価格ブレイクアウトに基づく適応型ボラティリティ取引戦略

1

Follow

1802

Followers

概要

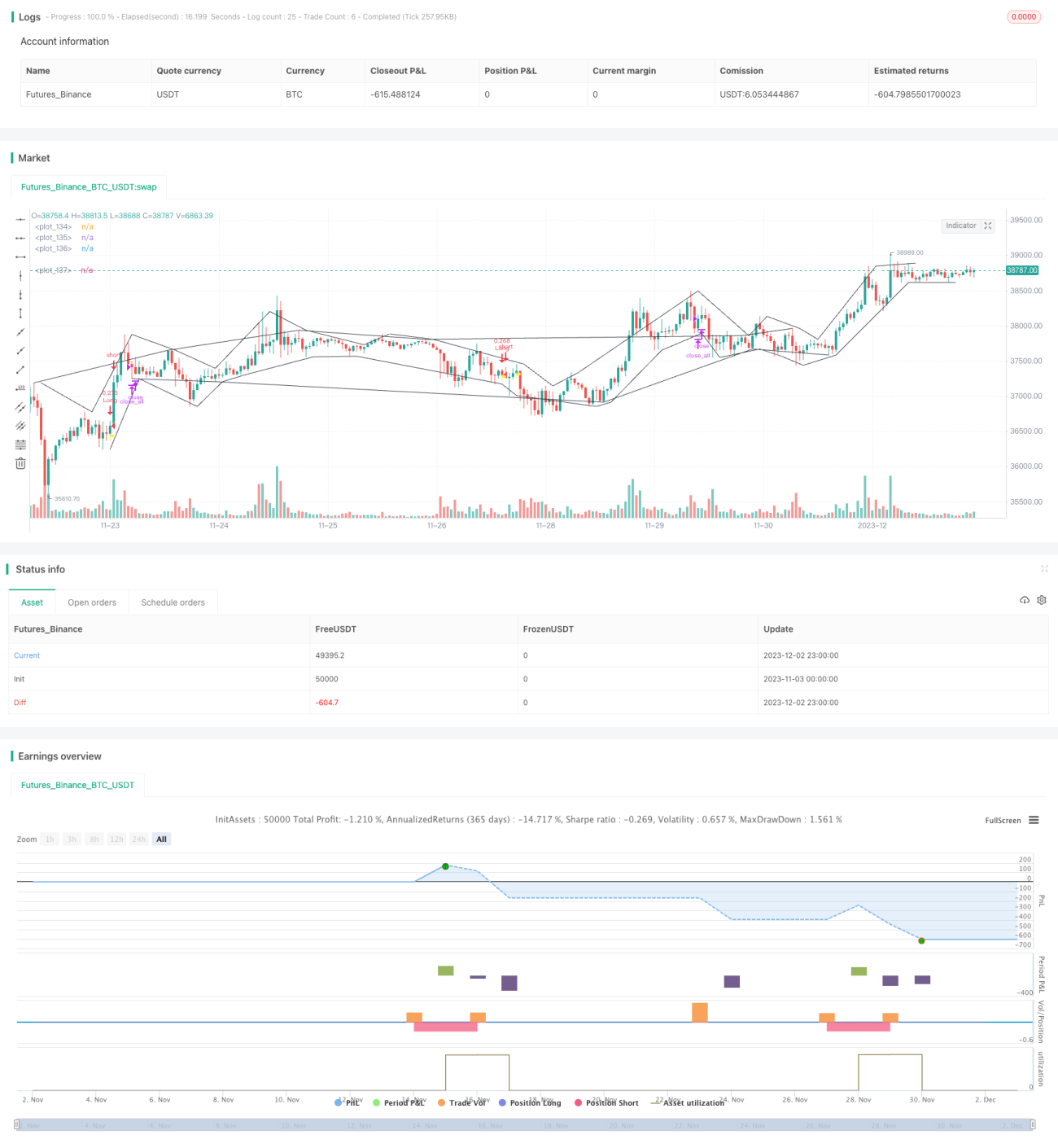

本戦略は、価格ブレイクアウトポイントに基づいて市場トレンドを識別し、適応型インジケーターを組み合わせて大勢を判断し、短期的な価格反転の機会を捉えます。価格が基準ブレイクアウトチャネルを突破したときに買い/売りシグナルを生成します。本戦略は、高ボラティリティの仮想通貨取引に適しています。

戦略の原理

- 価格の極値点をチャネルの境界として識別します。価格が新高値または新安値を付けたとき、その点をチャネルの境界とします。

- 適応型ボラティリティ指標MAを計算し、全体のトレンド方向を判断します。MAの値が大きいほど、現在はレンジ相場であることを示します。

- 価格がチャネルの上限を上抜けたときに買いシグナル、下限を下抜けたときに売りシグナルを生成します。

- ストップロスを設定します。ロングポジションのストップロスはエントリー価格の1%とします。

優位性分析

- 価格チャネルは適応性を持ち、トレンド転換点を正確に判断できます。

- ボラティリティ指標で大勢を判断し、レンジ相場で大きな方向性を見逃すのを防ぎます。

- 反転戦略であり、短期的な価格リバウンドの捕捉に適しています。

リスク分析

- 大幅な継続下落相場では、複数のストップロスが発動しやすく、大きな損失につながる可能性があります。

- レンジ相場では、頻繁な売買により取引コストが増加します。

- エントリータイミングを手動で判断する必要があり、完全自動取引ではオーバーフィッティングのリスクがあります。

最適化の方向性

- MAのパラメータを最適化し、全体の値動きをより適切に判断できるようにする。

- 出来高指標を追加し、出来高が枯渇した反転シグナルを回避する。

- 機械学習モデルを追加し、パラメータの動的最適化を実現する。

まとめ

本戦略は全体的な考え方が明確であり、一定の実用価値を持っています。ただし、特定の相場環境で大きな損失を被らないよう、取引リスクの管理に注意する必要があります。次のステップでは、全体フレームワーク、指標パラメータ、リスク管理など複数の観点から最適化を進め、戦略パラメータと取引シグナルの信頼性を高めることができます。

Source

Pine

/*backtest

start: 2023-11-03 00:00:00

end: 2023-12-03 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version = 4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © TradingGroundhog

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1