Strategi Investasi Berkala dengan Rata-rata Biaya Dinamis dan Bunga Majemuk

Gambaran Umum

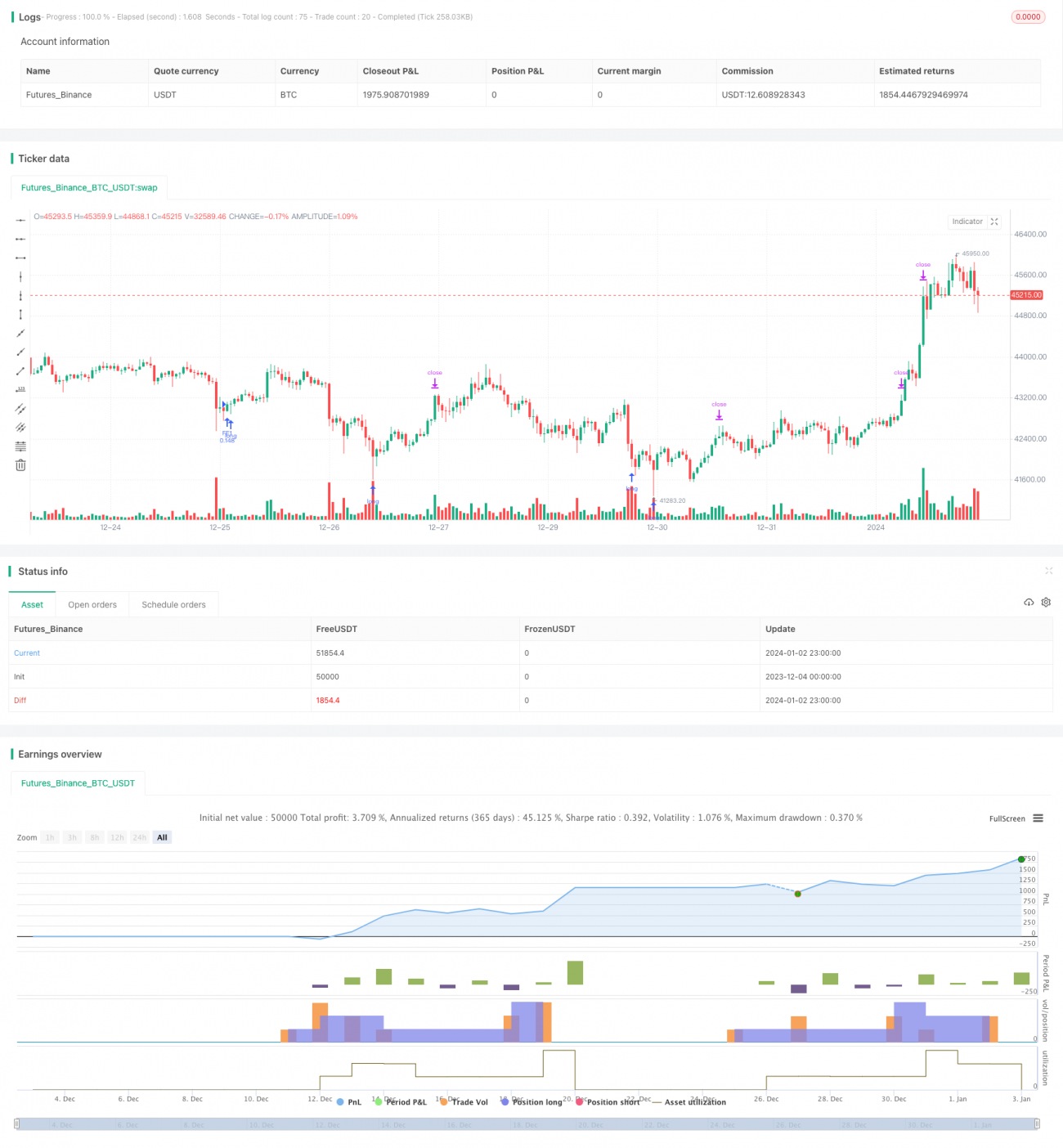

Strategi DCA (Dollar Cost Averaging) dengan bunga majemuk biaya rata-rata dinamis menyesuaikan jumlah posisi yang dibuka setiap kali, dengan membuka posisi kecil di awal fase tren, kemudian secara bertahap meningkatkan ukuran posisi seiring dengan bertambahnya kedalaman konsolidasi. Strategi ini menggunakan fungsi eksponensial untuk menghitung level stop loss setiap lapisan, dan memicu pembukaan posisi baru secara bertahap, sehingga garis biaya kepemilikan dapat turun secara eksponensial. Seiring bertambahnya kedalaman, biaya posisi dapat ditekan secara bertahap ke bawah, dan setelah harga berbalik, posisi ditutup secara bertahap untuk meraih keuntungan yang lebih besar.

