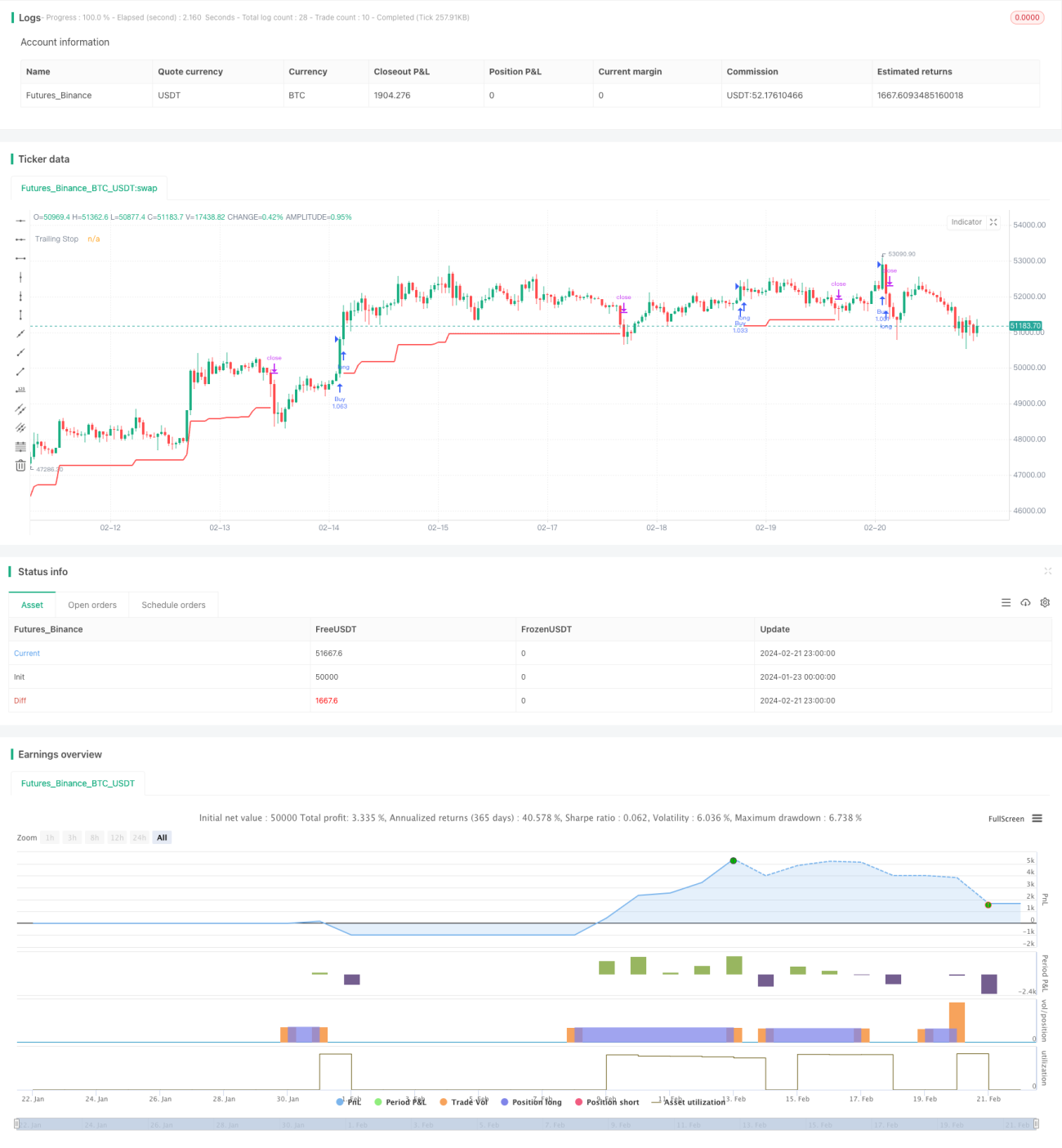

Berdasarkan strategi momentum breakout

Ikhtisar

Strategi Momentum Breakout adalah strategi tren yang melacak momentum pasar. Strategi ini menggabungkan berbagai indikator untuk menentukan apakah pasar saat ini berada dalam tren naik atau turun, dan membuka posisi beli saat menembus level resistensi kunci, serta membuka posisi jual saat menembus level support kunci.

