Strategi Terobosan Momentum Dua MA

Gambaran Umum

Strategi Breakout Momentum MA Ganda adalah strategi trading kuantitatif yang menggabungkan dua moving average dan indikator RSI. Strategi ini menghitung moving average cepat, moving average lambat, dan indikator RSI, menetapkan threshold overbought/oversold pada indikator momentum RSI, melakukan long saat terjadi golden cross pada dua MA, dan short saat terjadi death cross, untuk menangkap pergerakan tren pasar.

Prinsip Strategi

Strategi Breakout Momentum MA Ganda terutama didasarkan pada dua moving average dan indikator RSI. Pertama, hitung dua moving average, satu cepat dan satu lambat: garis cepat adalah Weighted Moving Average 10 hari, garis lambat adalah Linear Adaptive Moving Average 100 hari. Kemudian hitung indikator RSI 14 hari dan tetapkan threshold overbought/oversold. Ketika garis cepat melintasi di atas garis lambat, dianggap sebagai kondisi bullish, sedangkan ketika garis cepat melintasi di bawah garis lambat, dianggap sebagai kondisi bearish. Saat menentukan kondisi bullish/bearish, diperlukan juga indikator RSI berada di atas garis overbought atau di bawah garis oversold, sehingga dapat menyaring sinyal palsu secara efektif.

Secara spesifik, ketika kondisi bullish terdeteksi, jika RSI saat itu berada di atas garis overbought, maka buka posisi long; ketika kondisi bearish terdeteksi, jika RSI berada di bawah garis oversold, maka buka posisi short. Setelah posisi dibuka, ketika sinyal trading berbalik, lakukan pembukaan posisi sebaliknya.

Keunggulan Strategi

Strategi Breakout Momentum MA Ganda menggabungkan indikator dua MA dan RSI, sehingga dapat mengidentifikasi tren pasar secara efektif, dan menggunakan RSI untuk menyaring sinyal palsu, meningkatkan keandalan sinyal trading. Dibandingkan dengan sistem MA tunggal, strategi ini dapat secara signifikan mengurangi transaksi yang tidak efektif. Selain itu, optimasi parameter RSI juga memberikan fleksibilitas pada strategi.

Risiko Strategi

Strategi Breakout Momentum MA Ganda juga memiliki risiko tertentu. Sistem dua MA sangat sensitif terhadap parameter, sehingga perlu menguji kombinasi parameter secara hati-hati untuk pasar yang berbeda. Selain itu, jika threshold yang ditetapkan pada indikator RSI tidak tepat, dapat menyebabkan hilangnya peluang trading. Terakhir, stop loss trailing yang agresif dapat ditembus dalam kondisi pasar tertentu, sehingga perlu menyesuaikan titik stop loss berdasarkan hasil backtest.

Optimasi Strategi

Strategi Breakout Momentum MA Ganda dapat dioptimalkan dari beberapa aspek berikut:

- Mengoptimalkan parameter MA cepat dan lambat untuk menemukan kombinasi parameter terbaik;

- Mengoptimalkan parameter RSI, menyesuaikan threshold overbought/oversold;

- Menambahkan mekanisme stop loss trailing adaptif untuk mengendalikan risiko;

- Menambahkan modul optimasi ukuran posisi untuk meningkatkan efisiensi penggunaan modal.

Kesimpulan

Strategi Breakout Momentum MA Ganda menggunakan sistem dua MA untuk menentukan arah tren, dan memanfaatkan indikator RSI untuk menyaring sinyal, sehingga secara efektif memperbaiki kekurangan sistem MA tunggal. Strategi ini memiliki ruang optimasi parameter yang besar dan dapat diadaptasi secara otomatis, menjadikannya strategi pengikut tren yang unggul.

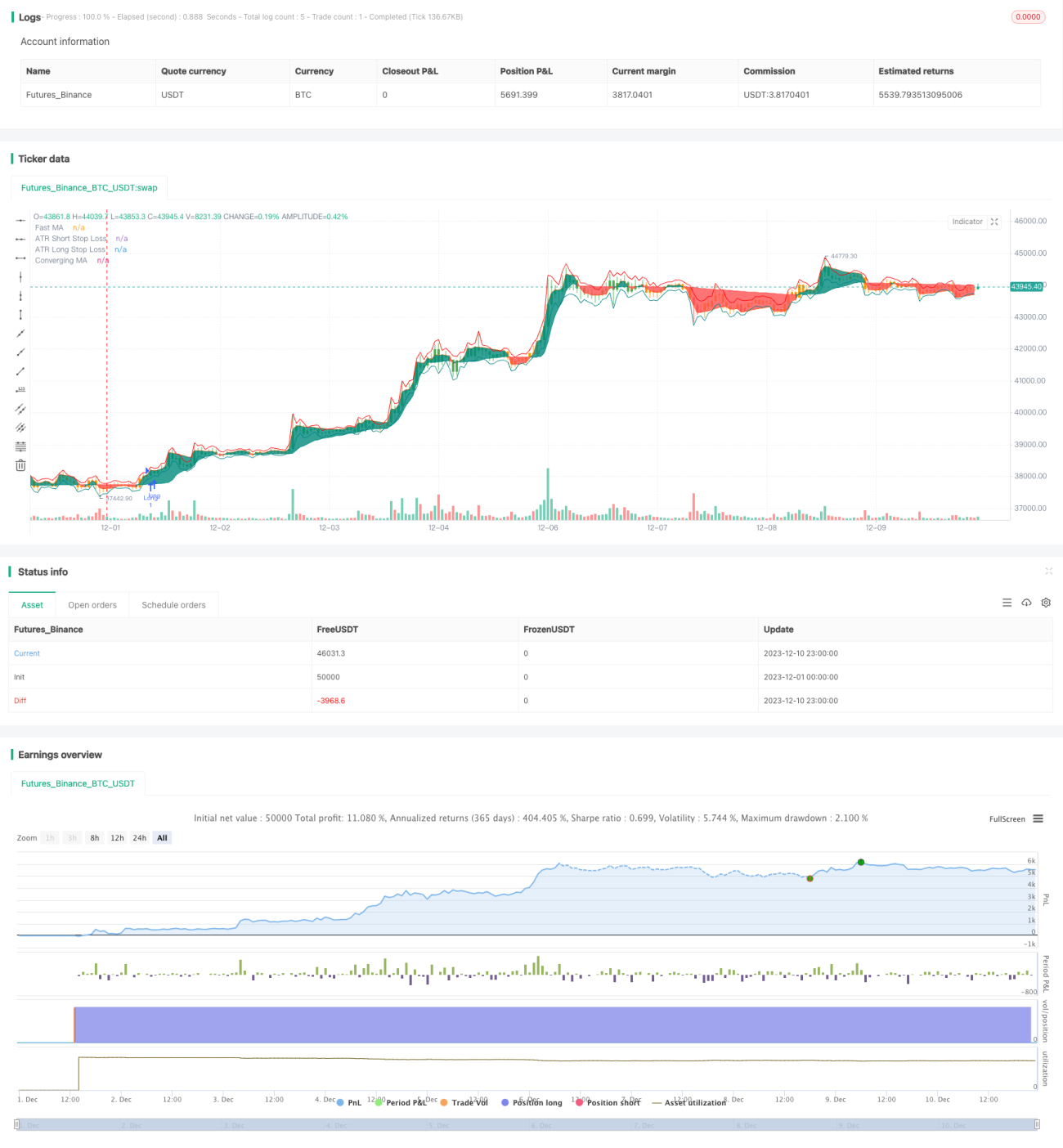

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-10 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © Salman4sgd

//@version=5- 1