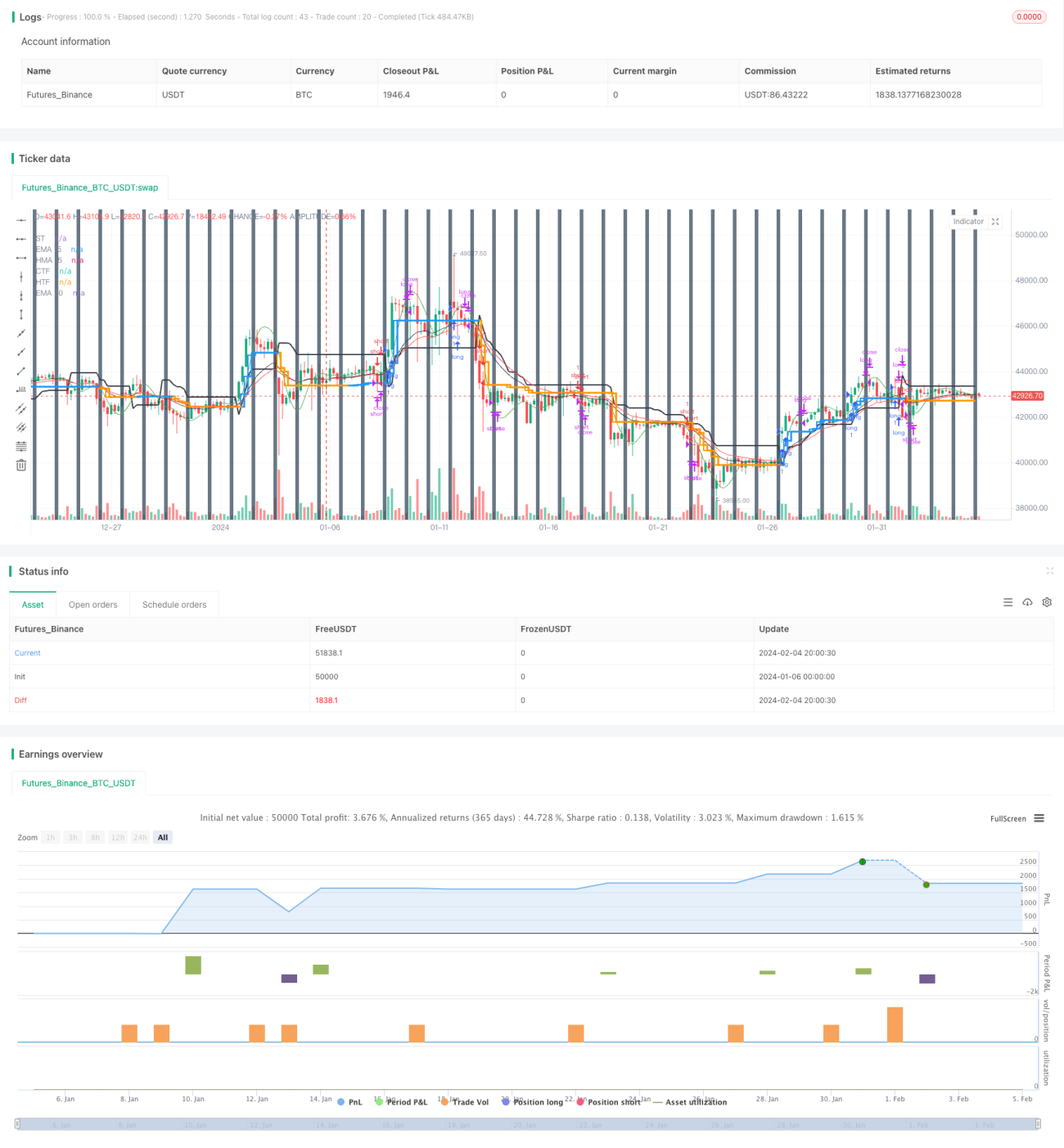

Strategi trailing stop berdasarkan Super Trend Heikin Ashi

Ringkasan Strategi

Strategi ini adalah strategi trailing stop yang menggabungkan lilin Heikin Ashi dan indikator Super Trend. Strategi ini menggunakan lilin Heikin Ashi untuk menyaring kebisingan pasar, indikator Super Trend untuk menentukan arah tren, dan Super Trend sebagai garis stop loss dinamis untuk mencapai trailing stop dan manajemen risiko yang efisien.

Prinsip Strategi

- Menghitung lilin Heikin Ashi: termasuk harga pembukaan, penutupan, tertinggi, dan terendah.

- Menghitung indikator Super Trend: menghitung pita atas dan bawah berdasarkan ATR dan harga.

- Menggabungkan lilin Heikin Ashi dan Super Trend untuk menentukan arah tren.

- Ketika harga penutupan Heikin Ashi lebih dekat ke pita atas Super Trend dibandingkan harga penutupan lilin sebelumnya, itu adalah tren bullish; ketika harga penutupan Heikin Ashi lebih dekat ke pita bawah Super Trend dibandingkan harga penutupan lilin sebelumnya, itu adalah tren bearish.

- Dalam tren bullish, gunakan pita atas Super Trend sebagai garis trailing stop; dalam tren bearish, gunakan pita bawah Super Trend sebagai garis trailing stop.

Keunggulan Strategi

- Menggunakan Heikin Ashi untuk menyaring sinyal palsu, sehingga sinyal tren lebih andal.

- Super Trend sebagai stop loss dinamis memaksimalkan penguncian keuntungan tren dan menghindari penarikan yang terlalu besar.

- Menggabungkan berbagai periode waktu untuk menentukan bullish/bearish, sehingga sinyal level tinggi/rendah lebih andal.

- Fungsi tutup posisi terjadwal menghindari dampak pergerakan irasional pada waktu tertentu.

Risiko Strategi

- Mudah terkena stop loss saat terjadi pembalikan tren. Risiko ini dapat dikurangi dengan memperlonggar garis stop loss secara wajar.

- Pengaturan parameter Super Trend yang tidak tepat dapat menyebabkan stop loss terlalu lebar atau terlalu sempit. Berbagai kombinasi parameter dapat diuji.

- Tidak mempertimbangkan manajemen modal. Harus menetapkan kontrol posisi.

- Tidak mempertimbangkan biaya transaksi. Dampak biaya harus diperhitungkan.

Arah Optimasi Strategi

- Mengoptimalkan kombinasi parameter Super Trend untuk menemukan parameter optimal.

- Menambahkan fungsi kontrol posisi.

- Menambahkan pertimbangan biaya, seperti komisi, slippage, dll.

- Dapat menyesuaikan lebar stop loss secara fleksibel berdasarkan kekuatan tren.

- Pertimbangkan untuk menggabungkan indikator lain untuk memfilter sinyal masuk.

Kesimpulan

Strategi ini mengintegrasikan keunggulan Heikin Ashi dan Super Trend, mampu menangkap arah tren, sekaligus menggunakan Super Trend untuk mencapai trailing stop dinamis otomatis, sehingga mengunci keuntungan tren. Risiko utama strategi berasal dari pembalikan tren dan optimasi parameter, keduanya dapat diperbaiki melalui optimasi lebih lanjut. Secara keseluruhan, strategi ini meningkatkan stabilitas sistem perdagangan dan potensi keuntungan melalui integrasi indikator.

- 1