Prinsip Strategi

Strategi ini terutama menggunakan saluran Donchian dengan berbagai periode untuk menentukan tren pasar dan level harga kunci. Secara spesifik, ketika harga menembus batas atas saluran Donchian periode panjang, misalnya 40 hari, strategi menganggapnya sebagai tren naik, dan berdasarkan hal tersebut, ditambah dengan filter seperti harga tertinggi tahun ini dan pengaturan arah rata-rata bergerak, menghasilkan sinyal beli. Sebaliknya, ketika harga menembus batas bawah saluran Donchian periode panjang, strategi menganggapnya sebagai tren turun, dan dengan filter seperti harga terendah tahun ini, menghasilkan sinyal jual.

Dalam hal keluar dari posisi, strategi ini menyediakan dua pilihan: batas stop-loss tetap dan trailing stop. Batas stop-loss tetap ditentukan berdasarkan saluran Donchian periode lebih pendek, misalnya 20 hari. Trailing stop menghitung garis stop-loss bergerak setiap hari berdasarkan nilai ATR. Kedua metode stop-loss ini dapat mengendalikan risiko dengan baik.

Analisis Keunggulan

Strategi ini menggabungkan penilaian tren dan operasi breakout, sehingga efektif menangkap peluang arah jangka pendek hingga menengah di pasar. Dibandingkan dengan indikator tunggal, strategi ini menggunakan berbagai filter untuk menyaring sebagian sinyal palsu, sehingga meningkatkan kualitas sinyal masuk. Selain itu, penerapan strategi stop-loss membuatnya memiliki ketahanan yang baik, bahkan jika terjadi koreksi jangka pendek, kerugian dapat dikendalikan secara efektif.

Analisis Risiko

Risiko utama strategi ini adalah fluktuasi pasar yang tajam dapat memicu stop-loss sehingga posisi keluar. Jika pasar kemudian berbalik arah dengan cepat, hal ini dapat menyebabkan kehilangan peluang. Selain itu, penggunaan berbagai filter juga dapat menyaring sebagian peluang, sehingga mengurangi frekuensi posisi strategi.

Untuk mengurangi risiko, nilai ATR dapat disesuaikan atau jarak saluran Donchian diperlebar, sehingga kemungkinan stop-loss tertembus berkurang. Filter juga dapat dikurangi atau dihapus untuk meningkatkan frekuensi masuk, namun risikonya juga akan meningkat.

Arah Optimasi

Strategi ini dapat dioptimasi dari beberapa aspek berikut:

- Mengoptimasi panjang saluran Donchian untuk menemukan kombinasi parameter terbaik.

- Mencoba berbagai jenis rata-rata bergerak sebagai indikator filter.

- Menyesuaikan pengali ATR atau mengganti dengan stop-loss titik tetap.

- Menambahkan lebih banyak indikator tren, seperti MACD.

- Mengoptimasi jendela periode harga tertinggi/terendah tahun ini, dll.

Dengan menguji berbagai parameter, dapat ditemukan kombinasi parameter optimal yang menyeimbangkan risiko dan keuntungan.

Kesimpulan

Strategi ini menggabungkan berbagai indikator untuk menentukan arah tren, dan memberikan sinyal perdagangan saat terjadi breakout di titik kunci. Mekanisme stop-lossnya juga memberikan kemampuan pengendalian risiko yang kuat. Dengan mengoptimasi pengaturan parameter, strategi ini dapat menghasilkan keuntungan berlebih yang stabil. Strategi ini cocok untuk investor yang tidak memiliki penilaian jelas tentang pasar namun ingin mengikuti tren.

/*backtest

start: 2024-01-23 00:00:00

end: 2024-02-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HeWhoMustNotBeNamed

//@version=4- 1