Strategi Kuantitatif Kombinasi Triple Moving Average dan MACD

Ikhtisar

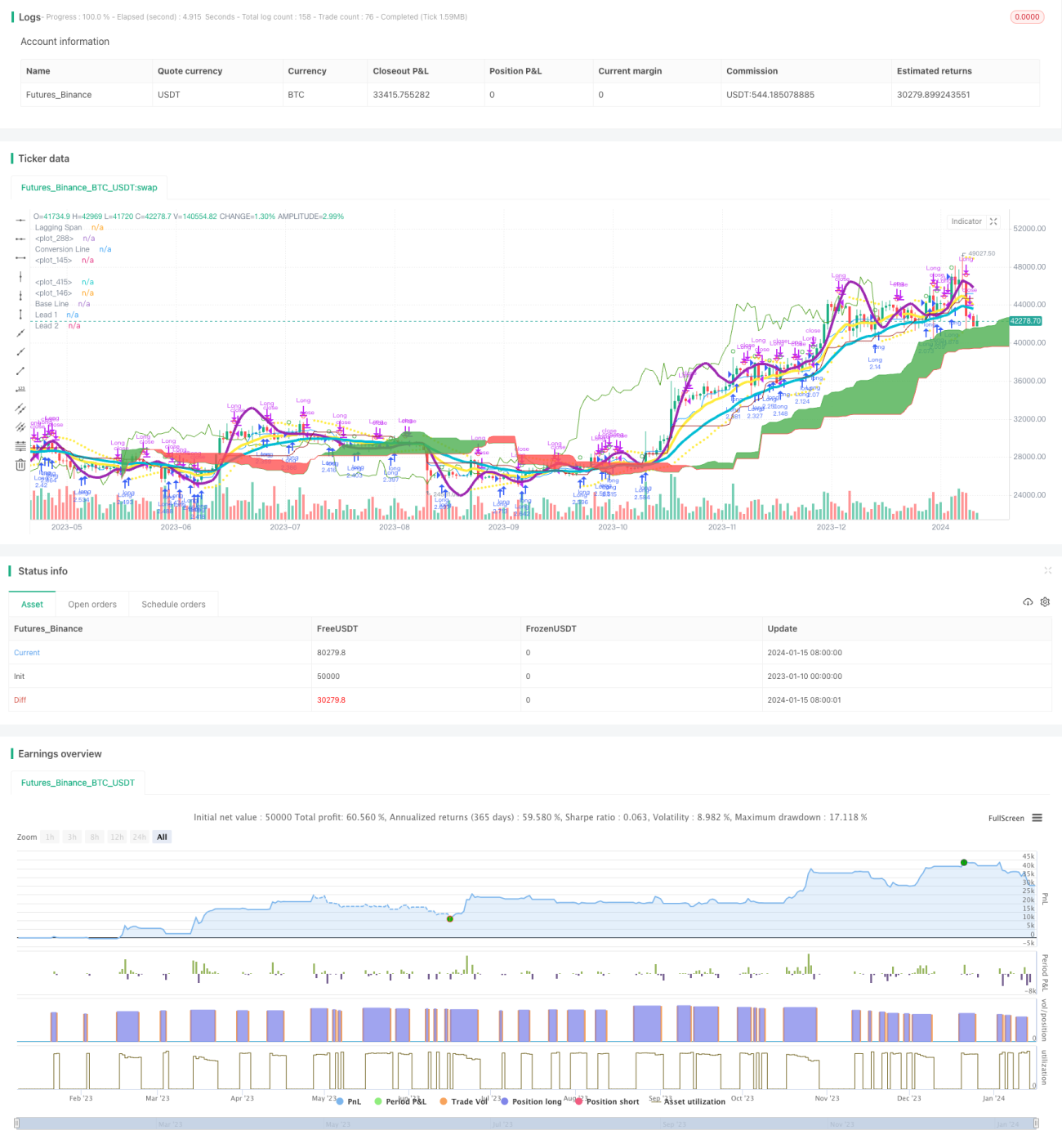

Strategi ini mengembangkan strategi trading kuantitatif yang cukup stabil dan andal dengan menggabungkan indikator Triple Exponential Moving Average dan indikator MACD. Strategi ini bertujuan untuk menangkap tren yang mungkin muncul di masa depan, dan sangat cocok untuk posisi jangka menengah hingga panjang.

