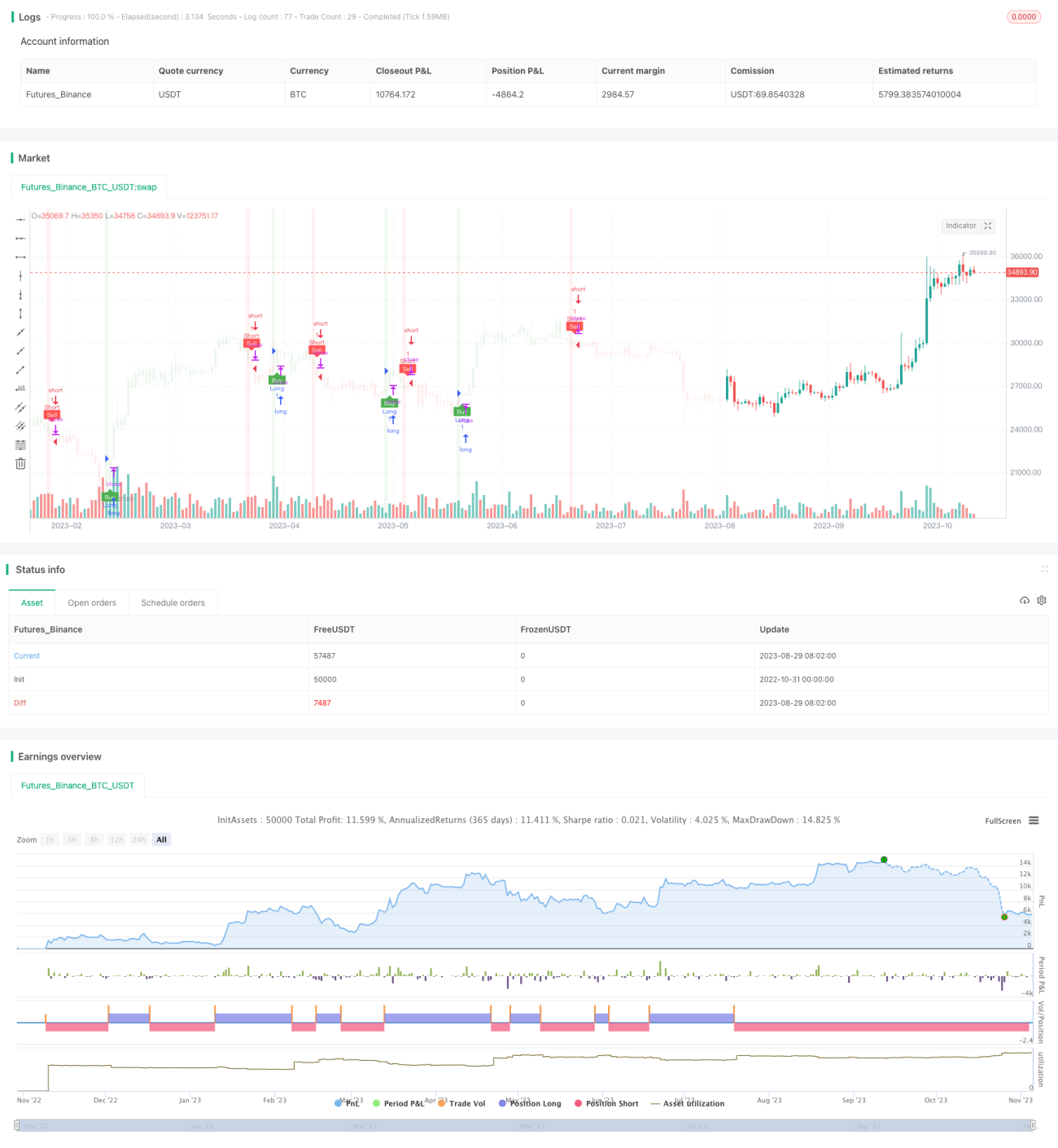

T3移動平均線とATRに基づく取引戦略

概要

本戦略は、T3移動平均線、ATRインジケーター、およびヘイキンアシの組み合わせを利用して、買いシグナルと売りシグナルを識別し、ATRに基づいてストップロスと利確の位置を計算し、トレンドフォロー取引を実現します。戦略の利点は、反応が速く、取引リスクをコントロールできることです。

