagangan lebih andal.

- Mekanisme keluar berantai membuat keuntungan lebih stabil, memaksimalkan seluruh laba.

Risiko dan Solusinya

- Dalam kondisi pasar yang bergerak sideways tanpa tren yang jelas, akan muncul lebih banyak sinyal palsu dan pembalikan. Solusinya adalah dengan menggabungkan filter lebar Bollinger Bands, lakukan operasi saat menyempit.

- Ketika terjadi pembalikan tren yang jelas, rata-rata bergerak akan mengalami keterlambatan dan tidak dapat segera mendeteksi sinyal pembalikan. Solusinya adalah dengan memperpendek parameter periode rata-rata bergerak secara tepat.

- Ketika terjadi gap harga, titik stop-loss dapat terkena secara instan, menyebabkan kerugian besar. Solusinya adalah dengan melonggarkan parameter stop-loss secara tepat.

Arah Optimasi Strategi

- Optimasi parameter. Lakukan pengujian menyeluruh pada periode rata-rata bergerak, titik beli/jual osilator, parameter Bollinger Bands, dan parameter filter tren untuk menemukan kombinasi parameter terbaik.

- Integrasi indikator lain. Pertimbangkan untuk menambahkan indikator lain yang mendeteksi pembalikan tren, seperti indikator KD, MACD, dll., untuk meningkatkan akurasi strategi.

- Pembelajaran mesin. Kumpulkan data historis, gunakan algoritma pembelajaran mesin untuk melatih model, optimalkan berbagai parameter secara dinamis, sehingga mencapai penyesuaian parameter secara adaptif.

Ringkasan

Strategi ini secara komprehensif menggunakan indikator rasio rata-rata bergerak ganda dan indikator Bollinger Bands untuk menentukan arah tren jangka menengah-panjang. Setelah mengonfirmasi tren, strategi mencari titik masuk terbaik, dan menetapkan mekanisme keluar berantai untuk mengunci keuntungan. Strategi ini memiliki keandalan yang tinggi dan hasil yang nyata. Strategi ini dapat ditingkatkan lebih lanjut melalui optimasi parameter, penambahan indikator bantu lainnya, dan pembelajaran mesin untuk meningkatkan tingkat keuntungan.

- 1