Strategi Ichimoku Cloud Nine untuk Trading

Ikhtisar

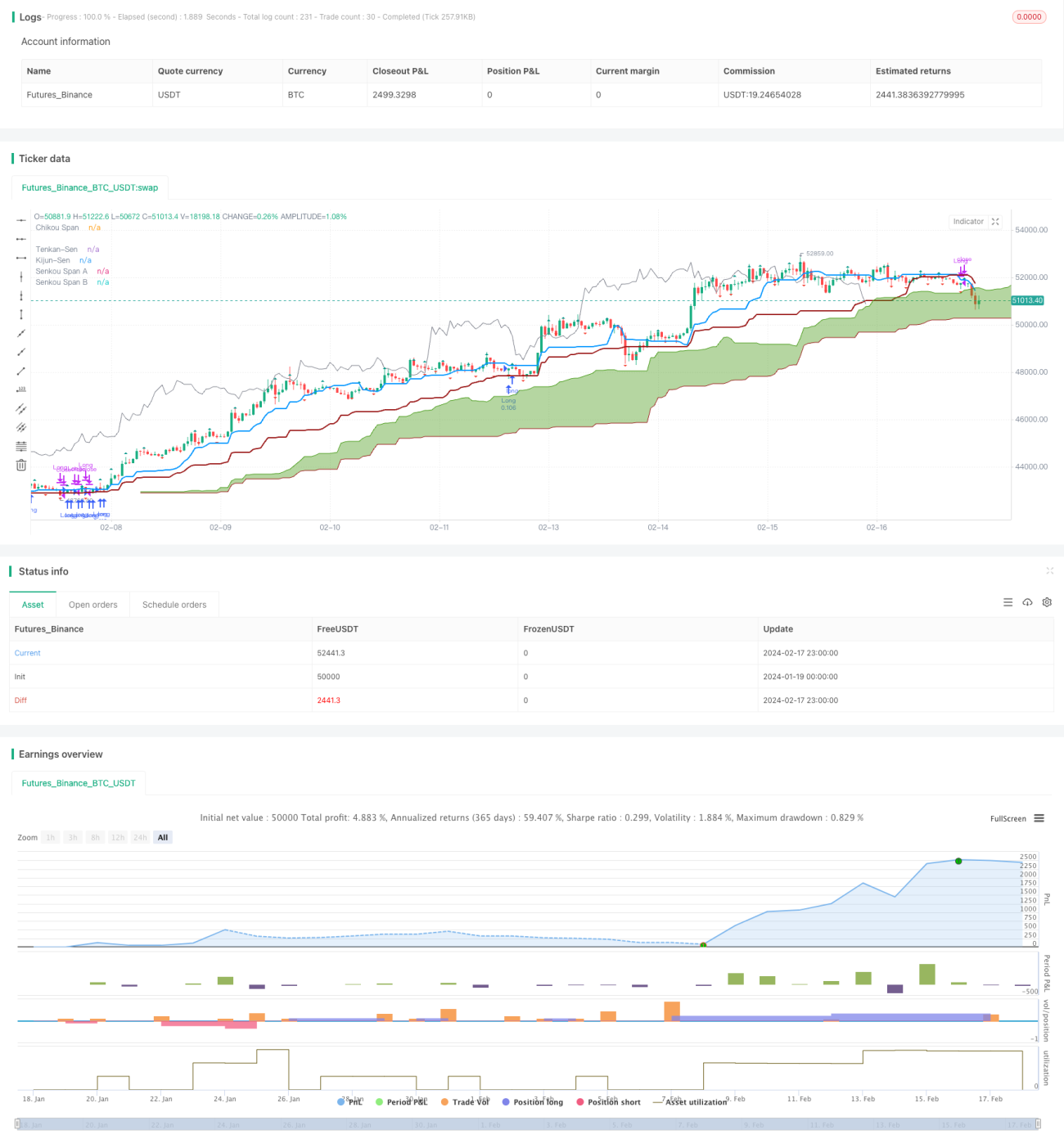

Strategi Ichimoku Cloud Nine adalah strategi trading yang didasarkan pada indikator Ichimoku Cloud yang dikombinasikan dengan Williams Fractal. Strategi ini memanfaatkan beberapa sinyal trading yang disediakan oleh indikator Ichimoku Cloud untuk menghasilkan sinyal trading. Ini adalah strategi yang ditujukan untuk trading praktis.

