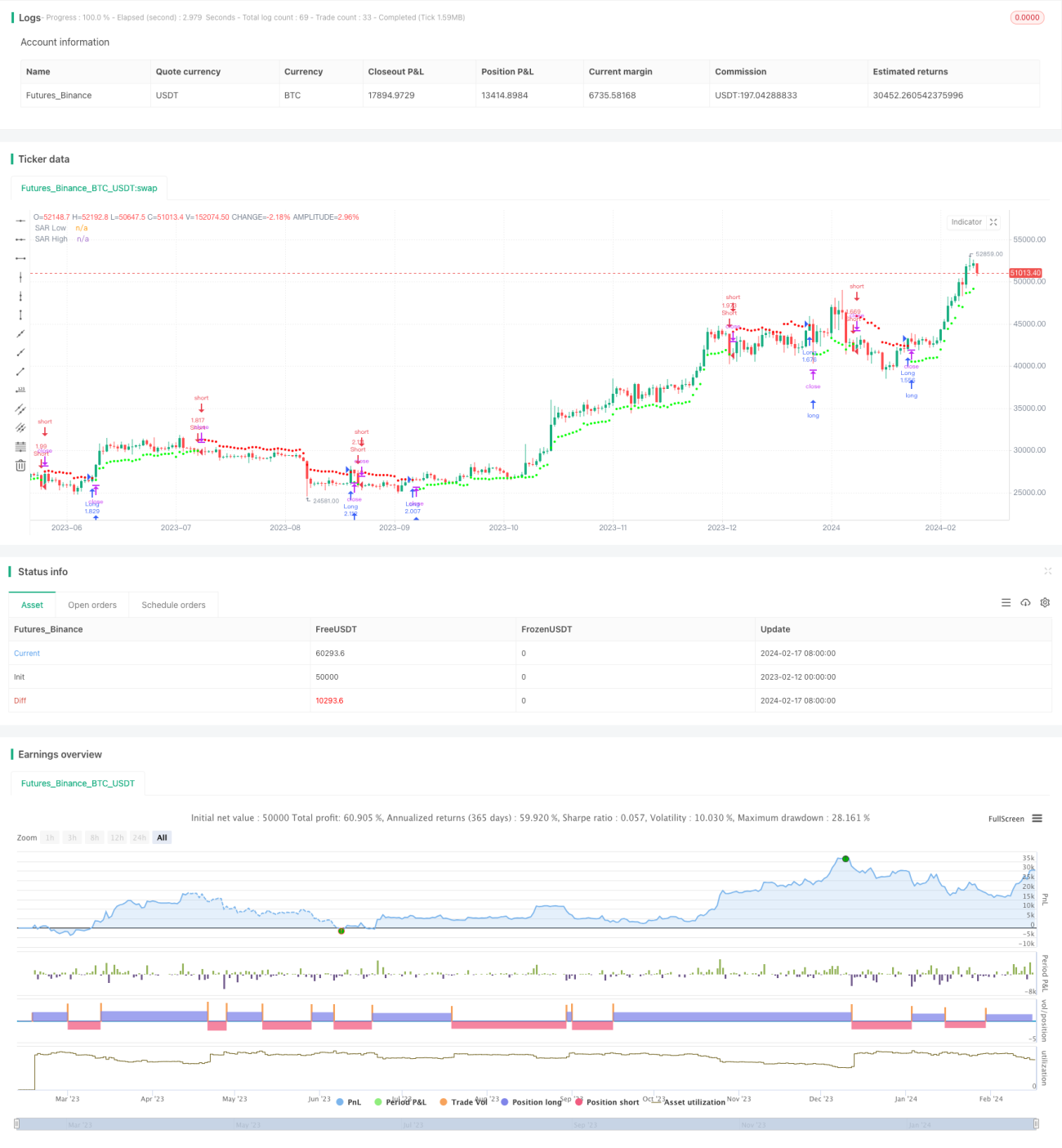

Strategi Trading Reversal Breakout Kanal

Ringkasan

Strategi perdagangan reversal dengan break-out saluran adalah strategi perdagangan reversal yang melacak titik take-profit dan stop-loss bergerak pada saluran harga. Strategi ini menggunakan metode rata-rata bergerak tertimbang untuk menghitung saluran harga, dan membuka posisi long atau short ketika harga menembus saluran.

Prinsip Strategi

Strategi ini pertama-tama menghitung volatilitas harga menggunakan indikator Wilder Average True Range (ATR). Kemudian, berdasarkan nilai ATR, dihitung konstanta rentang rata-rata (ARC). ARC adalah setengah lebar saluran harga. Selanjutnya, dihitung batas atas dan bawah saluran, yaitu titik take-profit dan stop-loss, yang disebut titik SAR. Ketika harga menembus batas atas, lakukan short; ketika menembus batas bawah, lakukan long.

Secara spesifik, pertama-tama hitung ATR dari N candle terbaru. Kemudian, ARC diperoleh dengan mengalikan ATR dengan suatu koefisien. ARC yang dikalikan dengan koefisien dapat mengontrol lebar saluran. ARC ditambahkan ke titik tertinggi harga penutupan dari N candle untuk mendapatkan batas atas saluran, yaitu SAR tinggi. ARC dikurangkan dari titik terendah harga penutupan untuk mendapatkan batas bawah saluran, yaitu SAR rendah. Jika harga penutupan menembus batas atas, lakukan short; jika harga penutupan menembus batas bawah, lakukan long.

Keunggulan Strategi

- Menggunakan volatilitas harga untuk menghitung saluran adaptif yang dapat melacak perubahan pasar

- Perdagangan reversal, cocok untuk pasar dengan pembalikan tren

- Take-profit dan stop-loss bergerak, dapat mengunci keuntungan dan mengontrol risiko

Risiko Strategi

- Perdagangan reversal rentan terjebak, perlu menyesuaikan parameter dengan tepat

- Dalam pasar dengan fluktuasi besar, posisi mudah ditutup

- Parameter yang tidak tepat dapat menyebabkan perdagangan terlalu sering

Solusi:

- Optimalkan periode ATR dan koefisien ARC agar lebar saluran wajar

- Gabungkan indikator tren untuk menyaring waktu masuk

- Perbesar periode ATR untuk mengurangi frekuensi perdagangan

Arah Optimasi Strategi

- Optimalkan periode ATR dan koefisien ARC

- Tambahkan kondisi pembukaan posisi, misalnya dengan indikator MACD

- Tambahkan strategi stop-loss

Kesimpulan

Strategi perdagangan reversal dengan break-out saluran menggunakan saluran untuk melacak perubahan harga, membuka posisi reversal saat volatilitas meningkat, dan menetapkan take-profit dan stop-loss bergerak adaptif. Strategi ini cocok untuk pasar konsolidasi yang didominasi pembalikan, dan dapat memberikan imbal hasil investasi yang cukup baik jika titik pembalikan diprediksi dengan akurat. Namun, perlu diperhatikan untuk menghindari stop-loss yang terlalu longgar dan masalah optimasi parameter.

- 1