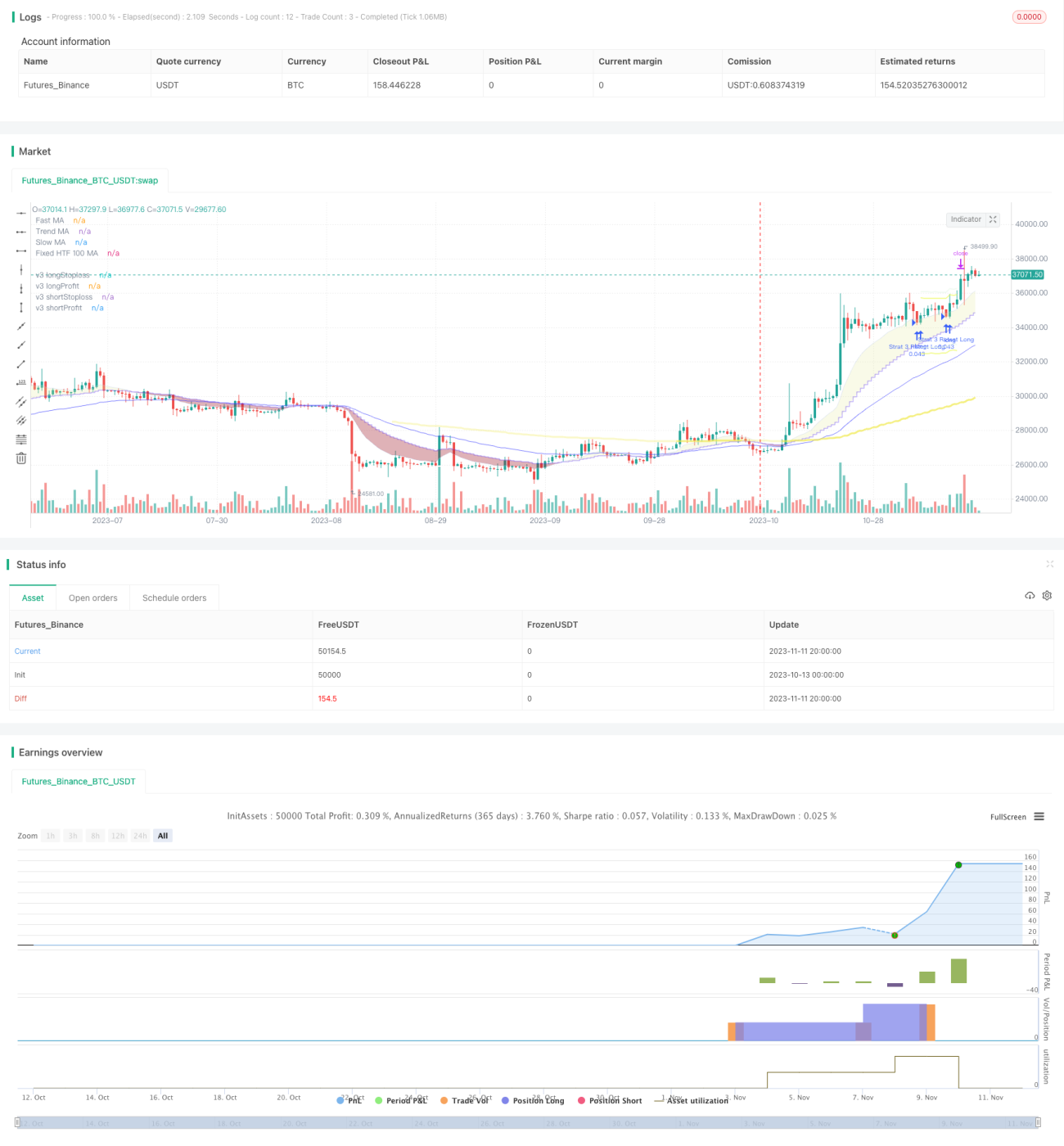

移動平均線クロスシステム取引戦略

概要

本戦略は移動平均線クロスシステムに基づく取引戦略です。異なる期間の移動平均線を計算し、それらのクロスを買い・売りシグナルとして設定します。同時にRSI指標を用いて取引シグナルをフィルタリングし、取引頻度を減らしながら利益率を向上させます。

戦略の原理

-

速い移動平均線、中程度の移動平均線、遅い移動平均線を計算します。速い移動平均線と中程度の移動平均線の間に取引チャネルを構成します。

-

価格が速い移動平均線を上抜けた時に買い、下抜けた時に売ります。

-

取引チャネルの方向判断:速い移動平均線 > 中程度の移動平均線 → 強気、速い移動平均線 < 中程度の移動平均線 → 弱気。チャネル方向が一致している時のみ取引します。

-

遅い移動平均線をトレンドフィルターとして使用:価格が遅い移動平均線より上にある場合のみ買い、逆の場合は売ります。

-

RSI指標の判断:RSIが設定した買いラインを超えたら買い、RSIが設定した売りラインを下回ったら売ります。

-

損切り・利確設定:ATRによる損切り、ATRによる利確を使用します。

優位性分析

-

複数の移動平均線の組み合わせにより、市場変化に柔軟に対応できます。

-

RSI指標により偽のブレイクアウトを回避し、シグナルの質を向上させます。

-

ATRによる動的損切り・利確により、ロスカットリスクを低減します。

-

遅い移動平均線+RSIの二重フィルターにより、不要な取引を回避します。

リスク分析

-

移動平均線クロスシグナルには遅延が生じる可能性があります。

-

二重フィルターにより一部の取引機会を逃す可能性があります。

-

ATRによる損切りが通常の損切り範囲を超える可能性があります。

-

パラメータ設定が不適切な場合、取引が過度に頻繁になったり、逆にまばらになったりする可能性があります。

これに対応するリスク管理措置:

-

移動平均線の期間を適切に短縮し、遅延の確率を低減します。

-

フィルターパラメータを適切に調整し、適度な取引頻度を維持します。

-

ATR倍率を調整し、損切りが許容範囲内に収まるようにします。

-

パラメータ設定を最適化し、最適なパラメータ組み合わせを見つけます。

最適化の方向性

-

異なる種類の移動平均線の組み合わせ効果をテストします。

-

異なる移動平均線期間パラメータの最適化をテストします。

-

RSIパラメータの最適化をテストします。

-

ATR損切り・利確係数の最適化。

-

フィルターパラメータの最適化により、最適なフィルター強度を探します。

まとめ

本戦略は移動平均線、RSI、ATRの3つの指標を総合的に活用し、パラメータの最適化により、様々な市場に適応可能な取引システムを構築できます。単一のテクニカル指標と比較して、偽のシグナルを効果的に減らし、利益を得る確率を高めることができます。ただし、いかなるテクニカル指標戦略も市場リスクを完全に回避することはできないため、厳格なリスク管理体制を確立することが不可欠です。

- 1