ヒストグラムのブレイクアウトに基づく取引戦略

概要

本戦略は、ヒストグラムブレイクの原理と移動平均線のトレンド判断を組み合わせ、トレンド方向へのブレイクアウト取引を実現します。価格がヒストグラムの境界を突破した際に取引シグナルを生成します。同時に、短期と長期の移動平均線の位置関係を判断して全体のトレンド方向を特定し、レンジ相場での誤ったシグナルを回避します。

戦略の原理

-

短期移動平均線(20期間)と長期移動平均線(50期間)を計算します。

-

ローソク足から、上昇の長方形(close>open)または下降の長方形(close<open)が形成されたかを判定します。

-

長方形が前のローソク足の高値または安値を突破したかを判断します。上昇長方形で前のローソク足の高値を突破した場合はロングブレイクシグナル、下降長方形で前のローソク足の安値を突破した場合はショートブレイクシグナルとなります。

-

同時に、短期移動平均線が長期移動平均線より上にあるかどうかを判断します。上にある場合は上昇トレンド、下にある場合は下降トレンドと判定します。

-

短期・長期移動平均線が上昇トレンドと判断された場合のみロングブレイクシグナルが有効となり、下降トレンドと判断された場合のみショートブレイクシグナルが有効となります。これにより、レンジ相場での誤シグナルを回避します。

-

有効なロングブレイクシグナルが発生した場合、所定のストップロスとテイクプロフィット条件でロングポジションをオープンします。有効なショートブレイクシグナルが発生した場合、所定のストップロスとテイクプロフィット条件でショートポジションをオープンします。

-

短期移動平均線と長期移動平均線がクロスバック(再交差)した場合、現在のポジションを決済します。

優位性分析

-

ヒストグラムの境界を突破口として利用することで、強いブレイクシグナルを捉えます。

-

トレンド方向も同時に考慮することで、レンジ相場での誤シグナルを回避し、確度を高めます。

-

トレンドとブレイクの両方を考慮することで、トレンド相場で優れたパフォーマンスを発揮します。

-

パラメータ最適化により、異なる銘柄や時間足に適応できます。

リスクと対策

-

ブレイク失敗のリスク。対策として、より大きな突破口を選択し、ブレイクの勢いを確保します。

-

トレンド判断の不正確さのリスク。対策として、移動平均線パラメータを調整し、他の補助指標を追加してトレンドを判断します。

-

ストップロスが狭すぎて頻繁に損切りが発生するリスク。対策として、銘柄や時間足に応じてストップロス幅を動的に調整します。

-

利確幅が小さすぎるリスク。対策として、銘柄や時間足に応じてリスクリワード比率を動的に設定します。

最適化の方向性

-

全体的に、移動平均線パラメータ、突破口パラメータ、ストップロス幅、リスクリワード比率は、銘柄や時間足に応じてテスト・最適化し、戦略パラメータをカスタマイズする必要があります。

-

異なるタイプの移動平均線(EMA、SMAなど)をテストし、より適切な指標を探索することができます。

-

モメンタムなどの他の補助判断指標を追加して、トレンド判断の精度を向上させることができます。

-

機械学習などの手法を用いて、各種パラメータを動的に最適化することができます。

-

ブレイク成功率に関する統計学習を行い、突破口パラメータを調整することができます。

まとめ

本戦略はトレンド特性とブレイク特性を統合しており、理論上多くの無効なシグナルをフィルタリングできます。重要なのはパラメータのテストと最適化に注力し、戦略を異なる銘柄や時間足にカスタマイズすることで、実際の取引で良好な結果を得ることです。また、補助指標や機械学習技術も戦略改善の方向性を提供します。継続的な最適化により、本戦略は安定した信頼性の高いトレンドブレイク取引戦略となり得ます。

