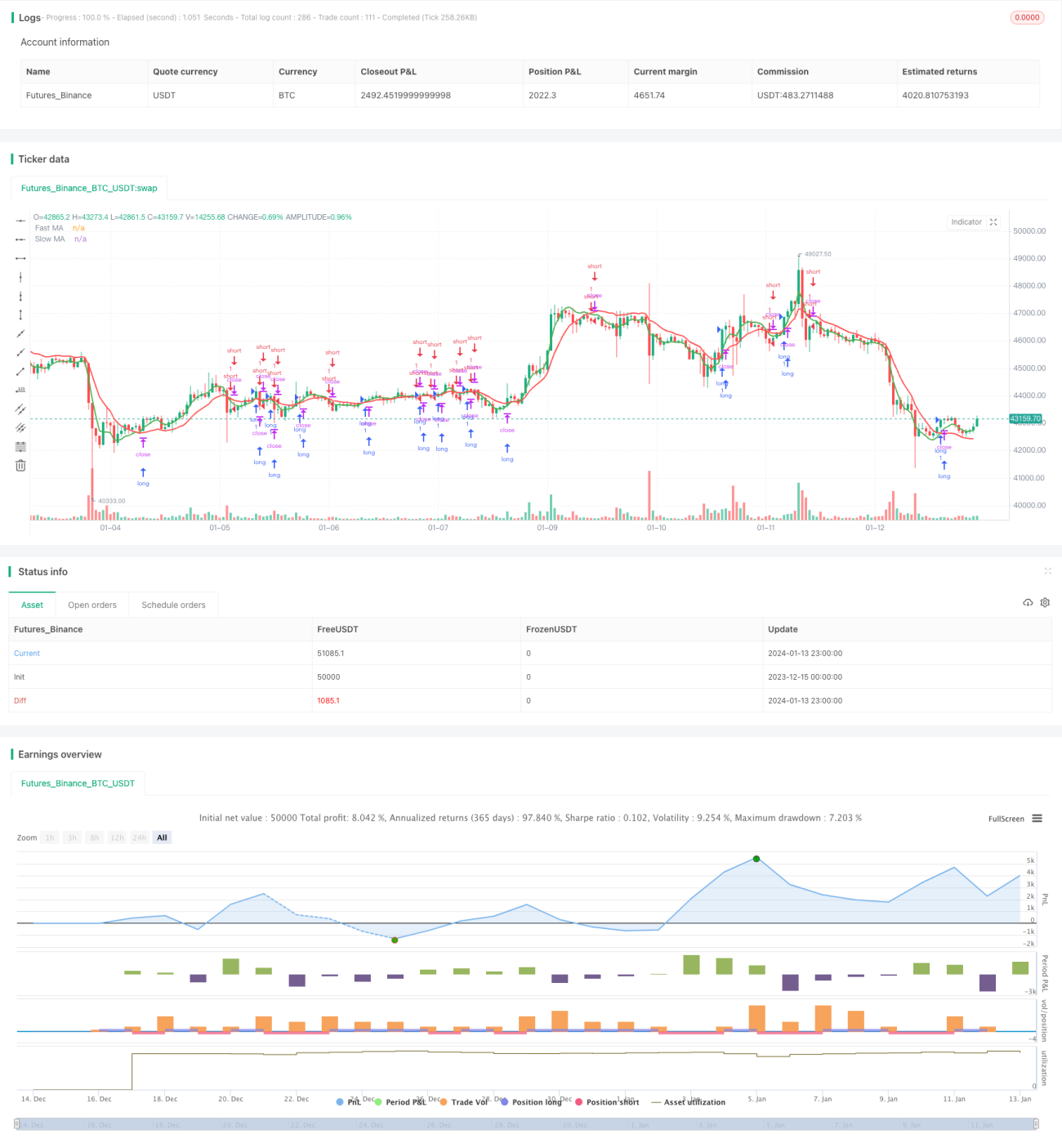

Strategi Persilangan Kombinasi Sebelas Rata-rata Bergerak

Ikhtisar

Strategi ini menggabungkan persilangan dari 11 jenis rata-rata bergerak (moving average) yang berbeda untuk melakukan posisi long (beli) dan short (jual). Kesebelas moving average yang digunakan meliputi: Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), Volume-Weighted Moving Average (VWMA), Smoothed Moving Average (SMMA), Double Exponential Moving Average (DEMA), Triple Exponential Moving Average (TEMA), Hull Moving Average (HMA), Zero-Lag Exponential Moving Average (ZEMA), Triangular Moving Average (TMA), dan Super Smoother Filter (SSMA).

Strategi ini memungkinkan konfigurasi dua moving average – satu yang lebih cepat dan satu yang lebih lambat, keduanya dipilih dari 11 pilihan. Ketika MA yang lebih cepat melintasi di atas MA yang lebih lambat, sinyal long dihasilkan. Ketika MA yang lebih cepat melintasi di bawah MA yang lebih lambat, sinyal short dihasilkan.

Fitur tambahan termasuk pengaturan pyramiding, level take-profit, dan stop-loss.

Logika Strategi

Logika inti strategi bergantung pada persilangan antara dua moving average untuk menentukan entry dan exit.

Kondisi masuk adalah:

Long entry: MA cepat > MA lambat

Short entry: MA cepat < MA lambat

Exit ditentukan oleh salah satu dari tiga kriteria berikut:

- Level take-profit tercapai

- Level stop-loss tercapai

- Sinyal berlawanan dihasilkan (moving average bersilangan ke arah sebaliknya)

Strategi ini memungkinkan konfigurasi parameter kunci seperti tipe dan panjang MA, pengaturan pyramiding, serta persentase take-profit dan stop-loss. Ini memberikan fleksibilitas untuk mengoptimalkan strategi sesuai dengan kondisi pasar dan preferensi risiko yang berbeda.