Prinsip Strategi

Strategi ini terutama didasarkan pada beberapa sinyal Ichimoku berikut untuk masuk posisi:

- Penembusan Awan: Sinyal muncul ketika harga penutupan menembus batas atas atau bawah awan.

- Persilangan TK: Sinyal muncul ketika garis Tenkan berpotongan dengan garis Kijun.

- Pembalikan Awan: Sinyal muncul ketika garis Senkou Span A berpotongan dengan garis Senkou Span B.

- Persilangan Tepi: Sinyal muncul ketika harga bergerak dari satu sisi awan ke sisi awan lainnya.

Selain itu, strategi ini juga akan menutup posisi dalam kondisi berikut:

- Menutup posisi ketika harga penutupan memasuki awan.

- Menutup posisi ketika terjadi persilangan TK secara terbalik.

- Menutup sebagian posisi ketika Williams Fractal ditembus.

Strategi ini menggabungkan beberapa sinyal trading dari Ichimoku Cloud, yang bertujuan untuk meningkatkan keandalan sinyal trading sambil menggunakan fractal untuk menetapkan stop loss dan mengendalikan risiko.

Keunggulan Strategi

Dibandingkan dengan strategi sinyal tunggal, strategi ini secara komprehensif memanfaatkan beberapa sinyal dari Ichimoku Cloud, sehingga dapat menyaring beberapa sinyal yang tidak tepat dan meningkatkan akurasi sinyal. Selain itu, parameter strategi dapat dikonfigurasi secara fleksibel, sehingga cocok untuk berbagai instrumen dan optimasi parameter.

Selain itu, strategi ini memperkenalkan penembusan Williams Fractal untuk menetapkan stop loss, sehingga dapat mengendalikan risiko secara lebih proaktif, mengunci keuntungan, dan menghindari kerugian besar.

Risiko Strategi

Strategi ini terutama menghadapi risiko berikut:

- Indikator Cloud memiliki keterlambatan (lagging), sehingga tidak dapat mencerminkan perubahan harga secara tepat waktu.

- Banyaknya sinyal mungkin terlalu konservatif, sehingga melewatkan beberapa peluang.

- Stop loss fractal mungkin tertembus, menyebabkan kerugian.

Untuk mengatasi masalah keterlambatan, parameter dapat disesuaikan atau beberapa sinyal penyaring dapat dinonaktifkan. Untuk mengatasi risiko stop loss fractal, periode waktu fractal dapat disesuaikan, atau hanya melakukan stop loss sebagian.

Arah Optimasi Strategi

Strategi ini terutama dapat dioptimalkan dari beberapa aspek berikut:

- Menyesuaikan parameter Ichimoku untuk beradaptasi dengan periode waktu dan instrumen yang berbeda.

- Menyesuaikan atau menonaktifkan beberapa sinyal penyaring, mempertahankan sinyal inti.

- Menyesuaikan parameter fractal, menggunakan fractal dengan periode waktu yang lebih besar, atau hanya menggunakan stop loss sebagian.

- Menambahkan filter indikator lain, seperti indikator volume, dll.

Kesimpulan

Strategi Ichimoku Cloud Nine mengintegrasikan beberapa sinyal trading dari Ichimoku Cloud, sehingga memanfaatkan keunggulan indikator Cloud sekaligus meningkatkan akurasi dan tingkat keberhasilan sinyal. Strategi ini juga menggunakan fractal sebagai metode stop loss untuk mengendalikan risiko. Strategi ini dapat dioptimalkan melalui parameter dan sinyal, sehingga cocok untuk trading algoritmik pada berbagai instrumen.

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Cloud Nine", shorttitle="Ichimoku Cloud Nine", overlay=true, calc_on_every_tick = true, calc_on_order_fills = false, initial_capital = 5000, currency = "USD", default_qty_type = "percent_of_equity", default_qty_value = 10, pyramiding = 3, process_orders_on_close = true)

color green = #459915- 1