動的ボラティリティブレイクアウト戦略

概要

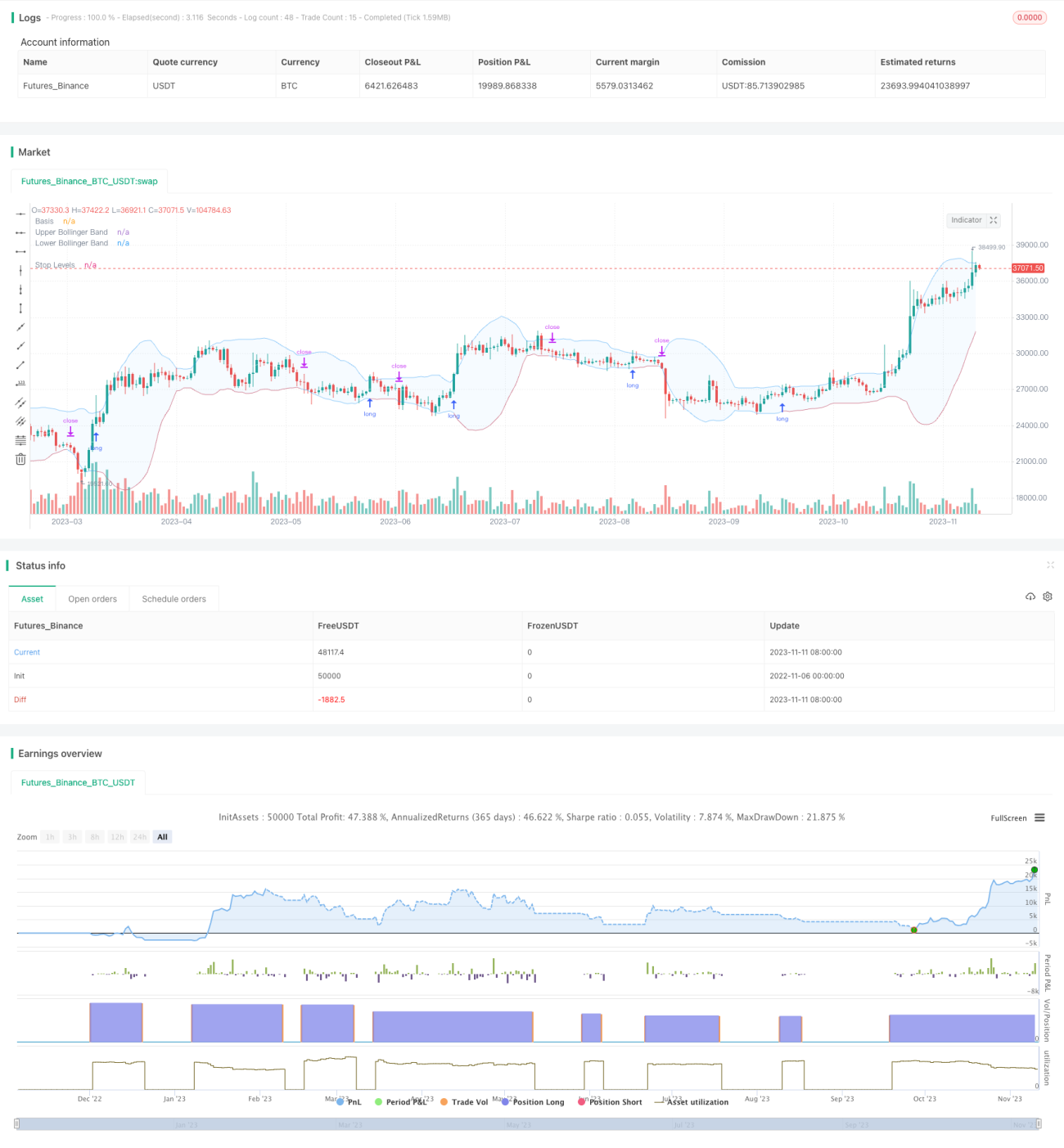

この戦略は、ボリンジャーバンドの動的な上限線と下限線を利用し、価格が上限線を突破したときに買い、下限線を割り込んだときにポジションを決済します。従来のブレイクアウト戦略とは異なり、ボリンジャーバンドの上下線は過去のボラティリティに応じて動的に変化するため、市場の買われ過ぎ・売られ過ぎの状態をより的確に判断できます。