Kelebihan

- Menggabungkan 11 jenis MA yang berbeda untuk menghasilkan sinyal yang kuat

- Konfigurasi parameter utama yang fleksibel

- Fungsi take-profit dan stop-loss melindungi keuntungan dan membatasi kerugian

- Pyramiding memungkinkan penambahan posisi dalam tren yang kuat

Risiko

- Seperti indikator teknis lainnya, persilangan MA dapat menghasilkan sinyal palsu

- Over-optimasi pada kondisi pasar saat ini dapat mengurangi kinerja di masa depan

- Stop-loss keras dapat menutup posisi yang benar lebih awal pada pasar yang volatil

Manajemen risiko dapat diperkuat dengan menggunakan konfirmasi harga untuk sinyal masuk, menggunakan trailing stop-loss alih-alih stop-loss keras, dan menghindari over-optimasi.

Ruang Optimasi

Strategi ini dapat ditingkatkan melalui beberapa cara:

- Menambahkan filter tambahan sebelum entry, seperti volume dan pemeriksaan harga

- Menguji secara sistematis kinerja berbagai jenis MA dan memilih 1-2 yang terbaik

- Mengoptimalkan panjang MA untuk instrumen dan kerangka waktu tertentu

- Menggunakan trailing stop-loss sebagai pengganti stop-loss keras

- Menambahkan take-profit bertahap saat tren berlanjut

Kesimpulan

Strategi persilangan sebelas moving average menyediakan pendekatan sistematis untuk trading dengan persilangan. Dengan menggabungkan sinyal dari berbagai indikator MA dan memungkinkan konfigurasi parameter kunci, strategi ini menawarkan kerangka trading yang kuat dan fleksibel. Optimasi dan manajemen risiko akan memainkan peran kunci dalam menyempurnakan kinerja. Strategi ini memiliki potensi yang kuat dalam trading momentum, tetapi harus disesuaikan dengan kondisi pasar yang berbeda.

- 1