Prinsip Strategi

Strategi ini menggunakan sinyal oversold sederhana dari RSI yang dikombinasikan dengan metode pemilihan waktu berdasarkan moving average untuk menentukan waktu pembukaan posisi. Ketika RSI berada di bawah garis oversold dan harga penutupan lebih kecil dari moving average, sinyal pembukaan posisi pertama dihasilkan. Setelah posisi pertama dibuka, berdasarkan fungsi eksponensial, batas bawah penurunan harga dihitung untuk menghasilkan sinyal DCA. Setiap kali DCA dilakukan, jumlah posisi disesuaikan sehingga setiap lot memiliki ukuran yang sama. Karena perubahan dinamis dalam jumlah posisi dan biaya kepemilikan, hal ini menciptakan efek leverage.

Seiring bertambahnya frekuensi DCA, biaya kepemilikan terus menurun, sehingga hanya diperlukan sedikit kenaikan harga untuk mencapai keuntungan saat take profit. Setelah beberapa posisi dibuka berturut-turut, garis stop loss akan digambar di atas harga rata-rata. Begitu harga menembus ke atas melewati harga rata-rata kepemilikan dan garis stop loss, posisi akan ditutup untuk menghentikan kerugian.

Keuntungan terbesar dari strategi ini adalah seiring dengan turunnya biaya kepemilikan, bahkan dalam pasar yang berkonsolidasi, biaya dapat dikurangi secara bertahap. Ketika tren berbalik, karena biaya kepemilikan sudah jauh di bawah harga pasar, keuntungan yang lebih besar dapat diraih.

Risiko dan Kekurangan

Risiko terbesar dari strategi ini adalah keterbatasan posisi awal. Jika terjadi penurunan tren yang berkelanjutan, ada risiko stop loss. Oleh karena itu, perlu menetapkan tingkat stop loss yang dapat ditoleransi.

Selain itu, penetapan tingkat stop loss juga memiliki dua ekstrem. Jika stop loss terlalu besar, unit yang berhenti tidak akan mendapatkan cukup kedalaman rebound. Sebaliknya, jika stop loss terlalu kecil, kemungkinan harga berbalik dan naik lagi dalam penyesuaian jangka menengah akan lebih besar. Oleh karena itu, sangat penting untuk memilih tingkat stop loss yang sesuai berdasarkan pasar yang berbeda dan toleransi risiko pribadi.

Jika periode DCA panjang dan terbentuk banyak level, ketika harga naik secara signifikan, akan menghadapi risiko biaya posisi yang terlalu tinggi dan tidak dapat melakukan stop loss. Ini juga perlu disesuaikan secara wajar dengan total posisi dan biaya posisi maksimum yang dapat ditanggung.

Saran Optimalisasi

-

Optimalkan sinyal pemilihan waktu. Dapat menguji parameter yang berbeda dan kombinasi indikator yang berbeda untuk memilih sinyal dengan tingkat kemenangan yang lebih tinggi.

-

Optimalkan mekanisme stop loss. Dapat menguji penggunaan stop loss berbentuk Λ atau stop loss berbentuk busur untuk menggantikan stop loss bergerak sederhana, yang mungkin memberikan efek stop loss yang lebih baik. Juga dapat menambahkan strategi penyesuaian stop loss berdasarkan waktu posisi.

-

Optimalkan metode take profit. Dapat menguji berbagai jenis take profit bergerak untuk mencari peluang keluar take profit yang lebih baik, sehingga meningkatkan tingkat pengembalian keseluruhan.

-

Tambahkan mekanisme anti-rebound. Setelah stop loss, mungkin terjadi sinyal DCA lagi yang menyebabkan pembukaan posisi kembali. Dalam hal ini, dapat dipertimbangkan untuk menambahkan rentang anti-rebound dengan besaran tertentu untuk menghindari pembukaan posisi secara agresif segera setelah stop loss.

Kesimpulan

Strategi ini menggunakan indikator RSI untuk menentukan waktu beli, serta strategi DCA dinamis dengan stop loss yang dihitung berdasarkan fungsi eksponensial, untuk menyesuaikan jumlah posisi dan biaya kepemilikan secara dinamis, sehingga memperoleh keunggulan harga di pasar rentang. Optimalisasi terutama berfokus pada sinyal masuk dan keluar, cara stop loss dan take profit, dll. Secara keseluruhan, strategi ini menggunakan inti konsep DCA eksponensial, yang membuat biaya kepemilikan terus turun, memberikan lebih banyak ruang operasi selama konsolidasi, dan menghasilkan pengembalian yang lebih tinggi dalam tren pergerakan. Namun, tetap perlu memilih parameter yang sesuai berdasarkan rencana manajemen modal untuk mengendalikan risiko posisi secara keseluruhan.

- 1