Prinsip Strategi

Strategi ini terutama didasarkan pada kombinasi antara Triple Exponential Moving Average dan indikator MACD.

Pertama, strategi menggunakan tiga garis moving average eksponensial dengan panjang masing-masing 3, 7, dan 2. Ketiga moving average ini membentuk sistem moving average dari yang cepat ke lambat untuk menentukan arah tren di masa depan. Ketika moving average jangka pendek melintasi ke atas moving average jangka panjang, itu adalah sinyal beli (long); ketika moving average jangka pendek melintasi ke bawah moving average jangka panjang, itu adalah sinyal jual (short).

Kedua, strategi juga secara bersamaan menggunakan indikator MACD dengan parameter 3 dan 7. Ketika garis utama MACD melintasi ke atas garis sinyal, itu adalah sinyal beli; ketika melintasi ke bawah, itu adalah sinyal jual.

Dengan menggabungkan dua indikator, strategi ini dapat menghindari banyak sinyal palsu yang disebabkan oleh satu indikator saja, sehingga meningkatkan stabilitas strategi.

Keunggulan Strategi

- Menggunakan filter dua indikator untuk meningkatkan kualitas sinyal

- Parameter telah dioptimalkan melalui banyak pengujian, stabil dan andal

- Menggunakan sistem Triple Moving Average, yang secara efektif dapat menyaring noise pasar dan menentukan tren masa depan

- Parameter MACD diatur cukup cepat untuk menangkap peluang jangka pendek dengan cepat

Risiko Strategi

- Terdapat risiko drawdown dan kerugian beruntun

- Ketika pasar tidak memiliki tren yang jelas, strategi ini akan menghasilkan lebih banyak transaksi yang salah

- Indikator MACD rentan menghasilkan sinyal palsu, perlu dikombinasikan dengan indikator moving average

Solusi:

- Menggunakan strategi stop-loss yang tepat untuk mengontrol drawdown maksimum

- Mengurangi frekuensi trading ketika kondisi pasar jelas tidak memiliki tren

- Mengoptimalkan parameter MACD dan menggabungkannya dengan indikator lain

Arah Optimasi Strategi

- Menguji dan mengoptimalkan parameter moving average dan MACD untuk menemukan kombinasi terbaik

- Menambahkan indikator bantu seperti KDJ, VRSI untuk menghindari sinyal palsu

- Menambahkan model machine learning untuk menilai kondisi pasar guna mencapai penyesuaian dinamis

- Menggabungkan strategi stop-loss untuk menetapkan titik stop-loss yang optimal

Kesimpulan

Strategi ini mencapai penangkapan tren yang stabil melalui kombinasi moving average dan MACD. Keunggulannya terletak pada penggunaan kombinasi indikator yang secara efektif mengurangi sinyal palsu, sehingga menghasilkan kinerja strategi yang lebih baik. Langkah selanjutnya adalah menyempurnakan strategi ini melalui optimasi parameter, penerapan strategi stop-loss, penyesuaian dinamis, dan cara lainnya, sehingga menjadi alat yang efektif untuk mencari peluang jangka menengah hingga panjang.

/*backtest

start: 2023-01-10 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Matt's MACD Algo v1", shorttitle="Matt's MACD Algo v1", overlay=true, pyramiding = 0, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=7000, calc_on_order_fills = true, commission_type=strategy.commission.percent, commission_value=0, currency = currency.USD)

//study("MFI Fresh", shorttitle="MFI Fresh", overlay=true)

- 1