戦略の原理

この戦略は主にボリンジャーバンドインジケーターを使用して価格のブレイクアウトを判断します。ボリンジャーバンドは以下の3本の線で構成されます。

- ミドルライン:n日移動平均線

- アッパーバンド:ミドルライン + k × n日標準偏差

- ロワーバンド:ミドルライン - k × n日標準偏差

価格がアッパーバンドを超えて上昇した場合、市場は買われ過ぎの状態と見なされ、買いポジションを取ります。価格がロワーバンドを下回った場合、市場は売られ過ぎの状態と見なされ、ポジションを決済します。

この戦略では、ボリンジャーバンドのパラメーター(ミドルラインの期間nと標準偏差の倍率k)をカスタマイズできます。デフォルトでは、ミドルラインは20日、標準偏差の倍率は2です。

株式は毎日終値後に、その日の終値がアッパーバンドを突破したかどうかをチェックします。突破した場合、翌日の寄り付きで買いシグナルを実行します。買いポジションを保有した後、リアルタイムで価格がロワーバンドを下回るかどうかを監視し、下回った場合に決済します。

また、この戦略には移動平均線フィルターが導入されており、価格が移動平均線より上にある場合のみ買いシグナルが生成されます。現在の周期またはより高い周期の移動平均線を描画することで、エントリータイミングを制御できます。

ストップロスの方法として、固定パーセンテージストップロスとボリンジャーバンドのロワーバンドに追従するストップロスの2つから選択できます。後者は利益を伸ばすためのより大きな余地を提供します。

戦略の利点

- ボリンジャーバンドを使用して市場の買われ過ぎ/売られ過ぎを判断

- 移動平均線フィルターにより逆張り取引を回避

- ボリンジャーバンドのパラメーターをカスタマイズ可能で、異なる期間に対応

- 2種類のストップロス方法から選択可能

- バックテストによるパラメーター最適化と、実運用での戦略検証をサポート

戦略のリスク

- ボリンジャーバンドだけでは買われ過ぎ/売られ過ぎを完全に判断できない

- 移動平均線フィルターにより、急激なブレイクアウトの機会を逃す可能性がある

- 固定ストップロスは保守的すぎる可能性があり、追従ストップロスは積極的すぎる可能性がある

- 異なる銘柄や期間に適応させるためにパラメーターの最適化が必要

- 損失額を制限できないため、資金管理を考慮する必要がある

戦略の最適化

- 異なる移動平均線パラメーターの組み合わせをテスト

- 異なるボリンジャーバンドパラメーターを試行

- 固定パーセンテージストップロスとロワーバンド追従ストップロスの収益率を比較

- 資金管理モジュールを追加し、1回の損失を制限

- 他のインジケーターと組み合わせてボリンジャーバンドのシグナルを検証

まとめ

この戦略は、ボリンジャーバンドの動的な上下線を利用して買われ過ぎ・売られ過ぎを判断し、移動平均線フィルターでシグナルを選別し、ストップロスで資金を保護します。従来の固定レンジブレイクアウト戦略と比較して、市場のボラティリティにより適応できます。パラメーターの最適化とリスク管理により、戦略の安定性と収益率をさらに向上させることができます。全体として、この戦略はボリンジャーバンドの動的特性を活用し、ブレイクアウト戦略の利点を獲得しており、実運用での検証と長期的な追跡最適化に値します。

- 1