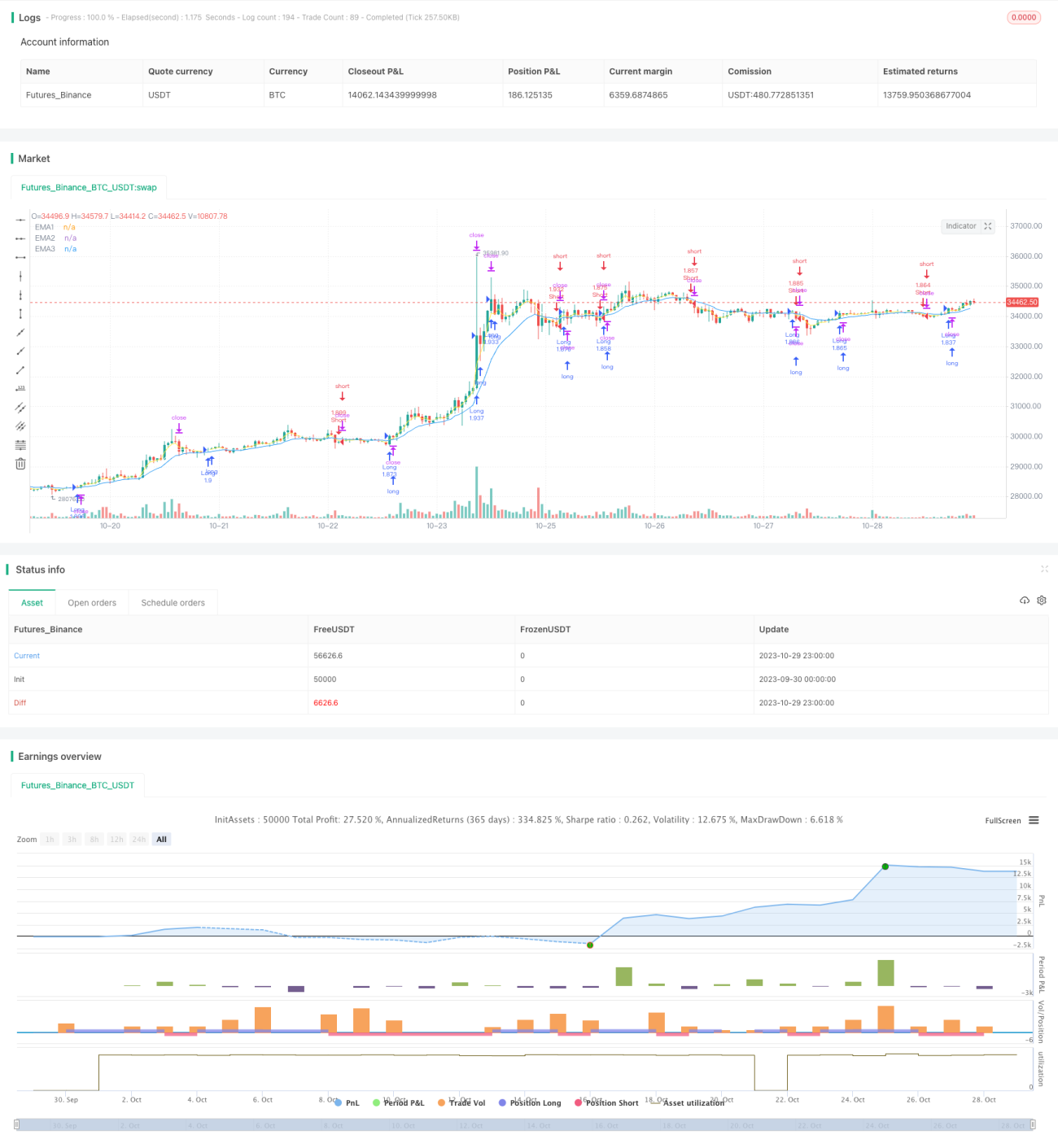

概要

移動平均線ポリゴン戦略は、複数の異なる期間の移動平均線を用いてポリゴンを構築し、そのポリゴンのブレイクアウトを取引シグナルとするトレンドフォロー戦略です。この戦略は複数の時間枠を総合的に考慮することで、市場ノイズを効果的にフィルタリングし、主要なトレンドを捉えることができます。

戦略の原理

この戦略では、3期間、7期間、13期間のEMAなど、異なる期間のEMAを入力し、それらを価格チャート上に描画してポリゴンチャネルを形成します。価格が複数のEMAラインを上抜けたときにロングシグナルを生成し、下抜けたときにショートシグナルを生成します。これにより、多くの偽のブレイクアウトを排除できます。

コードでは、close > ema1 and ema1 > ema2 and ema2 > ema3 によって上抜けシグナルを、close < ema1 and ema1 < ema2 and ema2 < ema3 によって下抜けシグナルを判定します。売買条件に時間条件(time_cond)を設定し、バックテストの範囲を制限します。買い・売りの執行時には移動ストップロスを使用して利益を保護します。

戦略のメリット

この戦略の最大のメリットは、主要なトレンド方向を効果的に捉えられる点です。複数の移動平均線によるフィルタリング機構により、市場の短期的ノイズに影響されにくく、誤ったシグナルを低減できます。移動ストップロスにより、適時に損切りして利益を確保できます。

リスクとその対処法

この戦略の主なリスクは、トレンドの転換点を特定できないことです。トレンドが反転したときに逆張りとなり損失が発生する可能性があります。また、移動平均線の組み合わせが適切でない場合、取引頻度が高すぎたりシグナルが遅れたりする可能性があります。移動平均線のパラメータ組み合わせを最適化したり、RSIやMACDなどの逆転サインを判断する他の指標を追加したり、ストップロスの幅を調整したりすることでリスクを低減できます。

最適化の方向性

この戦略は以下の点で最適化が可能です。

- 移動平均線の期間パラメータを最適化し、最適なパラメータ組み合わせを見つける

- トレンド転換点にRSIやMACDなどの逆転シグナル指標を追加し、適時に損切りして撤退する

- 移動ストップロスのストップ幅とオフセット値を最適化し、ストップロスが発動する確率を下げる

- 銘柄ごとにパラメータを最適化し、戦略の適応性を高める

まとめ

移動平均線ポリゴン戦略は、総じて信頼性が高く効果的なトレンドフォロー戦略です。最大の利点は、主要なトレンド方向を捉えながらノイズを大幅にフィルタリングできることです。ただし、逆転の認識が不十分な面もあります。パラメータ最適化や補助指標の追加などにより、戦略のパフォーマンスを向上させることができます。この戦略はトレンドが明確な銘柄に適しており、適切に使用すれば安定した取引収益を得ることができます。

- 1