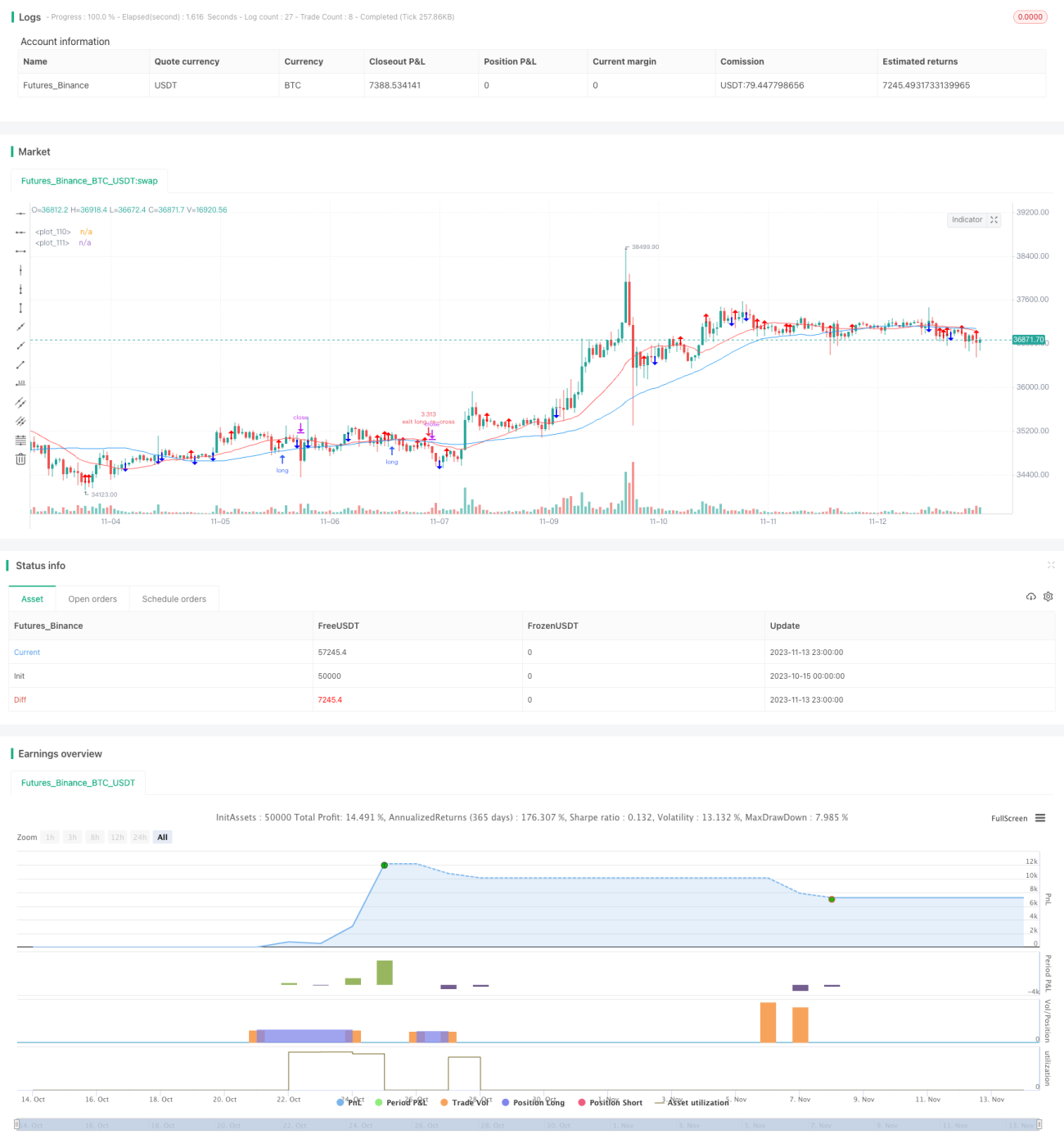

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//Backtested Time Frame: H1

//Default Settings: Are meant to run successfully on all currency pairs to reduce over-fitting.

//Risk Warning: This is a forex trading robot, backtest performance will not equal future performance, USE AT YOUR OWN RISK.- 1