Strategi Perdagangan Terarah Momentum Ganda Sensitif Harga PPO

Ringkasan

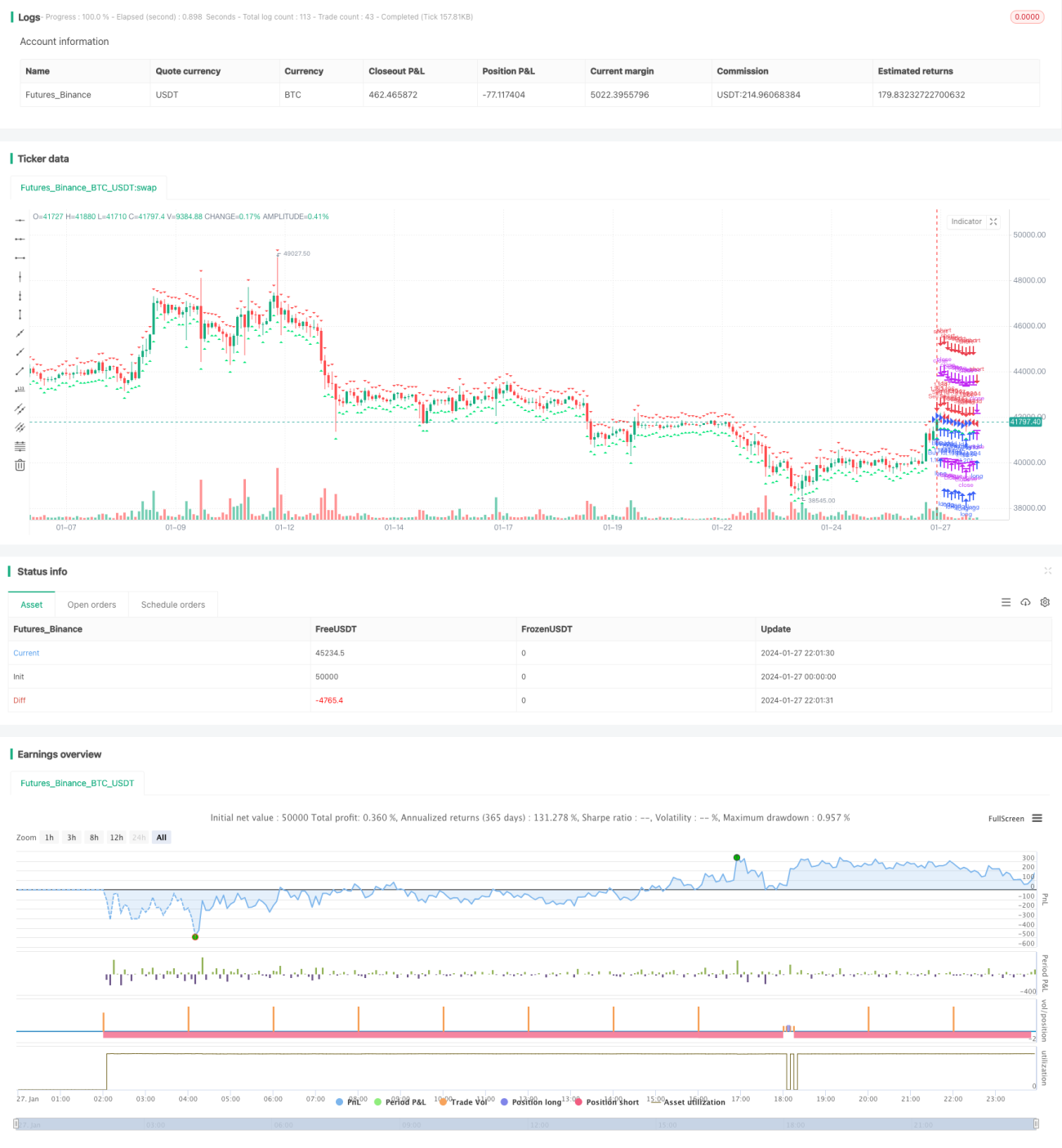

PPO Price Sensitivity Dynamics Binary Bottom Oriented Trading Strategy adalah strategi perdagangan yang menggunakan indikator price sensitivity dynamics untuk mengidentifikasi dan melacak tren pembentukan harga biner. Ini menggabungkan penilaian pembentukan biner indikator PPO dan penilaian karakteristik pergerakan harga, untuk mencapai lokasi yang tepat dari titik balik biner harga, sehingga menghasilkan sinyal perdagangan.