原理分析

指標計算

-

T3移動平均線: 平滑化されたパラメータT3(デフォルト100)のT3移動平均線を計算し、トレンドの方向性を判断します。

-

ATR: ATR(平均真実レンジ)を計算し、ストップロス・利確の位置の大きさを決定します。

-

ATR移動ストップロス: ATRに基づいて移動ストップロスラインを計算し、価格変動とボラティリティに応じて調整することで、トレンドフォローを実現します。

取引ロジック

-

買いシグナル: 終値がATR移動ストップロスラインを上抜け、かつT3平均線を下回っている場合に買いシグナルが発生します。

-

売りシグナル: 終値がATR移動ストップロスラインを下抜け、かつT3平均線を上回っている場合に売りシグナルが発生します。

-

ストップロス・利確: エントリー後、ATR値とユーザー設定のリスクリワード比率に基づいて、ストップロスと利確の価格を計算します。

戦略のエントリーとエグジット

-

買いエントリー後、ストップロス価格はエントリー価格からATR値を差し引いた価格、利確価格はエントリー価格にATR値×リスクリワード比率を加えた価格となります。

-

売りエントリー後、ストップロス価格はエントリー価格にATR値を加えた価格、利確価格はエントリー価格からATR値×リスクリワード比率を差し引いた価格となります。

-

価格がストップロスまたは利確の水準に達した場合、ポジションを決済します。

優位性分析

反応が速い

T3平均線のパラメータはデフォルトで100であり、一般的な移動平均線よりも感度が高く、価格変動に素早く反応できます。

リスクコントロール

ATRを使用して計算された移動ストップロスは、市場のボラティリティに応じて価格をトレイルし、ストップロスが突破されるリスクを回避します。利確・ストップロスの位置はATRに基づいているため、各取引のリスクリワード比をコントロールできます。

トレンドフォロー

ATR移動ストップロスラインはトレンドを追跡できるため、短期的な価格の調整が発生しても、決済をトリガーされにくく、誤ったシグナルを減らします。

パラメータ最適化の余地

T3平均線の期間とATRの期間は最適化可能であり、異なる市場に合わせてパラメータを調整することで、戦略の安定性を向上させることができます。

リスク分析

突破リスク

急激な相場変動が発生した場合、価格がストップロスラインを直接突破し、損失が発生する可能性があります。ATR期間やストップロスの距離を適宜拡大することで緩和できます。

トレンド反転リスク

トレンド反転時に価格が移動ストップロスラインをクロスすると、損失が生じる可能性があります。他の指標を組み合わせてトレンドを判断し、反転ポイント付近での取引を避けることができます。

パラメータ最適化リスク

パラメータ最適化には十分な過去データが必要であり、過学習のリスクがあります。単一のデータセットに依存せず、複数の市場や時間枠を組み合わせた最適化を採用すべきです。

最適化の方向性

-

異なるT3移動平均線の期間パラメータをテストし、感度と安定性のバランスが取れた最適なパラメータの組み合わせを見つける。

-

ATRの期間パラメータをテストし、リスクコントロールとトレンドの捕捉の最適なバランスを見つける。

-

RSIやMACDなどの指標を組み合わせて、トレンド反転ポイントでの誤取引を回避する。

-

機械学習手法を用いて最適なパラメータを訓練し、人手による最適化の限界を低減する。

-

ポジション管理戦略を追加して、リスクをより適切にコントロールする。

まとめ

本戦略はT3移動平均線とATRインジケーターの利点を統合し、価格変動に素早く反応するとともに、リスクをコントロールします。パラメータの最適化や他の指標との組み合わせにより、さらに戦略の安定性と取引効率を向上させることができます。ただし、トレーダーは引き続き反転や突破のリスクに注意し、バックテスト結果に過度に依存しないようにする必要があります。

- 1