マルチファクターRSIリバーサル戦略

概要

本戦略はRSIインジケーターを利用して買われ過ぎ・売られ過ぎを識別し、MACDやストキャスティクスなど複数の補助因子を組み合わせてエントリーします。この戦略は短期的な反転の機会を捉えることを目的としており、逆張り戦略に分類されます。

戦略の原理

本戦略は主にRSIインジケーターを用いて、市場が買われ過ぎまたは売られ過ぎの状態にあるかを判断します。RSIが設定した買われ過ぎラインを超えた場合、市場は買われ過ぎの可能性が高いとみなし、このとき戦略は売りポジションをとります。逆にRSIが設定した売られ過ぎラインを下回った場合、市場は売られ過ぎの可能性があると判断し、買いポジションをとります。これにより、相場が一方の極端な状態からもう一方の極端な状態へと反転する過程で生じる短期的な取引機会を捉えて利益を得ます。

さらに、本戦略はMACDやストキャスティクスなどの複数の補助因子も導入しています。これらの補助因子の役割は、偽陽性の取引シグナルをフィルタリングすることです。RSIがシグナルを発し、かつ補助因子もそのシグナルを支持する場合にのみ、戦略は実際の取引行動を起こします。このような多因子の組み合わせにより、戦略シグナルの信頼性が向上し、結果として戦略の安定性も高まります。

優位性分析

この戦略の最大の優位性は、効率的に機会を捉え、多因子検証によりシグナル品質を向上させている点です。具体的には以下の点が挙げられます:

- RSIインジケーター自体が市場の状態を識別する能力に優れており、買われ過ぎ・売られ過ぎを効果的に特定できます。

- 複数の補助ツールによる多因子検証により、シグナル品質が向上し、多くの偽陽性シグナルを排除します。

- 戦略はパラメータに対して鈍感であり、最適化が容易です。

リスクとその解決方法

本戦略には以下のようなリスクも存在します:

- 反転失敗リスク。反転シグナル自体は統計的裁定機会に依存しており、個別の反転失敗の可能性を排除できません。ポジションサイズを小さくしたり、ストップロスを設定することでリスクを管理できます。

- 上昇相場における損失リスク。戦略全体として逆張りが主体であるため、上昇相場では一定の損失が生じる可能性があります。大勢の判断を正確に行い、必要に応じて人手による介入で不利な相場環境を回避する必要があります。

最適化の方向性

本戦略は今後、以下の点を最適化する必要があります:

- 異なる銘柄でテストし、最適なパラメータ組み合わせを探す。戦略はパラメータに鈍感ですが、それでも銘柄ごとに最適なパラメータを探すことを推奨します。

- 適応型のエグジットメカニズムを追加する。動的ストップロスや時間経過によるエグジット方法などをテストし、戦略を市場の変化により適応させることができます。

- 機械学習アルゴリズムの導入。モデルに反転成功の確率を学習させることで、戦略の勝率を高めることが期待できます。

まとめ

本戦略は全体として短期的な逆張り戦略です。RSIインジケーターの買われ過ぎ・売られ過ぎを判断する能力を活用し、複数の補助ツールによる多因子検証を組み合わせることで、シグナルの品質を高めています。この戦略は機会を効率的に捉え、安定性も良好です。さらなるテストと最適化を行い、最終的な収益実現を目指す価値があります。

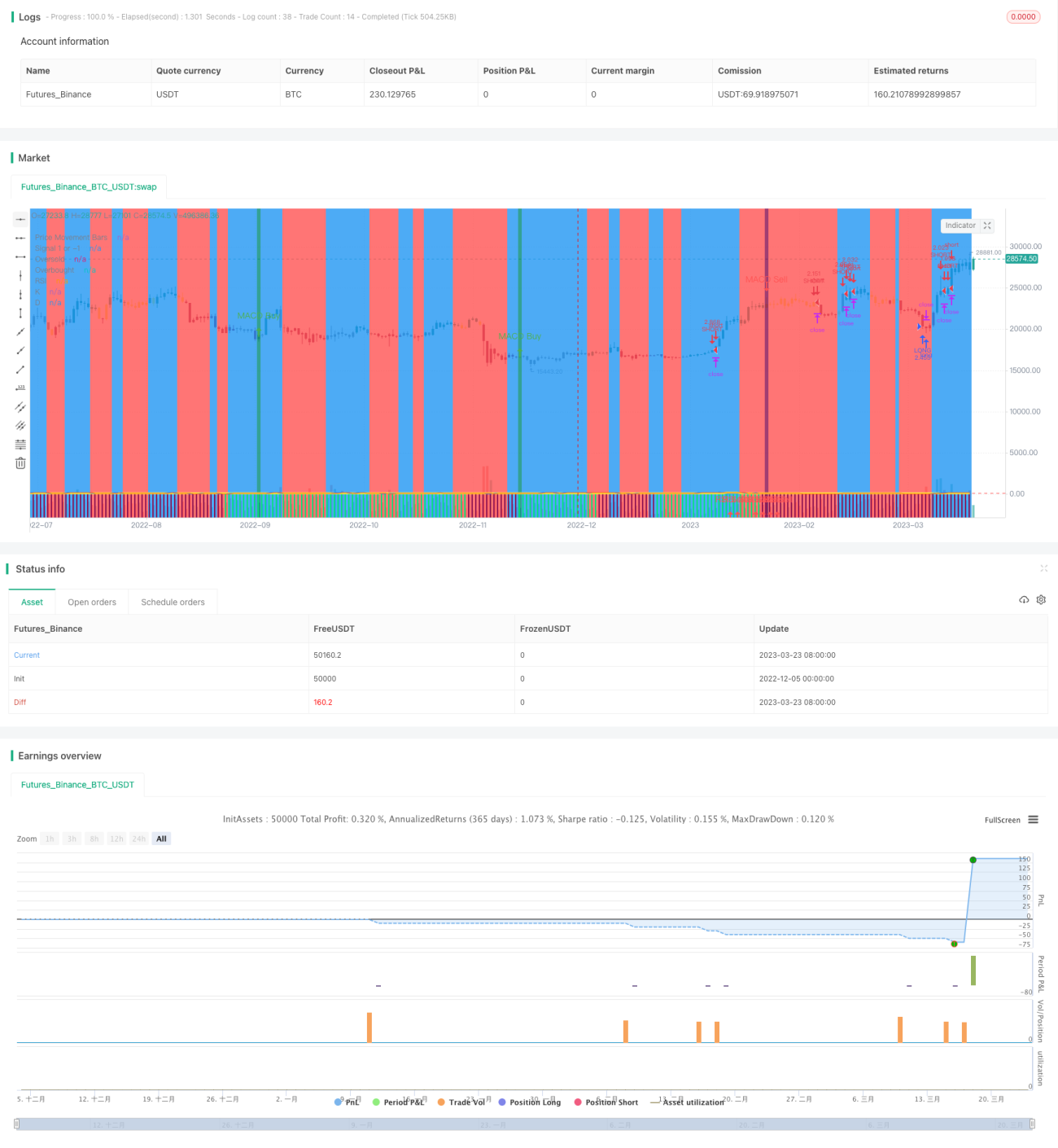

/*backtest

start: 2022-12-05 00:00:00

end: 2023-03-24 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='Ain1',title='All in One Strategy', overlay=true, initial_capital = 1000, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.18, calc_on_every_tick=true)- 1