Prinsip Strategi

Strategi ini menggunakan indikator PPO untuk menilai karakteristik harga double bottom, sekaligus menentukan titik terendah harga, dan memantau secara real time apakah indikator PPO menunjukkan karakteristik dasar. Ketika indikator PPO menunjukkan bentuk double bottom yang berbalik dari bawah ke atas, menunjukkan saat ini berada di titik peluang beli.

Di sisi lain, strategi ini bekerja dengan penilaian nilai minimum harga untuk menentukan apakah harga berada di level yang lebih rendah. Ketika harga berada di level yang lebih rendah, sinyal beli akan dihasilkan jika indikator PPO menunjukkan ciri-ciri bawah.

Dengan penilaian ganda dari penilaian karakteristik pembalikan indikator PPO dan konfirmasi posisi harga, peluang pembalikan harga dapat diidentifikasi secara efektif, beberapa sinyal palsu dapat disaring, dan kualitas sinyal dapat ditingkatkan.

Analisis Keunggulan

-

Dengan menggunakan indikator PPO yang memiliki dua dasar, Anda dapat menentukan kapan tepat waktu untuk membeli.

-

Kombinasi dengan penentuan posisi harga, dapat memfilter sinyal palsu yang dihasilkan dari titik yang lebih tinggi, meningkatkan kualitas sinyal.

-

Indikator PPO sensitif, dapat menangkap tren perubahan harga dengan cepat, cocok untuk pelacakan tren.

-

Menggunakan mekanisme double confirmation dapat secara efektif mengurangi risiko transaksi.

Risiko dan Solusi

-

Indikator PPO mudah menghasilkan sinyal palsu, perlu ditambah dengan indikator lain untuk konfirmasi. Dapat ditambah dengan indikator rata-rata atau indikator fluktuasi untuk membantu.

-

Jika posisi di posisi terbawah terbalik, maka ada risiko untuk terbalik lagi. Anda dapat mengatur stop loss dan mengoptimalkan manajemen posisi Anda.

-

Pengaturan parameter yang tidak tepat dapat menyebabkan risiko kebocoran atau kesalahan pembelian. Kombinasi parameter perlu dioptimalkan dengan pengujian berulang.

-

Kode yang lebih besar, dapat terus dimodulasi, mengurangi duplikasi kode.

Arah optimasi

-

Menambahkan modul stop loss dan mengoptimalkan strategi manajemen posisi.

-

Tambahkan indikator rata-rata atau indikator fluktuasi untuk konfirmasi tambahan.

-

Kode modular, mengurangi logika penghakiman berulang.

-

Terus mengoptimalkan parameter untuk meningkatkan stabilitas.

-

Untuk menguji lebih banyak varietas, gunakan Arbitrage.

Meringkaskan

Strategi perdagangan berorientasi dua dasar dengan menangkap karakteristik dua dasar indikator PPO, dikombinasikan dengan konfirmasi ganda yang ditentukan oleh posisi harga, untuk mencapai posisi yang efektif pada titik balik harga. Dibandingkan dengan penilaian indikator tunggal, strategi ini memiliki penilaian yang lebih akurat dan filter suara yang lebih baik. Namun, strategi ini juga memiliki beberapa sinyal risiko palsu, perlu terus mengoptimalkan portofolio indikator, dan didukung dengan strategi manajemen posisi yang ketat, Anda dapat memperoleh keuntungan yang stabil dalam kehidupan nyata.

- 1