双指標コンビネーションの狂乱的な日内スキャルピング戦略

概要

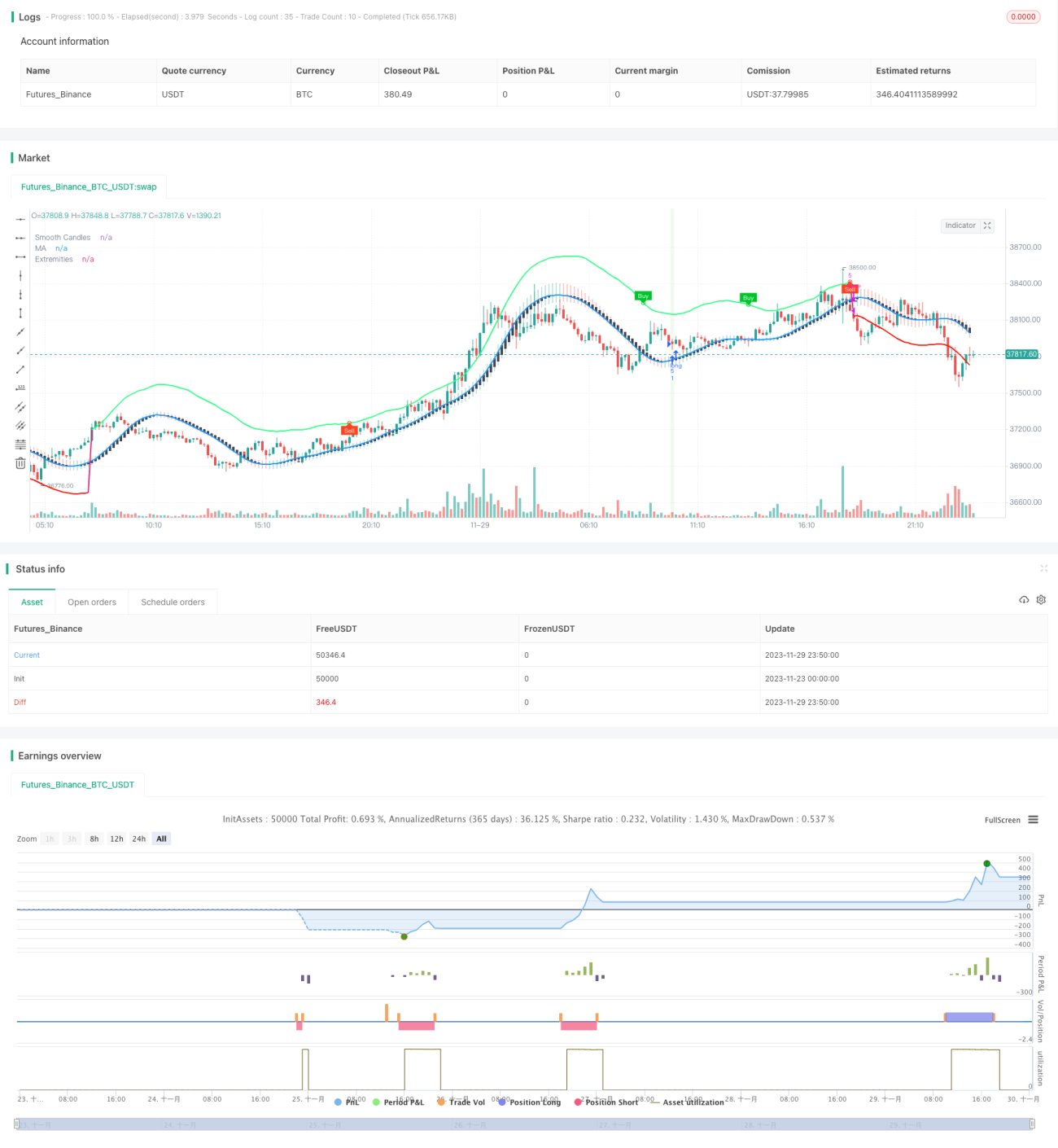

本戦略は、LuxAlgo が開発した TMO と AMA の2つのインジケーターの売買シグナルを組み合わせ、レンジ相場の中でトレンドの始まりを捉えます。TMO インジケーターの売買シグナル、AMA インジケーターの売買極値、ローソク足の実体が徐々に拡大するなど、複数の条件が満たされた場合にロングまたはショートのポジションを取ります。ストップロスは直近N本のローソク足の最高値・最安値を使用します。

