Strategi Stop Loss Pelacakan Tren RSI

Gambaran Umum

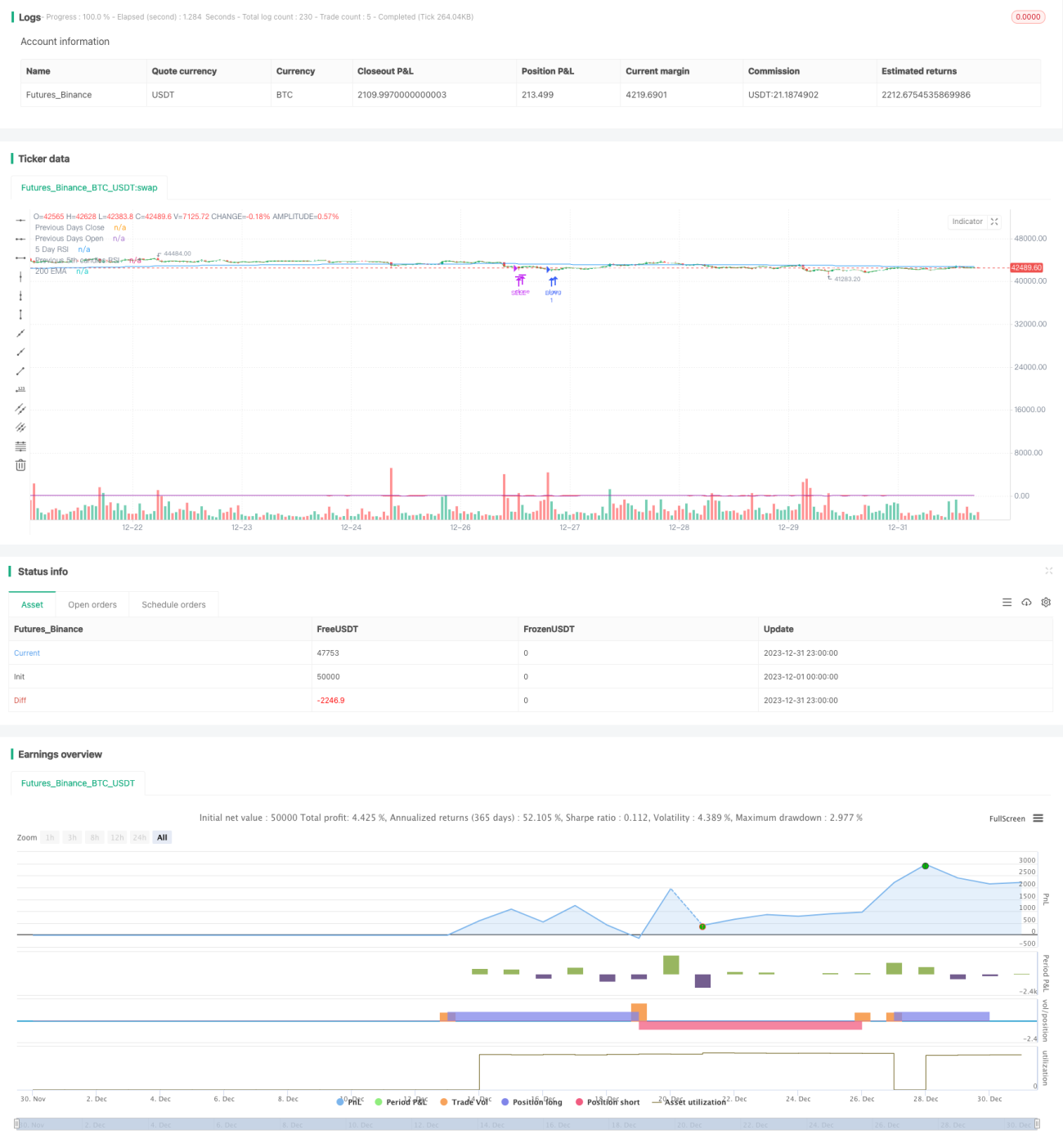

Ini adalah strategi trading kuantitatif yang menggunakan indikator RSI untuk menentukan tren dan menetapkan stop loss serta take profit. Strategi ini menggabungkan indikator RSI untuk mengidentifikasi arah tren pasar, serta menetapkan stop loss dan take profit dinamis untuk mengunci keuntungan dan meminimalkan risiko.

Prinsip Strategi

Strategi ini terutama menggunakan indikator RSI untuk menentukan arah tren pasar dan memutuskan posisi beli atau jual. Ketika indikator RSI menembus ke atas garis rendah, pasar dianggap sedang dalam tren naik, dan posisi beli (long) diambil. Ketika indikator RSI menembus ke bawah garis tinggi, pasar dianggap sedang dalam tren turun, dan posisi jual (short) diambil.

Pada saat yang sama, strategi ini melacak harga pembukaan setiap posisi dan menetapkan stop loss serta take profit yang mengambang. Untuk posisi beli, ditetapkan persentase tertentu dari harga pembukaan sebagai garis stop loss, sedangkan untuk posisi jual, ditetapkan persentase tertentu dari harga pembukaan sebagai garis take profit. Ketika harga menyentuh garis stop loss atau take profit, strategi secara otomatis menutup posisi untuk menghentikan kerugian atau mengunci keuntungan.

Keunggulan Strategi

- Menggunakan indikator RSI untuk menentukan arah tren pasar, menghindari trading di zona konsolidasi;

- Menetapkan stop loss dan take profit dinamis yang dapat mengunci keuntungan secara fleksibel dan mengelola risiko secara efektif;

- Parameter RSI dan rasio stop loss/take profit dapat disesuaikan melalui input eksternal untuk optimasi.

Risiko Strategi

- Indikator RSI memiliki keterlambatan tertentu, sehingga mungkin melewatkan titik perubahan tren jangka pendek;

- Garis stop loss dan take profit yang terlalu dekat dapat mengakibatkan posisi tertutup akibat breakout.

Arah Optimasi

- Dapat diuji efektivitas indikator RSI pada periode yang berbeda;

- Dapat diuji berbagai kombinasi parameter untuk menemukan rasio stop loss dan take profit yang optimal;

- Dapat ditambahkan indikator tambahan untuk menyaring sinyal.

Kesimpulan

Secara keseluruhan, strategi ini adalah strategi trading kuantitatif yang menggunakan indikator RSI untuk melacak tren, dilengkapi dengan stop loss dan take profit dinamis. Dibandingkan dengan strategi yang hanya mengandalkan satu indikator, strategi ini lebih baik dalam mengelola risiko dan dapat mengunci keuntungan secara efektif. Dengan optimasi parameter dan penambahan indikator bantu, kinerja strategi dapat ditingkatkan lebih lanjut.

- 1