戦略の原理

TMO インジケーターは価格のモメンタムを反映します。これはオシレーター系のインジケーターであり、価格にダイバージェンスが発生した際に取引シグナルを発します。AMA インジケーターは平滑化された移動平均線の一種で、価格変動の範囲を示し、価格が上限または下限に近づくと買われすぎ・売られすぎを示します。

本戦略の主要なロジックは、TMO インジケーターが価格トレンドのダイバージェンスを捉えて取引シグナルを提供し、AMA インジケーターが価格反転の可能性がある領域を示し、さらにローソク足の実体の拡大がトレンドの開始を確認するという点です。この組み合わせにより、取引成功率を高めることができます。具体的には、以下の条件下でロングまたはショートのポジションを建てます。

- TMO インジケーターがロングシグナル(価格の上向きダイバージェンス)を発し、かつ AMA インジケーターがロングの極値を示す。

- TMO インジケーターがショートシグナル(価格の下向きダイバージェンス)を発し、かつ AMA インジケーターがショートの極値を示す。

- 直近3本のローソク足の実体が徐々に大きくなっていること。

これにより、単一インジケーターでは発生する偽シグナルを低減します。ストップロス方式として直近N本のローソク足内の最高値・最安値を採用することで、リスクを適切にコントロールできます。

戦略の優位性

本戦略には以下の優位性があります。

- インジケーターの組み合わせによるシグナル精度向上:TMO と AMA の相互検証により偽シグナルを減らし、シグナル精度を高めます。

- 複数条件によるトレンド開始の捕捉:TMO シグナル、AMA 極値、ローソク足実体の拡大など複数の条件を設定することで、トレンド開始のタイミングを効果的に捉えられます。これはスキャルピング戦略が目指す目標です。

- ローソク足によるストップロスでのリスク管理:直近の最高値・最安値をストップロスとすることで、各取引のリスクを適切にコントロールできます。また、インジケーターの再計算による遅延や反転リスクも軽減されます。

- シンプルで効果的なトレーディングロジック:わずか2つのインジケーターで完結したスキャルピング戦略を実現しており、複雑ではなくロジックが明快です。また、例示の結果からも利益を上げられることが分かります。

戦略のリスク

本戦略には以下のリスクが存在します。

- 頻繁なエントリー・エグジットのリスク:スキャルピング戦略であるためポジション保有時間が短く、取引コストが高い場合は利益に影響を与える可能性があります。

- ローソク足ストップロスが過激すぎるリスク:直近の最高値・最安値をストップロスとする方法は、市場のノイズを完全に除去できず、ストップロスが発動する確率を高める可能性があります。

- パラメーター最適化の困難なリスク:複数のパラメーターが存在するため、最適なパラメーターの組み合わせを見つけるのは難しい場合があります。

最適化の方向性

本戦略は以下の方向で最適化が可能です。

- 追加のフィルター指標の導入:市場の出来高など、さらなるフィルター指標を追加することで、偽シグナルを除去しシグナル品質を向上させます。

- ストップロス条件の改善:ストップロスが過激になりすぎないよう、発動前に数本のローソク足での確認を追加するなど、条件を追加します。

- パラメーター最適化:最適な指標パラメーターの組み合わせを見つけることで、ノイズをさらに除去し勝率を向上させます。主な最適化対象は、TMO の期間、AMA の期間や倍数などです。

- 異なる銘柄・時間足でのバックテストと実運用:本戦略のロジックに最も適合する銘柄や時間足を探すため、複数の銘柄と時間足でテストを行います。

まとめ

本戦略は、TMO インジケーターと AMA インジケーターの取引シグナルを組み合わせ、レンジ相場の中でトレンドの開始を捉えてスキャルピングを行います。シグナル精度が高く、トレンドの初期段階を捉え、かつリスクをコントロールできる点が強みです。さらなるパラメーターやルールの最適化を施すことで、実戦価値の高いデイトレード向けスキャルピング戦略となり得ます。

- 1